Behavioural Economics and Practicalities of Intervention Lecture

The last four or five decades have witnessed the advent of several groundbreaking new theories in economics, several of which have interdisciplinary characteristics that make economics and business theories more robust and realistic. Several of the theories’ founders have also been awarded the Nobel Prise in economics for their efforts (covered in this chapter), including economists Warren Smith, Daniel Kahneman and James Buchanan. This chapter summarises the key contributions from five of these nascent theories: prospect theory, behavioural finance and economics, intertemporal choice, collective choice and public choice.

Obviously, there is far more detail to each of these theories than can be concluded in a relatively short overview chapter, but the main concepts are touched upon and highlighted in such a way that the reader can gain a basic understanding of each theory’s principal tenets. In addition, the chapter is full of citations and references that can be used for further research in any of the given subjects.

Prospect Theory

Prospect (or lottery) theory attempts to explain how people choose between probabilistic alternatives involving risk, when the probabilities of outcomes are known. People base decisions based on the potential gain or loss (rather than the outcome) of real-life choices, evaluating them using heuristics (Kahneman & Tversky 1979) or biases—simple and efficient rules that people use to form judgments and make decisions—wherein they decide what outcomes they consider equivalent. Furthermore, it is not correct to say that some personality types are naturally more risk-taking than others, but rather it is the context or the domain of gain or loss which determines the level of risk a rational person is willing to take. Individuals use a reference point (such as the status quo) to decide whether they are presently in the domain of loss or gain.

Once the reference point is set, a person considers poorer outcomes as losses and better ones as gains. Curiously, losses are more painful than the elation one gets from gains, making people “loss averse.” For most people, losing one thousand Euros hurts more than gaining the same amount pleases them. Overall, the theory more accurately describes decision making (psychologically) than was commonly done under expected utility theory (Tversky & Kahneman 1992).

The theory has profoundly impacted economics, including its public choice sub-discipline, as well as political science. “Almost all decisions by political actors entail a certain degree of risk, whereby risk is the probability that an event occurs (e.g. losing the election) times the impact that it did (e.g. losing office)” (Vis 2011: 334). Prospect theory helps political actors deal with decision making under risk, where people make different choices when facing losses, compared to their risk-adverse behaviour when confronting gains—so they can hold on to those gains (341).

1.1 Decision Processes

As people choose between valuable alternatives or choices, they pass through editing and then evaluation stages. In the editing stage, the expected outcomes from a decision are ordered per a heuristic. People decide which outcomes are equivalent and set a reference point. Less outcomes are considered losses and greater ones, gains. All probabilities are treated together rather than isolated. They are, as needed, combined, simplified, segregated, eliminated and sorted in order of dominance.

In the evaluation stage, people compute values based on the potential outcomes and their expected probabilities. Lower probabilities are said to be over-weighted, or considered by the decision maker to be of a higher probability than they really are, impelling him to favour the alternative choice. The resulting computed values fit into the economist’s utility maximising equation. In the final evaluation, the decision that produces the highest utility is chosen.

Need Help With Your Economics Essay?

If you need assistance with writing a economics essay, our professional essay writing service can provide valuable assistance.

See how our Essay Writing Service can help today!

1.2 Heuristics

Kahneman (2003: 1450) more recently argued that, “People are not accustomed to thinking hard, and are often content to trust a plausible judgment that comes to mind.” For that reason, they use heuristics or biases (or even prejudices) to make decisions easier. Rather than disparage such behaviour, Gigerenzer, Todd and others (1999) argue that heuristics generate accurate judgments rather than biased ones. Heuristics are “fast and frugal” alternatives to more complicated procedures, and often yield good solutions. People seek to minimise thinking tasks and decision making costs, and frequently look to lower-cost alternatives instead of doing more careful analysis.

Unfortunately, people are frequently over-confident that they are right. Psychologists have found on many occasions that when a person is 98% sure that something is right or true, he is wrong 30% to 40% of the time (Lichtenstein, Fischoff & Phillips 1982; Tversky & Kahneman 1974). Economists have long recognised that lack of knowledge (Hayek 1945), or market ignorance and uncertainty, are stark realities. For that reason, people form institutions (North 1992) and use heuristics, biases and prejudices to reduce search costs, decision costs and other transactions costs.

Nevertheless, while heuristics work well under most circumstances, they can at times generate systematic deviations from logic, probability or rational choice theory. Such errors are called “cognitive biases.” Documented cases of how this bias affects choices have been observed in home valuation, deciding the outcome of a legal case, or choosing an investment. Heuristics are dominant in people’s automatic, intuitive judgments, and are also used deliberately as mental strategies under imperfect or limited information (Haselton, Nettle & Andrews 2005; Tversky & Kahneman 1974).

Behavioural Finance

2.1 Fundamental Idea

Behavioural finance, like behavioural economics (Simon 1987), studies the effects of cognitive, psychological, social, and emotional factors on economic decisions. As Hirshleifer (2015: 133) notes, it is “the application of psychology to finance, with a focus on individual-level cognitive biases.” It also considers the impact of such decisions on prices and resource allocation, other kinds of behaviour in different environments. Since behavioural finance (and economics) deals with the bounds of rationality of economic agents, its models typically integrate insights from psychology, neuroscience and microeconomic theory, permitting them to touch a broad range of fields, concepts and methods.

For instance, scholars study how market decisions are made, as well as the processes that drive public choice theory (Plott & Smith 2008; Smith 1962, 1976, 1982), covered in the last section of this chapter. Some have equated behavioral finance’s potential impact on the field of finance as being like Einstein’s on Newtonian physics (Maymin 2011: 125), and has challenged the current viability of the efficient markets hypothesis (Shiller 2003; Malkiel, Mullainathan & Stangle 2005).

2.2 Relationship with Behavioural Economics

Experimental economics is the branch of that science involved in the design and conduct of laboratory experiments to test the hypothesis that the competitive market process yields welfare-improving (and possibly welfare-maximising) outcomes (Smith 2000, 2008). Relatedly, behavioural finance does similar experimentation in the world of finance. The injection of behavioural finance into modelling has improved investor predictions, managerial expectations and has lessened the need for vigorous regulation (Muradoglu & Harvey 2012: 75).

For example, researchers found that during the financial crisis of 2007-2008, people succumbed to non-rational behaviour: hubris, over-optimism, anchoring and herd behaviour, citing culprits of inadequate management and regulatory capture as reasons for the depth of difficulties experienced that led to the irrationality (Grosse 2012). In Japan, researchers have identified overconfidence bias in earnings forecasts and estimates by managers, leading to a decrease in the probability of issuing equities in the public market “by 4.7% per one standard error” (Ishikawa & Takahashi 2010). In other words, managerial irrationality, bias and overconfidence lead to distortions in corporate financing as well as merger and acquisition decisions (55).

2.3 Key Elements and Paradigm Shift

There are three prevalent themes in behavioural finance: (1) heuristics, where people often utilise rules of thumb instead of strict logic to make decisions, (2) framing, which are the mental emotional filters individuals rely on to understand and respond to events, including anecdotes and stereotypes, and (3) market inefficiencies, including non-rational decision making and incorrect pricing (Minton & Kahle 2013; Shleifer 1999). Also important is the “central role” of feelings and sentiment in decision making (Hirshleifer 2015: 151). Hence, since the 1990s, the field of finance has shifted away from econometric analyses of time series of prices, dividends and earnings, to models based on human psychology as it relates to financial markets (Shiller 2003: 90).

2.4 Theory of the Second Best in Relation to Public Policy

Relatedly, the economic theory of the second-best deals with situations where one or more optimality conditions cannot be satisfied. Richard Lipsey and Kelvin Lancaster (1956) showed that when this condition occurs, the next-best solution might involve changing other variables to otherwise non-optimal values. In public policy, the theory implies that when removing a market distortion is infeasible, introducing an additional distortion may partially counteract the first one, leading to a more efficient outcome.

Trying to correct an uncorrectable market failure in one sector might decrease economic efficiency in another, related sector. Instead, the theory suggests that leaving the two market imperfections to cancel each other out would be better than fixing either one, implying that optimal public policy intervention might be unusual. Therefore, economists should study the details of any policy situation before jumping to a conclusion based on standard theories which suggest that an improvement in one area implies global improvement in efficiency.

For instance, since air pollution is frequently associated with production, it will likely increase with greater output. If there is a lot of competition that production, pollution levels might increase. Therefore, eliminating monopolies in a sector will not necessarily increase economic efficiency. Even if gains from trade in the production of a natural resource increase, negative externalities from pollution also increase, perhaps outweighing those gains.

Intertemporal Choice

Intertemporal choice studies how people make choices between alternatives, and how much to spend, at various points in time, given that choices at one time influence the available opportunities at others. Such choices are influenced by the relative value assigned to two (or more) payoffs at different future points, and usually require a person to make tradeoffs.

3.1 Traditional Models

Economists have traditionally used a discount rate to analyse intertemporal decisions via the discounted utility model, which assumes that people evaluate utility or disutility like financial markets evaluate gains or losses, exponentially discounting the value of outcomes corresponding to the delay required to realise them. This method has been used to model intertemporal choices and as a public policy tool to analyse spending for research and development, health and education (Berns, Laibson & Loewenstein 2007).

The Keynesian consumption function suggested that average propensity to consume falls as income rises, and early empirical studies were consistent with it. However, post-World War II studies identified the opposite thing occurring: savings did not rise as incomes rose. Thus, a refined version of the theory of intertemporal choice emerged to replace the Keynesian theory.

Intertemporal choice was introduced and elaborated over a century of thought by John Rae (1834), Eugen von Böhm-Bawerk (1884) and Irving Fisher (1930). Later, the life cycle income hypothesis was proposed by Franco Modigliani (1956) and the permanent income hypothesis by Milton Friedman (1957), both of which showed that a Walrasian Equilibrium can be extended to incorporate intertemporal choice, yielding the concepts of futures prices and spot prices—the former for what people expect prices will be and the latter what they are today.

3.2 Upgraded Models

Since those earlier studies, much interdisciplinary empirical work has been done by economists, sociologists, psychologists, neuroscientists, ethnologists and mathematicians that a new way of thinking about choice has emerged. Hundreds of studies and many new theories have tried older economic discounted utility theories (Loewe 2006). In one such study, pensioners in Croatia showed intertemporal behaviour by choosing a larger, stream of payments when they had good health, expectations of longevity, higher incomes and liquidity. However, in another study, when they feared currency devaluation or political instability, they preferred a smaller, immediate payment (Brown, Ivkovic & Weisbenner 2015).

Sensitivity to income shocks in Italy showed “consumption mobility” in insurance markets, especially among lower-income, lower-educated people (Jappelli & Pistaferri 2006). Noor (2011) found that people tend to be more patient when they expect larger rewards, and thus developed a model where the discount factor changes according to the amount of the future payout. However, human behaviour is not consistent under demand shocks, where choices depend on whether a person is “sophisticated” or “naïve,” but more particularly on their level of risk aversion (Chen & Schwartz 2007). Also important are “subjective income expectations” and the role of “innovation” in predicting future income, which is the superior information of economic actors trumps that which is available to econometricians attempting to do estimations (Kaufmann & Pistaferri 2009).

3.3 Hyperbolic Discounting

Hyperbolic discounting theory demonstrated that one’s discount rate for future utility might decline over time (Thaler 1981), especially since deferring consumption for one period on objects of choice in the distant future is not very relevant, although there have been some effective criticisms of the theory (Rubinstein 2003). In the final analysis, many scholars would agree that, “dynamic consistency has been acting as an invisible straitjacket obstructing the development of intertemporal choice theory, and that it is only by undoing it that this field of research can achieve in the future a satisfactory understanding of human decision-making” (Loewe 2006: 217-218).

Some scholars have found that preferences themselves are the result of “evolutionary forces,” and have studied the habits of birds (e.g., pigeons) to show how instinct and behaviour, especially cravings and urges, induce animals to make the “right” choice in the average situation (Dasgupta & Maskin 2005: 1290, 1298). Accordingly, studies using conventional or traditional assumptions frequently go awry when the time preferences of economic actors are considered, whereas hyperbolic and “quasi-hyperbolic” discounting produce far better results in calculating the present value of annuities (Nagy 2010). Furthermore, the existence of secondary markets for durable goods produced by firms with market power were found to affect the price and allocation in primary markets among sophisticated consumers that understand that they can sell goods they purchase, leading them to procrastinate, and hyperbolic discounting is thus verified (Nocke & Peitz 2003).

However, contest participants tend to choose differently than when subject to normal individual choice conditions, and exhibit significant differences in individual discount rates for possible prises, which might leave classical discounting relevant in such “strategic settings” (Deck & Jahedi 2015: 159-160). Thus, for all its advance, hyperbolic discounting may not provide a general explanation for all observed human action in choosing between present and future consumption, investment, etc.

Collective Choice

Collective choice deals with “the ability of groups to implement efficiency-enhancing institutions,” especially those that “foster cooperation.” Indeed, people prefer to cooperate rather than compete if there are well-defined, inter-group competition rewards for the best-performing groups—although it does not usually improve Pareto conditions (since losing groups are worse off). Nonetheless, individuals were shown to prefer to contribute to their group’s overall performance and, “the incentive to outperform other groups mitigates the free-rider problem within one’s own group.” This fact holds true whether the rule is imposed or selected by majority voting (Markussen, Reuben & Tyran 2014: F163, F186-F188).

In households, individual intertemporal choice was found to be consistent with exponential discounting models. However, household consumption choices were not, and took on different characteristics when collective, where individual heterogeneity is subject to renegotiation. Moreover, heterogeneity discount factors were found to be correlated with the head of household’s age and education level, as well as the wife’s employment status (Adams, Cherchye, De Rock & Verriest 2014). In firms, collective choice in capital-intensive firms can be especially prominent when a firm has financial difficulties and, thus, the workers have a unified common concern. However, the best success stories of such collective action occur in a “muted or indirect forms of worker participation” in company management rather than direct management by employees (Dow & Skillman 2007: 123).

Normally, as Mancur Olson (1971/1965) argued in The Logic of Collective Action, the incentive for group action decreases as the sise of the group increases, unless individuals are offered selective incentives. Moreover, “collective action has characteristics analogous to a pure public good” (Congleton 2015: 232). His powerful argument has launched many research programs including the new institutional economics (North, Williamson, et al) and public choice (Buchanan, Tullock, Tollison, et al), and resurrected interest in many Austrian School theories (Mises, Hayek, Rothbard, Kirzner, et al).

Public Choice

5.1 Intensified Interest Group Activity

Given that a single vote is virtually meaningless, i.e., yields infinitesimal political influence, choosing not to vote is rational—especially where the state does not obligate citizens to vote. However, investing time in convincing others to vote for some important issue is apparently of great value, since special interest groups (SIGs) and political action committees (PACs) clearly abound in democratic societies. Moreover, since successful SIGs and PACs represent large blocks of votes, they command considerable political influence. Therefore, mature democratic processes tend to rationally proliferate SIG and PAC activity, especially when government regulation is expanding.

While the market process is guided by an “invisible hand” (Smith 1776) that coordinates catallactic coordination and cooperation among self-interested human actors, the political process is “led by an invisible hand to promote other kinds of interests” (Mitchell & Simmons 1994: 39) and SIG and PAC activities distort or subvert “public interest” goals in favour of private interests. Likewise, public policy cannot cure market failures. Instead, it often makes social problems worse.

Government is not a “frictionless plug” which, as welfare economists often propose, can be used to alleviate market failures. On the contrary, instead of genuine social benefits, the political process often provides “intense competition for power to benefit particularised interests at the cost of wider society” (Mitchell & Simmons 1994: 211-213).

The presence of SIGs and PACs distort democratic processes, transforming public policy into a battle between special interests primarily to benefit private interests. Government power ends up embellishing private interests at public expense, often dressed in “public interest” garb. As “bad” as markets might be in eliminating social problems, therefore, government “solutions” may be worse.

5.2 Demosclerosis

Public choice theorists contend that what often appears to be political gridlock due to SIG and PAC pressures is a misperception. On the contrary, political actors are more responsive and willing to change than ever, as evidenced in the United States (Rauch 1996: 17-18), and their rapidness, responsiveness and adaptability leads society to a state of demosclerosis. SIGs and PACs work so hard and fast to please constituents and retain past political benefits, that the casual onlooker mistakenly sees what appears to be nothing more than political gridlock. In the end, SIGs and PACs are so effective that their benefits never get cut out of budgets—no matter how popular reform movements may be.

Democratic societies generate SIGs and PACs, as well as lobbies, much faster than they eliminate them. These groups frequently win (and defend) government subsidies, favourable regulation, or tax breaks. Vote-seeking politicians exacerbate demosclerosis by retaining these benefits in order to avoid the political backlash against them—through upsetting blocks of voters represented by the affected SIG or PAC. Politicians (and to a lesser extent bureaucrats) are eager to keep as many voters happy as necessary to win re-election, making benefits increasingly difficult to remove once granted.

Consequently, government “succumbs to a kind of living rot…Stuck with all of its first tries [at various regulations or programs] virtually forever, government loses the ability to end unsuccessful programs and try new ones. It fails to adapt and, as maladaptive things do, becomes too clumsy and incoherent to solve real-world problems” (Rauch 1996: 18; Mitchell & Simmons 1994: 53, 76).

5.3 Rent Seeking

A frequent goal of SIGs is to gain market power and maximise profits through political action. Contrary to the market process, where entrepreneurs gain monopoly benefits that are quickly dissipated as others rush to enter the market, the political process can be used to thwart this natural check against long-lived monopoly privileges. For instance, government often enforces monopoly privileges by barring all potential entrants through patents, import tariffs, forcing consumers to buy goods from patent holders through “public interest” legislation (e.g., air bags in cars, fire extinguishers and fire-suppressing devices in buildings), taxicab medallions, occupational licensing, etc. For firms, obtaining government-sanctioned monopoly is very attractive, and often much cheaper than dealing with competition in the marketplace.

Such attempts to manipulate or control markets are known as rent seeking, which is probably better termed “privilege-seeking.” Tullock defines rent seeking as “the manipulation of democratic [or other types of] governments to obtain special privileges under circumstances where the people injured by the privileges are hurt more than the beneficiary gains” (Tullock 1993: 24, 51). Buchanan says, “The term rent seeking is designed to describe behaviour in institutional settings where individual efforts to maximise value generate social waste rather than social surplus” (Buchanan 1980: 46-47).

5.3.1 Theoretical Bases of Rent Seeking

Mutually beneficial gains from trade exist in all voluntary market exchange (i.e., making trade a positive-sum game). However, rent seeking is likely to generate net destruction of value because of the monopoly privileges granted. Thus, rent seeking is at best a zero-sum game and is possibly a negative-sum game akin to outright theft.

Public choice theory shows that the social loss from rent seeking is not just the “Harberger Triangle” in the typical monopoly diagram, but also the “Tullock Rectangle”—the area to the left of the Harberger Triangle. Social losses are exacerbated by “paperwork contests,” as the Tullock Rectangle is dissipated by competing SIGs and “reformer” SIGs that are seeking monopoly benefits (Higgins & Tollison 1988: 150-151). Moreover, the winning rent seeker may end up losing some or all his monopoly gains to reformers, or through his expenditures made to retain those privileges (Tollison & Wagner 1991: 60-64). Consumers lose by paying higher prices under the government-enforced monopoly privilege, along with any ancillary distortions in labour markets and any portion of the rent seeking costs passed along to taxpayers.

Rent seeking may go beyond attempts to obtain monopoly power. Rent seeking is, broadly speaking, any attempt to gain “concentrated benefits” through the political process while “dispersing the costs” over a wide range of ignorant or uniformed voters and residents, resulting in social losses. For instance, a rent seeker might try to attain public policy or regulation to create artificial demand for his product, processes, innovation or service that would otherwise have little market demand. The same is true for securing an exclusive licence over a production method.

5.3.2 Milking Theory and Regressive Entrepreneurship

Furthermore, legislators and regulators (or “favour brokers”) are often savvy with respect to rent seeking activity and might require being cut into the deal in order facilitate the “public interest” privilege—whether directly or indirectly. This process is called milking (McChesney 1987), which is like legal blackmail in effect. Accordingly, it behooves rent seekers to hire consultants that that can both identify lucrative rent seeking opportunities and to minimise milking payments to favour brokers. For instance, costs can be reduced by wisely manipulating the media with an ad campaign that changes public perception of a product, service or process, and thus affects the vote-seeking favour-broker’s actions and attitude.

Successful rent seekers master the art of convincing government actors that they deserve to be granted a special privilege. Those who are eminently “alert” to discovering and obtaining rent seeking opportunities are called regressive entrepreneurs (as opposed to progressive entrepreneurs found in the market). They are regressive because their activity creates social losses, although they profit personally.

Economists do not render value judgments regarding economic behaviour, including the ethics or morality of rent seeking, even though it undermines the quixotic view of government long-promoted by political scientists and historians. While scruples might prevent some people from seeking rents, just like they prevent others from engaging in objectionable businesses (e.g., prostitution rings, drug dealing, etc.), they will not impede everyone.

Moreover, any deterrent to such behaviour is mitigated when something once an objectionable is legalised (e.g., marihuana). Indeed, the marketplace evinces that there are always some that are plenty of economic actors who will avail themselves of privilege seeking. Economists do not declare these rent seekers to be “bad” or “immoral” but rather explain why their behaviour is both rational and to be expected. Accordingly, sustaining democratic processes free of rent seeking is implausible.

5.4 The Transitional Gains Trap

Coupled with rent seeking theory, Gordon Tullock identified a “transitional gains trap” that occurs once favoured SIGs win monopoly privileges through licensing requirements. Even the most effective and efficient SIGs must expend considerable resources to attain these privileges. Nevertheless, the monopoly privileges won by the initial rent seekers are transitional, since over time all new entrants will be “trapped” into paying the resulting artificial “entrance fee” (e.g., a taxicab medallion)—effectively transferring their profits from participating as a monopolist to the government. Thus, consumers pay monopoly prices but the firm ends up losing its monopoly gains.

Like any tax that does not yield a direct benefit in return, there is a permanent net social loss: “surviving original owners have opportunity costs equivalent to the price of the entry barrier and consumers are worse off” (Tullock 1975: 671-675). Accordingly, while the original privilege winners have transitional gains, afterwards there is a permanent deadweight social loss with consumers paying perpetually higher prices. Reform is unlikely since removing the barrier to entry or other restriction would require compensating new entrants for the fee (medallion, tax, etc.) paid to enter the market.

Moreover, why would government reform the policy if it means that a source of tax revenue would be lost? Consequently, those who have paid the “fee” will fight to retain them rather than lose the value of that medallion or privilege on their balance sheets, and vote seeking politicians will be “reluctant to inflict direct losses on specific sections of the electorate” (Tullock 1993: 68). The transitional gains trap is, lamentably, largely unavoidable so long as rent seekers are active in democratic processes. Rent seekers will disregard any long term social losses inflicted on others so long as they can benefit (especially if they expect to be protected in the future by “grandfathering” provisions).

5.5 Regulatory Capture

“Capturing” regulators can have a similar “beneficial” effect as rent seeking. Thus, industries might form SIGs to attempt to indirectly utilise government regulation for their benefit. For instance, they might be seeking beneficial regulation that: creates or sustains artificial demand for their products, assails their competitors, generates direct cash subsidies, restricts the output and prices of compliments and substitutes, legitimises price-fixing schemes, or erects barriers to entry against potential competitors. Moreover, the firm or industry that successfully captures its regulators will likely be able to disperse most (if not all) of the costs of the regulation to rationally ignorant voters, consumers or taxpayers over time.

5.5.1 How Capture Is Accomplished

When regulators are captured, private interests will dominate the “public interest” at the expense of consumers and taxpayers. But how can regulators be captured? One way is to create a new committee to serve the “public interest.” Another way is to (clandestinely) recommend and have a “friend” of the firm or industry placed on an existing regulatory board. Sometimes this can be accomplished through industrial strategy. For instance, three firms can intentionally collude in pricing and then tip off the media to the scandal, generating public outcry. The firms can then blush and become penitent, later recommending a new regulatory board as an act of “penance” to ensure that the public interest is never again compromised by their recidivism.

Then the firms, which know the industry better than anyone, will submit a list of “impartial” and “qualified” candidates to sit on the regulatory board. The friendly (or even paid) relationship that these candidates have with the firms is, of course, not divulged. At first, the new regulators castigate the miscreant firms but, not surprisingly, after some years of practice and being dismissed from close public scrutiny, favourable regulation begins to emerge. Thus, the firms suffer costs for several years but in the long run gain very large benefits through their capture strategy. The same thing can be accomplished by placing such “friends” on existing regulatory boards—even if by corruption, i.e., buying off legislators and bureaucrats (directly or indirectly).

5.5.2 Examples of Captured Regulators and Legislators

Scholars point out that antitrust regulation purports to be for the “public interest” but, in reality, it benefits monopolies and privilege seekers (DiLorenzo 1985; DiLorenzo & High 1988; Shughart 1990; Stigler 1971). Studies of early business regulation in the United States also evince that it emerged from opportunistic, strategic rent seeking or capture activity rather than publicly-spirited legislators themselves, such as the Pure Food and Drugs Act of 1906 (High & Coppin 1988), and the Cable Television Consumer Protection and Competition Act of 1992 (Boudreaux & Ekelund 1993: 356, 390). Local governments also practiced rent seeking to obtain federal funding for road repairs (Tullock 1993: 17-18).

The realities of rent seeking and regulatory capture are not glamorous for consumers, even though privilege winners, “friends,” political consultants, “milkers” and favour brokers profit from its ongoing social losses, resource misallocations, economic distortions and even venality. Nevertheless, there can be no question that these activities are merely natural outcomes of self-interested participants strategically taking advantage of legal opportunities provided by democratic processes. So far, no country’s constitution has been strong enough to prevent either malady.

Need Help With Your Economics Essay?

If you need assistance with writing a economics essay, our professional essay writing service can provide valuable assistance.

See how our Essay Writing Service can help today!

5.6 Vote Seeking

Quixotic notions of public service aside, public choice theory states that self-interested politicians are primarily driven by the dominant objective of re-election. Successful ones generate political benefits in excess of political costs. Accordingly, when spending public money, they calculate how many votes they will receive per dollar spent. Likewise, they calculate how many votes are lost from favouring one group at the expense of another. In the end, they determine the policy mix that optimises their vote count (Mitchell & Simmons 1994: 52, 73).

The “median voter theory,” coupled with the fact that more women than men vote, instructs vote seekers about optimal methods of securing the votes they need. Hence, they tailor emotional appeals to the relatively unprincipled and predominantly female voters near the centre of the frequency distribution. Subsequently, vote-seeking politicians not only gain political power, but also perks, milking money paid to their “foundations,” favour-broker benefits, and at times outright opportunities from venality—all of which accompany their office.

Conformably, “[t]he politician is…always selfish no matter whether he supports a popular program in order to get an office or whether he firmly clings to his own—unpopular—convictions and thus deprives himself of the benefits he could reap by betraying them…Unfortunately the office-holders and their staffs are not angelic. They learn very soon that their decisions mean for the businessmen either considerable losses or—sometimes—considerable gains. Certainly, there are also bureaucrats who do not take bribes; but there are others who are anxious to take advantage of any “safe” opportunity of “sharing” with those whom their decisions favour” (Mises 1966/1949: 734-735, 852). Thus, the politicians who decree and oversee regulation will practice vote-seeking. Their first objective will be to get re-elected, not to serve the public interest.

5.7 Perverse Incentives: Theory with Example

Despite its pejorative name, perverse incentives theory does not imply that the motives or character of planners and others who create public choice problems are “bad” people. Instead, like rent seeking and regulatory capture, such difficulties are simply viewed as the predictable result of economic self-interest. Adam Smith’s famous theory from The Wealth of Nations (1776) is merely applied to the political process. As a result, perverse incentives emerge in public policy contexts that generate the objective to maintain private, individual benefits at public expense, thereby creating social losses and government failures in its public policies. While the market may fail, government fails worse.

For starters, planners have a perverse incentive to be ineffective. “The government will never lose profits from being a poor regulator; in fact, the opposite is likely to be true” (Holcombe 1995: 103). Certainly, if regulation were fully effective at eliminating a negative externality (e.g., air pollution, structural fires, train derailments, automobile accidents, falling water tables, drug trafficking, prostitution, etc.), the need for regulation would vanish. Knowing this fact, regulators or planners that want to maintain their gainful employment (and certainly virtually all of them do) have an incentive to maintain a minimum level of the negative externalities that they are employed to combat. They have their jobs because the negative externality exists.

Ironically, these same planners have a perverse incentive to encourage and disseminate adverse public information which suggests that current regulation is failing in part or is underfunded and is thus unable to achieve its objective. The expected response to such information will be to increase regulation, which in turn will likely lead to larger budgets and thus greater power and salaries for planners. Consequently, from a public choice perspective, regulatory failures may be successes, and part of an opportunistic strategy. The goal is to do one’s job well, but never too well.

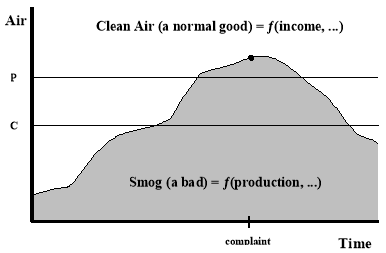

5.7.1 Perverse Incentives Model

The perverse incentives problem can be illustrated by Figure 1—a hypothetical example of air pollution levels (and regulatory constraints) for a major city. Note that any social malady (e.g., drug abuse, fires, drought, etc.) could be substituted in the example and the results would be similar. Assumptions: (1) clean air is a normal good, (2) earnings rise over time, (3) all production produces pollution, either directly or indirectly, and that (4) the urban area and its economic production are growing over time.

People will enjoy rising incomes and will be willing to accept higher amounts of air pollution to sustain that income as the city develops—at least up to a certain point of contentment, denoted as C. However, as the smog level rises above C, people start becoming concerned, and eventually preoccupied, about the smog problem. Nonetheless, most folks will still tolerate dirtier air because of the benefits they get from urban life, at least up to the point denoted as P, where they become critically preoccupied. Complaining will intensify from that point onward, too.

Figure 1: Clean air levels constrained by public policy (Cobin 2009: 176).

Moreover, as the smog level surpasses P, some people might neither complain nor change smog-producing behaviours in the short run, so long as they believe that the rise above P is only temporary. However, once they realise that the preoccupant level of smog is permanent, and even rising, they will take steps to alleviate the problem. Two options are feasible: market or public policy.

5.7.2 Market-Based Solution

The first option is to simply let profit-motivated innovators and entrepreneurs spontaneously develop solutions for the pollution problem. When people’s backs are against the wall, the human mind, the “ultimate resource” (Simon 1996), is keen to find a way out of difficulty. The problem is that people are not always patient enough to undertake such a “risky” strategy, thus making them opt for public policy instead. But public policy is not the most efficient or effective choice.

Since clean air is a normal good, people will buy more of it as incomes rise. Above P, people will even trade considerable portions of their relatively high incomes for cleaner air. Consequently, experts, innovators and entrepreneurs will emerge to meet the market demand, with competition leading to technological improvements that make pollution abatement increasingly cheaper. Over time, the subsequent lower price will permit acquiring more clean air for constant amount of money or percentage of income. Consequently, the smog level will continually decline, probably at a decreasing rate.

While smog might be reduced to zero someday, it is unlikely because the opportunity cost of doing so rises at an increasing rate. Thus, the costs of purity, just like getting dishes 100% clean instead of settling for 98% clean, are often sufficiently high to deter people from achieving it (e.g., paying double each month for hot water). It is usually not worth paying for absolute perfection or purity. Nevertheless, it is likely that the smog level will remain somewhere below C over the long run, where there would be less uneasiness caused by breathing smoggy air.

5.7.3 Public Policy Solution

The second option is to implement public policy to deal with the smog problem. The “public interest” would be invoked by politicians, perhaps citing both positive rights to clean air and negative rights to protection from against the pollution and its external costs. Vote seeking politicians will respond to the demands of voters, SIGs and PACs in two ways: (1) by creating a bureaucracy to “solve” the problem and (2) by taxing away a percentage of wealth or incomes to support it. As a result, personal freedom (utility) is also diminished by the new regulation.

The new bureaucrats, consultants and regressive entrepreneurs will probably be experts in pollution abatement, and people will experience the rigors of complying with their “public interest” objectives. Consequently, the smog level will decline, just as it would under the market option, and people will stop complaining vociferously once they perceive that smog has fallen below P. Hence, bureaucrats have an incentive, either directly or through pressure exerted by vote seeking politicians, to cross that threshold as soon as possible. When they attain that goal, voters will be elated with the regulatory effectiveness and will, in turn, laud the politicians that initiated it.

However, with the level of smog below P, the bureaucrats are faced with a perverse incentive. Consider that if the smog level should drop below C, social uneasiness would diminish sufficiently far that people would begin to complain more about the taxes and regulation pertaining to the bureaucracy than the smog itself. With cleaner air in place, people will prefer more disposable income and freedom from regulatory rigors. The wily bureaucrats, who will certainly want to keep their jobs and maximise their departmental budgets, will quickly realise their predicament and, thus, the importance of maintaining the smog level above C. Accordingly, they will choose policies and favour technologies that do so, implementing or relaxing them to ensure that a mildly uncomfortable level of smog persists. Note that they are also bounded by P on the upside, since crossing that line would lead to their dismissal for being incompetent. They must keep the problem between the C—P range if they want to stay employed.

Therefore, while serious smog problems will likely be alleviated and controlled by public policy—and evidence from urban regulation might confirm it—the key insight is that smog will never be eliminated or brought to a level below C in the long run. Thus, political intervention to eliminate smog will simply render an uncomfortable yet tolerable amount of it as a permanent part of social life. The same is true for any policy aimed at improving the quality of life or alleviating negative externalities such as drug abuse, fires, illegal immigration, drought, prostitution, teenage pregnancy, divorce, etc.

It is hard to find a compelling reason why self-interested planners and regulatory enforcers will be free from perverse incentives. Therefore, public choice theorists are hardly surprised by continual reports of some level of negative externalities related to fires, crime, terrorism, population densities, transportation, illegal immigration, drought, energy consumption, “climate change,” environmental degradation, land erosion, loss of “natural heritage,” and more. Indeed, many similar meta-terminologies certainly circulate to provide a basis for continued regulation and the employment of regulators.

Policy think tanks actually help push the same agenda, even if unwittingly. For instance, studies that find present regulatory echelons to be inefficient or ineffective will be, at least in part, strategically heralded by planners. They can be expected to make opportunistic appeals to the public for larger budgets by blaming regulatory shortcomings on underfunding and lack of personnel. Accordingly, many Chicago School and Virginia School economists, famous for their criticisms of regulation on the grounds of its inefficiencies, may paradoxically find (to their chagrin) that their studies are being used to augment regulation rather than replace it with market-based alternatives.

References

Adams, A., Cherchye, L., De Rock, B. & Verriest, E., 2014, ‘Consume Now or Later? Time Inconsistency, Collective Choice, and Revealed Preference’, American Economic Review 104(12), December, 4147-4183.

Berns, G.S., Laibson, D. & Loewenstein, G., 2007, ‘Intertemporal Choice—Toward an Integrative Framework’, Trends in Cognitive Sciences 11(11), 482-488.

Böhm-Bawerk, E., 1890/1884, Capital and Interest: A Critical History of Economical Theory, Macmillan Company, London.

Boudreaux, D.J. & Ekelund, R.B., Jr., 1993, ‘The Cable Television Consumer Protection and Competition Act of 1992: The Triumph of Private Over Public Interest’, Alabama Law Review 44(2), Winter, 355-391.

Brown, J.R., Ivkovic, Z. & Weisbenner, S., 2015, ‘Empirical determinants of intertemporal choice’, Journal of Financial Economics 116(3), June, 473-486.

Buchanan, J.M., 1980, ‘Rent Seeking and Profit Seeking’, in Buchanan, J., Tollison, R. & Tullock, G., (eds.), Toward a Theory of The Rent-Seeking Society, Texas A&M University Press, College Station, Texas, 3-15.

Chen, M.K. & Schwartz, A., 2007, ‘Intertemporal Choice and Legal Constraints’, American Law and Economics Review 14 (1), 1-43.

Cobin, J., 2009, A Primer on Free Market Economics and Policy, Universal Publishers, Boca Raton, Florida.

Congleton, R.D., 2015, ‘The Logic of Collective Action and Beyond’, Public Choice 164(4), July 14, 217-244.

Coppin, C.A. & High, J.C., 1991, ‘Entrepreneurship and Competition in Bureaucracy: Harvey Washington Wiley’s Bureau of Chemistry, 1883-1903’, in High, J.C. (ed.), Regulation: Economic Theory and History, The University of Michigan Press: Ann Arbor, Michigan, 95-118.

Dasgupta, P. & Maskin, E., 2005, ‘Uncertainty and Hyperbolic Discounting’, American Economic Review 95(4), September, 1290-1299.

Deck, C. & Jahedi, S., 2015, ‘Time Discounting in Strategic Contests’, Journal of Economics & Management Strategy 24(1), March, 151-164.

DiLorenzo, T.J., 1985, ‘The Origins of Antitrust: An Interest-Group Perspective’, International Review of Law and Economics 5, 73-90.

DiLorenzo, T.J. & High, J.C., 1988, ‘Antitrust and Competition, Historically Considered’, Economic Inquiry 36, July, 423-435.

Dow, G.K. & Skillman, G.L., 2007, ‘Collective Choice and Control Rights in Firms’, Journal of Public Economic Theory 9(1), February, 107-125.

Fisher, I., 1930, The Theory of Interest, Macmillan Company, New York.

Friedman, M., 1957, The Permanent Income Hypothesis: A Theory of the Consumption Function, Princeton University Press, Princeton, New Jersey.

Gigerenzer, G., Todd, P.M. & the ABC Research Group, 1999, Simple Heuristics That Make Us Smart, Oxford University Press, Oxford, United Kingdom.

Grosse, R., 2012, ‘Bank Regulation, Governance, and the Crisis: A Behavioral Finance View’, Journal of Financial Regulation and Compliance 20(1), 4-25.

Haselton, M.G., Nettle, D. & Andrews, P.W., 2005, ‘The Evolution of Cognitive Bias’, in Buss, D.M. (ed.), The Handbook of Evolutionary Psychology, John Wiley & Sons Inc., Hoboken, New Jersey, pp. 724-746.

Hayek, F.A., 1945, ‘The Use of Knowledge in Society’, American Economic Review 35(4), September, 519-530.

Higgins, R.S. & Tollison, R.D., 1988, ‘Life Among the Triangles and Trapezoids: Notes on the Theory of Rent-Seeking’, in Rowley, C. Tollison, R. & Tullock, G., (eds.), The Political Economy of Rent-Seeking, Kluwer Academic Publishers, Boston, 147-157.

High, J.C. & Coppin, C.A., 1988, ‘Wiley and the Whiskey Industry: Strategic Behavior in the Passage of the Pure Food Act’, Business History Review 62, 286-309.

Hirshleifer, D., 2015, ‘Behavioral Finance’, Annual Review of Financial Economics 7, 133-159.

Holcombe, R.G., 1995, Public Policy and the Quality of Life: Market Incentives Versus Government Planning, Greenwood Press, Westport, Connecticut.

Ishikawa, M. & Takahashi, H., 2010, ‘Overconfident Managers and External Financing Choice’, Review of Behavioral Finance 2(1), April 21, 37-58.

Jappelli, T. & Pistaferri, L., 2006, ‘Intertemporal Choice and Consumption Mobility’, Journal of the European Economic Association 4(1), March, 75-115.

Kahneman, D., 2003, ‘Maps of Bounded Rationality: Psychology for Behavioral Economics’, American Economic Review 93(5), December, 1449-1475.

Kahneman, D. & Tversky, A., 1979, ‘Prospect Theory: An Analysis of Decision under Risk’, Econometrica 47(2), March, 263-292.

Kaufmann, K. & Pistaferri, L., 2009, ‘Disentangling Insurance and Information in Intertemporal Consumption Choices’, American Economic Review 99(2), May, 387-392.

Lichtenstein, S., Fischoff, B. & Phillips, L.D., 1982, ‘Calibration of probabilities: The state of the art to 1980’, in Kahneman, D., Slovic, P. & Tversky, A. (eds.), Judgment Under Uncertainty: Heuristics and Biases, Cambridge University Press, London, 306-334.

Lipsey, R.G. & Lancaster, K., 1956, ‘The General Theory of Second Best’, Review of Economic Studies 24(1), 11-32.

Loewe, G., 2006, ‘The Development of a Theory of Rational Intertemporal Choice’, Analytical Sociology Theory 80, 195-221.

Malkiel, B., Mullainathan S. & Stangle, B., 2005, ‘Market Efficiency Versus Behavioral Finance’, Journal of Applied Corporate Finance 17(3), June, 124-134.

Markussen, T., Reuben, E. & Tyran, J.R., 2014, ‘Competition, Cooperation and Collective Choice’, The Economic Journal 124 (574), February 1, F163-F195.

Modigliani, F., 1966, ‘The Life Cycle Hypothesis of Saving, the Demand for Wealth and the Supply of Capital’, Social Research 33(2), 160-217.

Muradoglu, G. & Harvey, N., 2012, ‘Behavioural Finance: The Role of Psychological Factors in Financial Decisions’, Review of Behavioral Finance 4(2), November, 68-80.

Maymin, P.Z., 2011, ‘Behavioral Finance Has Come of Age’, Risk and Decision Analysis 2(3), January, 125.

McChesney, F.S., 1987, ‘Rent Extraction and Rent Creation in the Economic Theory of Regulation’, Journal of Legal Studies 16, January, 101-118.

Minton, E.A. & Kahle, L.R., 2013, Belief Systems, Religion, and Behavioral Economics: Marketing in Multicultural Environments, Business Expert Press, New York.

Mises, L., 1966/1949, Human Action: A Treatise on Economics, Contemporary Books, Chicago.

Mitchell, W.C. & Simmons, R.T., 1994, Beyond Politics: Markets, Welfare, and the Failure of Bureaucracy, Westview Press: San Francisco, California.

Nagy, B., 2010, ‘Hyperbolic Discounting and Economic Policy’, Review of Economic Perspectives 10(3), 71-86.

Nocke, V. & Peitz, M., 2003, ‘Hyperbolic Discounting in Secondary Markets’, Games and Economic Behavior 44, 77-97.

Noor, J., 2011, ‘Intertemporal Choice and the Magnitude Effect’, Games and Economic Behavior 72, 255-270.

North, D.C., 1992, ‘Institutions and Economic Theory’, American Economist 36(1), Spring, 3-6.

Olson, M., 1971/1965, The Logic of Collective Action: Public Goods and the Theory of Groups, Harvard University Press, Cambridge, Massachusetts.

Plott, C.R. & Smith, V.l. (eds.), 2008, Handbook of Experimental Economics: Results, North-Holland, New York.

Rae, J., 1905/1834, The Sociological Theory of Capital, McMillan Company, London.

Rauch, J. 1996, ‘Eternal Life: Why Government Programs Won’t Die’, Reason 28(4), August-September, 17-21.

Rubinstein, A. (2003), ‘Economics and Psychology? The Case of Hyperbolic Discounting’, International Economic Review 44, 1207-1216.

Shiller, R.J., 2003, ‘From Efficient Markets Theory to Behavioral Finance’, Journal of Economic Perspectives 17(1), Winter, 83-104.

Shleifer, A., 1999, Inefficient Markets: An Introduction to Behavioral Finance, Oxford University Press, New York.

Shughart, W.F., 1990, Antitrust Policy and Interest-Group Politics, Quorum Books, New York.

Simmons, R.T., 2012, Beyond Politics: The Roots of Government Failure, Independent Institute, Oakland, California.

Simon, H.A., 1987, ‘Behavioral Economics’, in Durlauf, S.N. & Blume, L.E. (eds.), The New Palgrave Dictionary of Economics, 2nd Edition, 221-224.

Simon, J., 1996, The Ultimate Resource 2,Princeton University Press, Princeton, New Jersey.

Smith, A., 1904/1776, An Inquiry into the Nature and Causes of the Wealth of Nations, Methuen & Company Ltd., London.

Smith, V.L., 1962, ‘An Experimental Study of Competitive Market Behavior’, Journal of Political Economy 70(2), 111-137.

Smith, V.L., 1976, ‘Experimental Economics: Induced Value Theory’, American Economic Review 66(2), 274-279.

Smith, V.L., 1982, ‘Microeconomic Systems as an Experimental Science’, American Economic Review 72(5), 923-955.

Smith, V.L., 2000, Bargaining and Market Behavior: Essays in Experimental Economics [1990-98], Cambridge University Press, New York.

Smith, V.L., 2008, ‘Experimental Economics’, in Durlauf, S.N. & Blume, L.E. (eds.), The New Palgrave Dictionary of Economics, 2nd Edition, 120-136.

Stigler, G.J., 1971, “The Theory of Economic Regulation,” The Bell Journal of Economics and Management Science 2(1), Spring, 1-21.

Thaler, R., 1981, ‘Some Empirical Evidence of Dynamic Inconsistency’, Economics Letters 8, 201-207.

Tollison, R.D. & Wagner, R.E., 1991, ‘Romance, Realism, and Economic Reform’, Kyklos 44(1), 57-70.

Tullock, G., 1993, Rent Seeking, The Shaftesbury Papers, 2, Edward Elgar, Brookfield, Vermont.

Tullock, G., 1988, Wealth, Poverty, and Politics, Basil Blackwell, New York.

Tversky, A. & Kahneman, D., 1974, ‘Judgments Under Uncertainty: Heuristics and Biases’, Science 185(4157), 1124-1131.

Tversky, A. & Kahneman, D., 1992, ‘Advances in prospect theory: Cumulative representation of uncertainty’, Journal of Risk and Uncertainty 5(4), 297-323.

Vis, B., 2011, ‘Prospect Theory and Political Decision Making’, Political Studies Review 9(3), September, 334-343.

Cite This Module

To export a reference to this article please select a referencing style below: