Case Study of China Aviation Oil Corporation Ltd

| ✅ Paper Type: Free Essay | ✅ Subject: Finance |

| ✅ Wordcount: 1264 words | ✅ Published: 04 Sep 2017 |

Risk Management and Corporate Governance

A Case Study of China Aviation Oil Corporation Ltd.

- Background

- introduction to CAO

China Aviation Oil (Singapore) Corporation Ltd (CAO) is the Singapore subsidiary of China Aviation Oil. CAO was established in 1993 and its main business were jet fuel (kerosene) purchase for Chinese airports and international trading of fuels. CAO developed really fast and achieved 92% market share of the procurement of imported jet fuel for China’s civil aviation industry by 2001.

However, it was then involved in a big scandal which lead to its failure. In November 2004, CAO declared a total loss of $550 million and filed for bankruptcy.

- timeline of critical events

Q1 2003 – CAO enters into speculative option trades on oil prices with a bullish view

Q4 2003 – CAO changed its strategy and started trading speculative option trades taking a bearish view.

Oct 2004 †international oil prices rose steeply, leaving CAO facing significant margin calls on its open (short) derivative positions.

Nov 2004 – in a press release CAO stated it was unable to meet some of the margin calls arising from speculative derivative trades. The total derivative losses amounted to $550m.

Mar 2006 †CEO Mr. Chen Jiulin was arrested with the charge of insider trading, fined and sentenced to 51 months imprisonment.

- option-based strategies

There are two types of options: call and put option. One can either long or short the two options to gain profit (speculating) or mitigate risk(hedging) from price changes.

In this case, CAO started its option trading in 2002 initially to hedge its jet fuel risk thorough. derivatives of futures and swaps. However, in the mid 2003, CAO started trading in speculative derivative options.

- hedging

A hedge is needed to mitigate the risk from potential unfavorable swings in commodities. However, considering the cost and benefit effect, a hedge is not always necessary. One needs to understand the risks to be hedged, evaluate the severity and timing of downside risks properly, consider the financial instruments available and costs of certain instruments to determine the most cost-effective way to hedge.

- risk management and corporate governance

Risk management is the identification, assessment, and prioritization of risks followed by coordinated and economical application of resources to minimize, monitor, and control the probability and/or impact of unfortunate events or to maximize the realization of opportunities. Risks can come from various sources including uncertainty in financial markets, threats from project failures, legal liabilities, credit risk, accidents, natural causes and disasters, or uncertain events, etc.

The Board should establish appropriate guidelines for trading and ensured that they were consistent with the company’s fundamental risk management policies, management capabilities and expertise, and overall risk appetite and tolerance. Senior managers (including executive members of the board) should formulate the major policies and guidelines of an institution. There should be a separation of duties between those who generate financial risks and those who manage and control these risks.

- Analysis

- CAO’s trading strategies

- escalating bets

As mentioned above, the company’s trading strategy changing from hedging risks in 2002 to speculation with bullish strategy (bought calls and sold puts)in Q1 2003, which proved to be an accurate prediction. However, CAO then took a bearish view of the trend in oil prices in the fourth quarter of 2003, and began to sell calls and buy puts, with the result that it was in a short position at the end of the quarter. As the assumption was that oil prices would fall, it was further assumed that the counterparties would not extend the options, and these would therefore lapse to the benefit of the company. However, the price went further upward this time. The rise in oil prices resulted in the counterparties exercising the extendible features on options, and with the calls that were sold, the company faced the real risk of having to sell the contracted number of barrels at the strike price and realizing substantial loss.

- incorrect option valuation methodology

The Special Auditor from PwC assigned by SGX discovered that the company used the wrong MTM valuation method by ignoring the time value, which lead to the misestimation of oil price and the wrong speculation strategy. While CAO had the chance to remedy the mistake by comparing the pricing with counterparties’ but the company met the margin calls without protest until it lost the financial capacity to do so at the end of September 2004.

- motivations behind

Financial: the company developed fast and became monopoly in the market since 2000. In order to bolster its profile as well as boost investor’s confidence and generate more profit, the company was willing to take high risk.

Political: according to exhibit 8, the year 2003 saw the burst of Gulf War. The company may want to take advantage of the war so that higher risk is acceptable as fuel is a critical resource during wars.

Corporational: the lack of risk management knowledge of the CEO, insufficient management environment within the company and the inefficient external audit, as will be discussed in detail in the next section, further accelerated the fall of the big company.

- CAO’s risk management and corporate governance

In its 2003 annual report, CAO indicated that it had “a formal system of rigorous internal controls over three layers”. Meanwhile, other sources of control includes China Securities Regulatory Commission and External Audits. It seems that the company should have a stringent risk appetite.

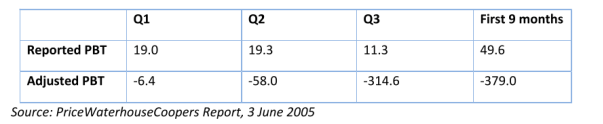

However, according to PwC’s report, despite a continuing significant loss in 2004, in order to avoid recording and reporting losses, the company adopted a much larger risk exposure by selling longâ€term options with extremely high risk profiles to raise the premiums to cover the cost of closing out the lossâ€making option contracts (Exhibit 1). So in effect, CAO coveredâ€up the losses that were realized when closing out the lossâ€making nearâ€dated options.

Exhibit 1

It was unclear why the company’s directors did not question or object to this contravention of regulations. The Audit Committee did not carry out its function of identifying and monitoring the financial risks involved in options trading, and investigating whether the risk management framework and safeguards were sufficient for dealing with the business.

- Follow-up Development

Restructuring outcome:

In response to the investigation results by PwC, CAO indicated in a press statement that it intended to form a committee to study the results and to recommend the company on specific remedial or disciplinary improvements. It also expressed the willingness to be more honest on past events and to move forward with the debt and equity restructuring exercise in a positive manner. The company then called for a creditor meeting to approve its latest debt restructuring plan on June 8.

As far as I am concerned, with the resources of the parent company, both from the aspects of finance and entrepreneurship, the support from Chinese government, and the establishment of a strict risk management framework, CAO can still gain back confidence from stakeholders, which may need time and effort.

- Conclusion

Improper application of accounting principles, lack of oversight, inadequate knowledge of market and ineffective risk management systems for the speculative options deal were the major contributing factors towards CAO’s failure. We should learn a lesson from the case as factors are similar and equally applicable to different business contexts so it is important to avoid certain mistakes.

- References

Li, S., & Nadeem, M. (2010). Risk Management and Internal Control: A case study of China Aviation Oil Corporation Ltd.

Farhan. (2016, April 10). China Aviation Oil (Singapore) Corporation Limited’s Jet Fuel Scandal (2005) – Casestudy. Retrieved January 15, 2017, from https://financetrainingcourse.com/education/2014/04/china-aviation-oil-singapore-corporation-limiteds-jet-fuel-scandal-2005-casestudy/

Yeo, A. (2014). China Aviation(Singapore) Limited- Sliding down a Slippery Slope: The $550m Derivative Trading Loss on November 2004.

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this essay and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal