Economic Growth & Development Lecture

Learning Outcomes

To be able to:

- Define and distinguish between economic growth, economic well-being and economic development

- To examine the cause of fluctuations in economic growth

- Outline the determinants of economic growth in the short and long run

- Understand the Solow growth Model

- Understand Endogenous growth theory

1.0 Introduction

Economic growth is the inflation-adjusted increase of the final market value of all goods and services produced in an economy over time. The common statistical measure used is GDP (gross domestic product), which is adjusted by an index of prices for the country in question. The adjustment is made in order to eliminate distortions in GDP caused by higher nominal money prices paid for inputs. Nominal prices differ from real prices in that the former reflect the amount of fiat or paper currency required to purchase an input, whereas the latter reflect the real subjective valuations of consumers based on supply and demand.

Thus, the adjustment process attempts to change all nominal GDP values to real values so as to make useful comparisons over time. The rate of economic growth is the percentage change in real GDP between any two points in time. Economic growth due to more efficient use of inputs is called intensive growth, whereas growth caused by the expansion of available inputs is called expansive growth.

This chapter will outline how GDP is used as a measure of economic growth. In section 2, we look at short term economic growth, the causes of fluctuations in the short term growth rates and this will be linked to the business cycle. Section 3 will examine the key determinants of long run economic growth. In this section we find out that a country’s capacity to produce must increase. So, we will be looking at the supply side of economics (human capital and technology). This will lead us to the introduction of the Solow growth model in order to examine the effects of technology and population growth on the economy. We look at Endogenous growth theory, and here the AK model of economic growth is introduced in section 5. Section 6 defines economic development and explores the other growth and development determinants. The next two sections consider the costs and benefits of economic growth. Lastly, we distinguish between developed and underdeveloped countries.

Need Help With Your Economics Essay?

If you need assistance with writing a economics essay, our professional essay writing service can provide valuable assistance.

See how our Essay Writing Service can help today!

2.0 Measuring economic growth: GDP

The three ways of measuring GDP

- Product method

- Income method

- Expenditure method

Real GDP is GDP measured at current prices whereas Nominal GDP takes into account inflation (it is GDP measured in constant prices).

GDP and Purchasing Power Parity

Countries are usually classified as “more” or “less” developed based on their GDP per capita, specifically considering their “purchasing power parity” (PPP) level. The PPP adjustment takes into account the exchange rates of different currencies when buying goods. In other words, real GDP differences between two countries can change dramatically when taking into account the cost of living in each country. Switzerland and Norway with very high per capita GDPs (84,000 USD and 101,000 USD respectively) and even moderately high GDP places like Hong Kong (38,000 USD) and perhaps New Zealand (41,000 USD) are extremely expensive in terms of cost of living relative to other (more or less) developed countries like Estonia (27,000 USD), Turkey (20,000 USD) or Chile (16.000 USD).

A person earning the equivalent of 100,000 USD in Chile, for instance, will have a substantially different cost for basic goods than his counterpart earning the same amount in Norway, such that the person in Chile might live in the same social class as that counterpart if he earned, say, only half as much. Therefore, the purchasing power parity adjustment is used to make country comparisons more accurate and realistic. This comparison provides important information to multinational firms making salary and other budget decisions for overseas divisions.

3.0 Short term economic growth

Before we examine the causes of economic growth, it is imperative that we distinguish between actual and potential growth and define the output gap.

Definitions:

- Actual growth is the percentage annual increase in national output actually produced.

- Potential growth refers to the speed at which the economy could grow. It is the % annual increase in the capacity of the economy to grow.

- Potential output refers to the sustainable level of output that could be produced in an economy. The difference between actual and potential output/GDP is referred to as the output gap.

Discussion points

- If an economy grows, at what speed and for how long can it continue to increase before it runs into inflationary problems?

- What minimal growth percentage should be achieved to avoid surging unemployment?

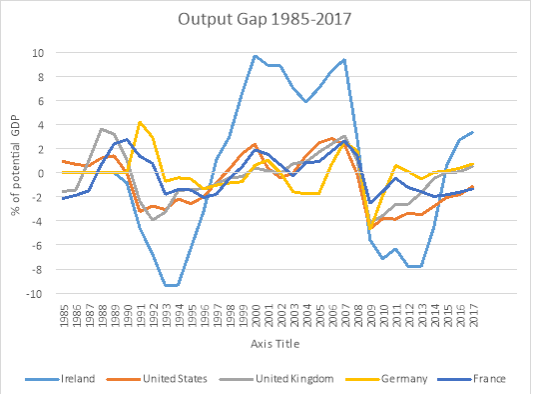

Figure 1: Economic Outlook: The output gap (deviations of actual GDP from potential GDP as % of potential GDP) of selected industrialised economies on the course of 1985 to 2017. Data extracted from OECD Statistics.

If the actual output/production is lower than the potential output (negative gap), there will be a greater than natural level of employment as organisations and companies are operating below their routine/normal level of capacity utilization. There will nonetheless be a downward pressure on inflation coming about because of a lower than normal level of demand. If the actual output is over the potential output (positive gap), there will be excess demand and an ascent in inflation.

Customarily, the gap is positive in a boom and negative during a recession (following the span of the business cycle).

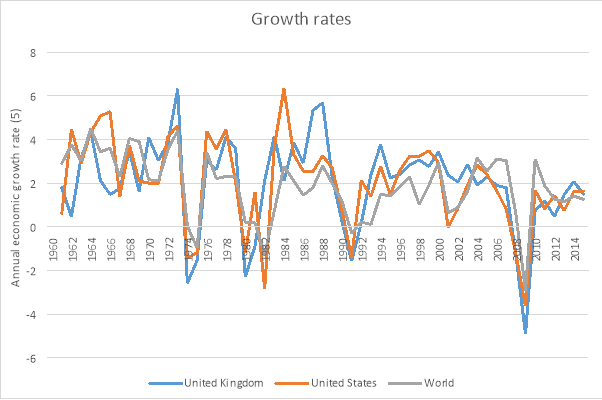

Figure 2: The growth rates in UK, USA and the world over the course of the last five decades. Data extracted from WorldBank

The business cycle is the upward and downward movements of levels of GDP and alludes to the period of expansions and contractions in the level of economic activities around a long haul development pattern. Figure 1.2 plots growth rates of the UK, USA and the World on the vertical axis, and from doing so, the cycles are clearly discernable.

Causes of fluctuations in actual growth

In the short run, fluctuations in growth rate can be attributed to variations in the growth of aggregate demand (AD)

Aggregate demand is the total demand for goods and services in an economy at a given time. AD constitutes of Consumption, Investment, Government Spending and Exports minus Imports

AD= C+I+G+X+M

- Consumption – An increase in consumption will lead to firms increasing their output. However, it is important to note that without an increase in real earnings brought about from increased productivity, an economic boom on the back of consumption will be an illusion. For example, in the USA an expansion in credit promoted binge buying and an imaginary wealth effect. Furthermore, it has also been argued that economic growth is the cause of increased consumption, and not the other way round.

- Investment – An increase in investment can lead to increased labour productivity. Investment could be in human capital or technology, which will both be discussed later on as causes of economic growth in the long run.

- Government spending - includes all government investment, consumption, and transfer payments in order to correct market failures, achieve supply side improvements and more.

- Net trade – GDP will increase when the total value of foreign goods and services that domestic producers sell to foreigners surpasses the total value of goods and services that domestic households purchase (trade surplus).

On the whole, a rapid increase in AD will create shortages, which tends to lead firms to increase their output. Consequently, there is less slack in the economy. Aggregate demand and actual out therefore fluctuate together in the short run (Low aggregate demand equals a recession and high aggregate demand equals a boom period). However, in the long run, a rapid rise in aggregate demand components is not sufficient to ensure a continuing high level of growth over several years.

4.0 Long Term Economic Growth

Discussion Points

Q: So, how can economies ensure a continuing high level of growth over a number of years?

A: Well, potential output has to increase. If potential output does not rise, actual output will only rise up to a certain level before spare capacity is used up.

Q: This leads us to our examination of the determinants of economic growth in the long run. How can potential output be increased?

A: Through supply side economic i.e. Improvements in labour and capital productivity

Impact of Population, Immigration, Human Capital and the Human Mind on Development

There are sociological factors that could play a role in development. For instance, the stability of marriage and the nuclear family, as well as literacy rate could lead to reduced economic costs.

Population growth is also fundamentally necessary for economic growth, since the human mind is the “ultimate resource” (Simon 1996) that solves human problems, relieves human misery, improves technology, augments food production and medical care, and betters the quality of life. There is no natural resource that rises to the same level of importance as the mind.

On the same score, economists view immigration as a boon to economic growth, especially adult immigrants, since the most expensive social costs of human preparation and development occur during the first twenty years of life. However, while immigration is a boon for the receiving country, it usually lowers grown the country emigrated from (Bildirici, et al 2005).

The increase in problems caused by more people is more than offset by the value of the increase in human minds, especially those minds which engender world-changing ideas. Consider the impact of William Shakespeare, William Wilberforce, Isaac Newton, Thomas Jefferson, Benjamin Franklin, Alexander Graham Bell, Thomas Edison, Henry Ford, Nicola Telsa, Albert Einstein, Orville and Wilbur Wright, Blaise Pascal, Bill Gates and Steven Jobs.

Human Capital

Theodore Schultz expounded the term human capital in the early 60’s to reflect the value of human capacities which were invested through expenditure in education, health and training that will lead to an improvement in the quality and level of production (Schultz 1961). He wrote that human capital was the factor most likely to limit growth.

The human capital augmented Solow growth model

Y(t) = K(t)aH(t)b(A(t)L(t))1-a-

In this Cobb-Douglas production function type based on Solow model (The Solow model is introduced in this chapter below, H is the stock of human capital, which is believed to have a significant impact on the level of economic growth.

Technology

There are a number of ways technology can improve economic development. Some of them are described below:

- Emergence of new services and industries – For example, information and communications technology has enabled the rise of a totally new sector: the app industry.

- Direct job creation – The information and communications technology industry is, and is anticipated to carry on being one of the largest employers.

- Business innovation – More than 95% of business in OECD countries have an online presence. Information and communications technologies have helped firms boost efficiency and improve their business processes.

The problem of diminishing returns

Assuming that a single factor of production expands in supply at the same time other stay fixed, diminishing returns will set in. For example, assuming that the amount of capital increases with no increases in other factors of production, there will be diminishing returns to capital. In other words, the rate of return to capital will fall. Unless the sum components of production increase, therefore, the rate of development/growth is prone to slow down. It is not sufficient that capital and labour increase if there is a constrained supply of land and raw materials.

4.1 Economic Growth without technological progress

Solow Growth Model

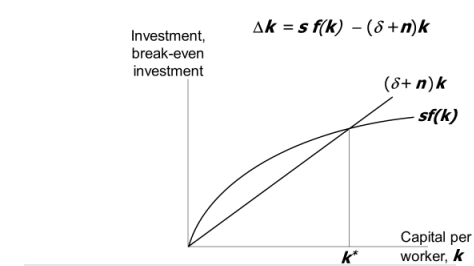

The Solow Growth Model (Solow 1956) shows how growth can occur from individual savings, investment and productivity, assuming a closed economy with no government expenditure affecting GDP (y = c + i). Since people save, then c = (1 – s) y, where s is the amount saved. People consume all that they do not save, which net consumption directly affects GDP, since i = sy. In the model’s production function, y =  , as capital (k) per worker rises, output per worker (y) also rises. However, it does so at a decreasing rate since capital will have a diminishing marginal product. Thus, investment is related to capital and savings, i = s.

, as capital (k) per worker rises, output per worker (y) also rises. However, it does so at a decreasing rate since capital will have a diminishing marginal product. Thus, investment is related to capital and savings, i = s.

The Solow Growth Model is dynamic, where the stock of capital changes over time and, thus, output changes over time (given that capital is the input). Capital per-worker is equal to the increase in new capital (investment or i) minus the depreciation of existing capital (d). Mathematically, ∆k = i – d = s – δk, where δ denotes the depreciation rate and ∆ denotes the change. This is the fundamental equation for the Solow Growth Model. The “steady state” version of the model, where new capital injections equal capital depreciation, denoted as k*, the ∆k = 0, since s

– δk, where δ denotes the depreciation rate and ∆ denotes the change. This is the fundamental equation for the Solow Growth Model. The “steady state” version of the model, where new capital injections equal capital depreciation, denoted as k*, the ∆k = 0, since s – δk* = 0. In this state, there is no economic growth in per-worker output. See figure 3.

– δk* = 0. In this state, there is no economic growth in per-worker output. See figure 3.

Implications of the Solow Growth Model for Economic Growth

Interestingly, with low amounts of initial capital, its depreciation will be a small factor if large inputs of new capital are added, on account of its large marginal product, economic growth will be faster. This is precisely what happens when capital is invested in developing countries compared to more developed ones: growth rates are higher and growth is faster. Moreover, higher rates of savings are equated with higher growth rates, at least in the short run, since in the long run higher savings will mean less consumption (thus affecting a country’s output). Therefore, there is a trade-off between savings and current consumption (affecting output). The point at which the marginal product of capital equals the depreciation rate is known as the golden rule level of capital.

Figure 3: Solow Model Diagram

With the Solow Growth Model, long term economic growth cannot be sustained without population and labor force growth, n. In the steady state scenario, population growth, capital per worker and output per worker are constant. However, as n changes, capital per worker and output per worker will change by n as well. Thus, there is a direct effect on total output, but output per worker (i.e., his individual standard of living) remains unknown.

Economic growth with technological progress

The next step in applying the Solow Growth Model comes from allowing for technological progress, i.e. permitting the efficiency of labor to increase. An increase in labor productivity has the same effect on economic growth as increasing population. Thus, after some heavy mathematics which introduce technological efficiency into capital and output, the model’s growth equation becomes ∆k = s– (δ + g + n) k. Therefore, in this model, also called the Solow-Swan model (Swan 1956), economic growth is a function of population increase, savings, capital investment and technological efficiency or productivity. Furthermore, it is thus considered to be an exogenous growth model, since grow depends on external factors.

5.0 Endogenous Growth Theory

Endogenous growth theory suggests that knowledge, innovation and increases in personal productivity through education and perfection of technological skills or processes are significant contributors to economic growth. Moreover, positive externalities or spillover effects in the information age’s advanced economies will lead to economic development. This theory affirms that the long run growth rate of an economy will depend on public policy choices, such as well-placed subsidies for research and development and for education, thus increasing the incentive for innovation.

The AK Model

The most common endogenous growth model is the “AK model,” which features the absence of diminishing returns to capital. A simple AK production function is: Y = AK, where A is a positive constant reflecting the level of technology and K includes human and all other capital, and y = A k is the output per capita. If {\displaystyle {\frac {f(k)}{k}}=A\,}  is substituted in the Solow-Swan Model equation, where is the output function per worker, an economy’s per capita income converges toward its steady-state value. Thus, the growth rate will be given by y = s

is substituted in the Solow-Swan Model equation, where is the output function per worker, an economy’s per capita income converges toward its steady-state value. Thus, the growth rate will be given by y = s – (

– ( + δ) {\displaystyle y=Ak\,}= s

+ δ) {\displaystyle y=Ak\,}= s – ( + δ), which also permits economic growth without exogenous technological change. Yet, technology can yield long-run per capita growth apart from any exogenous technological development, depending on the savings rate and population growth.

– ( + δ), which also permits economic growth without exogenous technological change. Yet, technology can yield long-run per capita growth apart from any exogenous technological development, depending on the savings rate and population growth.

In neoclassical growth models, the long-run growth rate is exogenously determined by either the savings rate, as in the Harrod–Domar model (Harrod 1939; Domar 1946) or the rate of technical progress, as in the Solow Growth Model. Endogenous growth theory improves on neoclassical theories by building macroeconomic models with microeconomic foundations, where households maximize utility subject to budget constraints and firms maximize profits.

Implications of the AK Model for Economic Growth

Of key importance is the generation of new technologies and labor productivity for efficiency. More advanced models consider spillover effects and positive externalities, benefits to third parties that do not pay for them, along with increases in varieties and qualities of goods.

Furthermore, endogenous growth theory implies that policies that foment openness, competition, change and innovation will promote economic growth. Conversely, rent seeking and policies that restrict or slow change by protectionism are likely to slow growth and disadvantage consumers.

Sustaining economic growth required a process of continual transformation, as has been seen in the wrenching changes, or “creative destruction” (as Schumpeter 1942, 1971, 2008 called it), since the Industrial Revolution. These painful alterations lead to long-term prosperity. Economies that cease to transform themselves are destined to stop growing and perhaps experience backwardness (Aghion 2004; Aghion & Howitt 1992).

Advances in Endogenous Growth Theory: Merger with the Theory of Entrepreneurship

Schumpeter rejected the neoclassical postulate that the entrepreneur is “an abstract figure assumed to be unaffected by the influences external to the rational operation of the firm he directed”; conversely, he viewed him as “the focal point and key to the dynamic of economic development and growth” (eds. Greenfield & Strickson 1986: 5). Moreover, he viewed the entrepreneur as different from mere businessmen on account of their flexibility, mobility, and creation of new inputs, although either group can invent new products (Schumpeter 1971: 54, 65).

For Schumpeter, the entrepreneur’s hallmark quality is that of a disequilibrating innovator.[1] In a developing economy, the process by which going concerns are knocked off by innovation is called creative destruction. Booms and busts are inevitable—impossible to correct without stunting the growth of wealth through innovation (Schumpeter 1942, 2008/1911). Boiled down to its core, by “creating disequilibrium” the entrepreneur performs “implementation and commercialization” (ed. Kent 1984: 3). And, his success depends on “the capacity of seeing things in a way which afterwards proves to be true, even though it cannot be established at the moment (1934: 85)” (O’Driscoll & Rizzo 1996: 68). Papanek modified Schumpeter, noting the importance of religious or ideological imperatives, e.g., as noted in Weber’s The Protestant Ethic and the Spirit of Capitalism (Papanek 1971/1962: 317, 318).

Kirzner further modified basic Schumpeterian theory saying, “it becomes difficult to see the processes of short-run resource allocation as anything but special cases of the more general discovery processes that constitute economic growth” (Kirzner 1973: 50). He simplified that perspective by earmarking three major types of entrepreneurial activity: “(1) arbitrage activity; (2) speculation activity; and (3) innovative activity” (Kirzner 1973: 52).

Need Help With Your Economics Essay?

If you need assistance with writing a economics essay, our professional essay writing service can provide valuable assistance.

See how our Essay Writing Service can help today!

6.0 Economic Development and the other determinants of growth and development

Economic development is a concept related to economic growth that has been utilized to characterize economic progress since the Industrial Revolution began in England around 1775. It is also called industrialization or modernization—sometimes even Westernization. It refers to the process by which a country improves the economic efficiency. Economic development is primarily a function of economic growth, although other factors are also important such as the level of pollution or contamination, safety from crime and natural disasters, drinking water purity, ability to meet medical, dental, shelter, clothing and food needs, along with institutions like the rule of law and access to education, plus adequate infrastructure, transportation and ample supplies of usable energy.

Other Factors Affecting Economic Development/Growth

Trade openness

It is a measure of economic policies that either limit or economic trade between countries. Trade liberalisation permits nations to specialise in producing the goods and services where they have a comparative advantage. This facilitates a net gain in economic welfare.

Impact of Rent Seeking on Development

Still other economists cite excessive rent seeking as a cause for underdevelopment (Tullock 1988, 1993; Simmons 2012), which can lead to a pernicious “transitional gains trap” (Tullock 1975) that makes the social costs from rent seeking permanent. Rent seeking would probably better be termed privilege seeking, since it entails firms acting to gain state-granted economic privileges through manipulation of democratic processes, such that the amount gained by the benefitted firm or industry is less than the social cost of such action.

The resulting loss from state-granted monopoly privileges and tariff barriers—and all attempts to create artificial scarcity or artificial demand for a good or service through legislation or executive decree—lowers social welfare and hence retards economic development. As a result, people pay higher, monopolized prices and, thus, have fewer opportunities for consumption given their budget constraints. The few benefit at the expense of the many.

Measuring the exact amount of rent seeking in a country is a daunting task, but oftentimes inferences can be made by looking at the number of patents issued, the amount of protectionist legislation enacted (e.g., import tariffs, taxi medallions) and the number of lobbyists or special interest (pressure) groups that exist.

Egalitarianism and Development

Many economists and other scholars believe that there is a link between development and income or wealth equality, such that “better” societies are more egalitarian. This view is normative and borders on breaking the economist’s cardinal rule of not making value judgements (which are always subjective). Nonetheless, these social scientists and analysts have created benchmarks and tools to assist them in making comparisons.

Inequality

Inequality might impair development if those with low incomes experience low productivity and poor health as result, or alternatively, as proof suggests, the poor battle to finance investments in education. Inequality might likewise undermine public confidence in growth boosting policies like free trade. The most widely-used factor is the Gini Coefficient, a statistical measure of a country’s income or wealth inequality, where a value of 0 means perfect equality and a value of 1, perfect inequality. This measure is frequently used to judge economic development, with lower coefficients being preferred. Among the thirty-five “developed” OECD countries, the Gini Coefficient ranges from 0.24 (Slovenia) to 0.5 (Chile). Nevertheless, there is reason to doubt the usefulness of the Gini Coefficient for public policy modification.

Case of Chile

For instance, since ousting communism in 1973, Chile has reduced abject poverty to under 5% and the middle class has expanded to encompass over 65% of the population, while the upper classes comprise between 10% and 15% of the total population. Incomes for nearly everyone have doubled and tripled (or more) in the last two or three decades.

Yet, Chile remains dominated by around twenty wealthy families, and has a disproportionate number of billionaires on the Forbes list that other countries close to its size, or in the Latin American region, making the Gini Coefficient rather high. Nevertheless, for the average Chilean that has risen far above what his grandparents or even parents could have ever dreamed of being, it makes little difference to them how many billions of dollars the few actually have, so long as they, too, are moving upwards.

This kind of upwardly-mobile disparity stands in stark contrast to countries like Brazil, South Africa, Indonesia, China, Russia or India, where an elite class maintains its wealth and power, while poorer people show little upward movement, and the middle class grows very slowly. Therefore, so long as the rate of growth of income or wealth for all social classes at the same time is significantly positive, the level of inequality between classes or groups is effectively superfluous and the Gini Coefficient loses relevance in terms of public policy implications.

Economic Freedom and Corruption Indices and Development

A better means to judge prosperity and economic development might be the now-famous indices of economic freedom and corruption perception produced annually by the Heritage Foundation (Washington), the Fraser Institute (Vancouver) and Transparency International (Berlin). The top twenty-five countries listed in each of these indices seems to be directly correlated with economic development, higher quality of life and general prosperity.

Sixteen countries that are in this top end of all three 2016 lists include (World Bank/CIA World Fact Book Gini Coefficient for incomes in parentheses): Hong Kong (n.d./.537), Switzerland (.316/.287), Singapore (n.d./.464), New Zealand (.362/.362), Denmark (.291/.248), Canada (.337/.321), Australia (.349/.303), Ireland (.325/.339), Chile (.505/.521), Luxembourg (.348/.304), Finland (.271/.268), Netherlands (.280/.251), United Kingdom (.326/.324), United States (.411/.450), Estonia (.332/.329) and United Arab Emirates (n.d./n.d.). Probably no one is surprised that these countries made the grade.

If the group is extended to the top forty places in one ranking and top twenty-five in the other two, these countries are added to the list: Taiwan (n.d./.338), Czech Republic (.261/.249), Sweden (.273/.249), Norway (.259/.268), Germany (.301/.270) and Japan (.321/.379). Lithuania (.352/.355), Mauritius (.358/.359) and Georgia (.400/.460) come in with honourable mention.

All of these twenty-five countries have relatively high per capita GDPs and cultures or institutions that foment low corruption and thus lower transactions costs. Interestingly, Hong Kong, Singapore, the United States, Chile and Georgia all have relatively high Gini Coefficients, yet they are often included among the most desirable places to live in the world, underscoring the weakness of the measure.

Can one conclusively say that the six countries listed above with the lowest Gini Coefficients (Denmark, Netherlands, Finland, Czech Republic, Sweden and Norway) are clearly better than their higher Gini coefficient counterparts? Would the general consensus of people in any of the top twenty-five countries listed register overall economic dissatisfaction? We do not live in paradise. Yet, people in these countries enjoy a relatively high standard of living and quality of life than most other places in the world. Chileans, for instance, tend to stop complaining so much about the relative quality of life they enjoy after visiting Nigeria, India, Cuba, Haiti and other countries of the developing world.

The role of institutions

For economists, finding the best institutions “matters” a great deal (North 1992), since lower costs of social cooperation and doing business tend to lead to greater economic growth and development. Although it is not usually politically correct to say that one culture or practice is better (i.e., more efficient) than another, economics, as value-free science, has no trouble ranking economic systems based on the efficiency of relative cultural and institutional virtues or defects.

Thus, in terms of economic development and efficiency, economists would have no problem saying something like, “Western Civilization is superior to other world civilizations” or “capitalism is superior to socialism or communism.” In so doing, they are not passing judgment on the values in other cultures or their practices. Unlike moral philosophers, economists do not find right or wrong in their analysis, but rather the relative efficiency or inefficiency, the expected costs and benefits, as well as whether there are more or less opportunities, greater or lesser uncertainty, and how the relative quality of life is affected or generated by cultural institutions and practices.

7.0 Entrepreneurship

Definition and the Alertness Concept

Business school academics (e.g., Drucker 1985) often differ with economists in their understanding of the entrepreneur. A simple definition often cited is: an entrepreneur is a businessman who is never hired, who cannot be fired, and is the residual claimant (i.e., he receives the profits or losses of his enterprise). Plus, many business schools offer MBA programs where they purport to train people to be entrepreneurs.

Economists go beyond the simple definition (and training programs) of these academic colleagues. An entrepreneur is more than just a businessman or an innovator. The entrepreneur possesses in his brain an extraordinary quality of “alertness” (Kirzner 1973: 85-86) and thus can see an opportunity for future profit, correctly predict the demand of consumers, and successfully market his good or service.

Environment Needed to Benefit from Entrepreneurial Minds

Both Mises (1966) and Hayek (1945) contend that the market’s price system is the only efficient means of allocating resources and engendering growth. Indeed, the market process requires competition that is analytically inseparable from entrepreneurial activity (Kirzner 1973: 9).

Moreover, knowledge is a key component of capital formation and technological efficiency in both exogenous and endogenous growth models. Yet, the great economic problem of society is that “the utilization of knowledge is not given to anyone in its totality” (Hayek 1945: 520), making Simon’s “ultimate resource” thesis clearly significant. Hence, human minds are essential for economic growth and development, and entrepreneurs have a special alertness gift—among other things—that makes them essential to knowledge discovery.

They thrive under free markets and institutions that guarantee strong property rights and rule of law (ed. Kilby 1971: 55), where “economic problems arise always and only in consequence of change” (Hayek 1945: 523), which in turn provide them with temporary monopoly profits. An entrepreneur uses his alertness “to discover and exploit situations in which he is able to sell for high prices that which he can buy for low prices” (Kirzner 1973: 48).

The Speculative Nature of Entrepreneurship Leads to Economic Growth and Development

Progressive entrepreneurial action yields efficient and effective resource allocation, which in turn promotes economic growth and development. Entrepreneurs notice maladjusted prices before others do and engage in arbitrage. Their profits are realised when their judgement of the future correctly determines what are undervalued inputs of production. Indeed, in a sea of uncertainty, the speculative nature of entrepreneurship is inherent in all entrepreneurial action.

Yet, what appears risky to onlookers, is far less so to the entrepreneur on account of his alertness (Kirzner 1973: 85-86). They have something that normal people do not have: superior “mental power and energy [and] are the leaders on the way toward material progress” (Mises 1966: 336).

They are characterized by dynamic abilities to react to change, correctly foresee future demand, and subordinate other interests in order to effectively serve consumers.

8.0 The benefits of economic growth

- Increased consumption – Given that economic development overtakes population growth, it will prompt higher income per head. This might prompt higher levels of consumption of goods and services. Assuming that mankind's welfare may be identified with the level of consumption, then economic growth presents a clear gain on the public arena.

- Makes it easy to redistribute incomes to the poor – If incomes increase, the government can readjust incomes from the rich to the poor without the rich losing. For example, as peoples' incomes increase, they will naturally pay more taxes. These additional revenues might be a chance for the government to lessen poverty.

- Avoid macroeconomic problems – Individuals aim to have higher living standards. If wage demands do not match productive potential - there will be inflationary pressures, industrial disputes, worse balance of payments crises (as individuals import more) et cetera. Thus, growth in the productive potential aids individuals to meet these aims and avoid macroeconomic crises.

9.0 The costs of economic growth

Opportunity costs

In order to attain faster growth, firms will presumably require to invest more. This will require financing, which can come from higher taxes, higher retained profits or savings. All these options constrain consumption meaning there will be a reduction in consumption. In the short run, accordingly, higher growth leads to less consumption.

Environment

The higher the level of consumption-led growth, the higher likely to be the level of waste and furthermore, contamination from pollution. If an increase in capital and labour prompts a more intensive utilisation of natural resources and land, the emerging growth in output may be environmentally unsustainable.

Social Effects, Economic well-being and Happiness economics

It could be contended than an over the top quest for material growth by a nation can lead to a more selfish, greedier and less caring society. As communities become more industrialised, suicides, violence, divorcees, crime and different stress related sicknesses may prevail. By comparison, a life that is less materialistic may be more fulfilling. Gross national happiness is a term coined in the 1970's by His Majesty the Fourth King of Bhutan. The idea infers that sustainable development should take a comprehensive approach towards notions of progress and give equal importance to non-economic elements of well-being.

Economic welfare is a more extensive measure of well-being (economic + social). Numerous parts of well-being are not material aspects of life. Welfare measures incorporate median incomes and inequality. In other words, the measure of well-being goes beyond the level or rate of growth of GDP

10.0 Developed Versus Underdeveloped Countries

Note that in common terminology, economists talk about developed countries and less developed, underdeveloped or developing countries. Previously, stemming from the division between capitalist and communist countries during the Cold War, the world came to be divided into (1) the “First World” (the United States, Canada, Western Europe, Israel, Australia, New Zealand, Hong Kong, Singapore, Taiwan, Japan and South Korea), (2) the “Second World” (the Soviet Union and its communist satellites, and perhaps China, North Korea, Vietnam and other progressive socialist countries) and (3) the “Third World” (all other unaligned, poor countries of the Caribbean, Latin America, Africa and Asia).

Lines of demarcation change over time. For instance, Argentina moved from being wealthy (what would have been called a First World country) in the early Twentieth Century to being a mediocre and perhaps Third World country by the turn of the Twenty-First Century, while Chile, South Korea and South Africa have over the same period moved from being what would have been called the Third World to the First World, at least for larger population centers.

All Third World countries have nicer sections where the wealthy live, such as in Nigeria, China and Brazil. However, the great majority of the population is impoverished. What set apart Chile, South Korea and (to a lesser extent) South Africa was the development of a significant middle class—people with disposable personal income, acquisitive power and the ability to save. Nowadays, this tripartite paradigm is being less utilized by professional academics, but one will still find it in the literature.

11.0 References

Aghion, P., 2004, ‘Growth and Development: A Schumpeterian Approach’, Annals of Economics and Finance 5, 1-25.

Aghion, P. & Howitt, P., 1992, ‘A model of growth through creative destruction’, Econometrica 60(2), 323–351.

Bildirici, M., Orcan, M.S., Sunal, S. & Aykaç, E., 2005, ‘Determinants of Human Capital Theory, Growth and Brain Drain: An Econometric Analysis for 77 Countries’, Applied Econometrics and International Development 5(2), 109-140.

Domar, E., 1946, ‘Capital Expansion, Rate of Growth, and Employment’, Econometrica 14(2), 137-147.

Drucker, P.F., 1985, Innovation and Entrepreneurship, Harper & Row Publishers, New York.

Greenfield, S.M. & Strickson, A. (eds.), 1986, Entrepreneurship and Social Change, University Press of America, New York.

Harrod, R. 1939, ‘An Essay in Dynamic Theory’, The Economic Journal 49(193), 14–33.

Hayek, F.A., 1945, ‘The Use of Knowledge in Society’, American Economic Review 35(4), September, 519-530.

Kent, C.A. (ed.), 1984, The Environment for Entrepreneurship, Lexington Books, Lexington, Massachusetts.

Kilby, P. (ed.), 1971, Entrepreneurship and Economic Development, The Free Press, New York.

Kirzner, I.M., 1973, Competition and Entrepreneurship, University of Chicago Press, Chicago.

Kirzner, I.M., 1989, Discovery, Capitalism, and Distributive Justice, Basil Blackwell, New York.

Kirzner, I.M., 1992, The Meaning of Market Process: Essays in the Development of Modern Austrian Economics, Routledge, New York.

Mises, L., 1966/1949, Human Action: A Treatise on Economics, Contemporary Books, Chicago.

North, D.C., 1992, ‘Institutions and Economic Theory’, American Economist, Spring, pp. 3-6.

O’Driscoll, Jr, G.P. & Rizzo, M.J., 1996, The Economics of Time and Ignorance, Routledge, New York.

Papanek, G.F., 1962, ‘The Development of Entrepreneurship’, American Economic Review 52(2), May, 45-58.

Schumpeter, J.A., 1942, Capitalism, Socialism, and Democracy, Harper & Brothers, New York.

Schumpeter, J.A., 1971, ‘The Fundamental Phenomenon of Economic Development’, in P. Kilby (ed.), Entrepreneurship and Economic Development, 62-94, The Free Press, New York.

Schumpeter, J.A., 2008/1911, The Theory of Economic Development: An Inquiry into Profits, Capital, Credit, Interest and the Business Cycle, transl. R. Opie, Transaction Publishers, London.

Simmons, R.T., 2012, Beyond Politics: The Roots of Government Failure, Independent Institute, Oakland, California.

Simon, J., 1996, The Ultimate Resource 2,Princeton University Press, Princeton, New Jersey.

Solow, R.M., 1956, ‘A Contribution to the Theory of Economic Growth’, Quarterly Journal of Economics 70(1), February, 65–94.

Swan, T.W., 1956, ‘Economic growth and capital accumulation’, Economic Record 32(2), November, 334–361.

Tullock, G., 1975, ‘The Transitional Gains Trap’, The Bell Journal of Economics 6, Autumn, 671-678.

Tullock, G., 1988, Wealth, Poverty, and Politics, Basil Blackwell, New York.

Weber, M., 1958/1904-5, The Protestant Ethic and the Spirit of Capitalism, transl. T. Parsons, Charles Scribner & Sons, New York.

[1] Schumpeter’s five cases where entrepreneurial innovation occurs (ed. Kent 1984: 3) are: (1) The introduction of a new good or of a new quality of good, (2) the introduction of a new method of production, (3) the opening of a new market, (4) the conquest of a new source of supply of raw materials, and (5) the carrying out of new organisation of any industry.

Cite This Module

To export a reference to this article please select a referencing style below: