Theories of Keynesian Economics

| ✅ Paper Type: Free Essay | ✅ Subject: Economics |

| ✅ Wordcount: 1164 words | ✅ Published: 20 Aug 2018 |

Origin

Keynesian economic is a macroeconomic model that used to identify the equilibrium level, and examine disruptions, total production and income. Equilibrium is when total production and income intersect with the total expenditures. The Keynesian model has three basic variations designated by several macroeconomic sectors such as two-sector, three-sector, and four-sector. Keynesian model also frequently presented in the form of injections and leakages in addition to the standard total expenditures format. Keynesian model used to study some important topics and issues such as multipliers, business cycle, fiscal policy, and monetary policy.

Keynesian model normally presented as the Keynesian cross-intersection between the total expenditures line and 45 degree line. The theory was the standard macroeconomics analysis since the Great Depression of early 1980s and throughout the mid-1900s. The theory still counting to provide important insight into the working of the macroeconomic despite cross-intersection was largely substituted by total market analysis which is measured by aggregate supply and aggregate demand.

Keynesian economics is established by John Maynard Keynes. The theory believe that total demand take an important role in business-cycle instability and recessions. Keynesian economics points to unrestricted government policies, especially fiscal policy as the key of stabilizing business cycle.

There are some basic principles of Keynesian economics such as the General Theory of Employment, Money and Interest in Keynes’ book, published in 1936. These principles has launched the modern study of macroeconomics and worked as a conductor for macroeconomic theory and macroeconomic policies for few decades.

Assumptions

There are three key assumptions of Keynesian economics. First assumption if rigid prices. Keynesian economics assumes that prices is inflexible, especially in the downward direction which can stop markets to reach equilibrium.

Next assumption is effective demand. Keynesian economics is according to concept of effective demand, the principle of consumption expenditures are due to disposable income that available from the household sector instead of income that available at full employment.

Lastly is saving and investment determinants. Keynesian economics also believes that interest rate would affected saving and investment. In addition, household saving is depend on household income and business investment is depend on the expected profitability of production.

Highlights

- Macroeconomic is a separate entity operating by its own principles and the standard of microeconomic market principles do not necessarily apply.

- Changes in total demand is the primary source that causes business-cycle instability.

- Markets do not reach equilibrium automatically, so full employment is not guaranteed.

- Persistent unemployment problems, including those taking place during the Great Depression, result due to lack of total demand.

- The method to sustain full employment is through government intervention, for example, government apply fiscal policy to changes government spending.

Four Macroeconomic Sectors

The foundation of the Keynesian model is built by the four macroeconomic sector including household, business, government, and foreign on their expenditures for total production. The four sectors are household, firms, government and foreign. Household sector refer to everyone in the economy; consumption expenditure refer to their expenses on production used for satisfaction.

Business sector refer to firms that produce output; investment expenditures refer to their expenses on capital goods.

Government sector refer to federal, state, and local government; government purchases refer to their expenses on production used to offer government services.

Foreign sector refer to all households, businesses, and government beyond the political boundaries of the domestic economy; net exports refer to their expenditure contribution.

Keynesian Equilibrium

Like most economic models, Keynesian model is mainly focus on equilibrium. In general, equilibrium is when the balance between opposing forces which remains unchanged as long as another force interferes. Equilibrium is when demand meet supply in the market. Demand force is consumers who normally looking for low price and supply force is sellers who normally demand high price. In the macroeconomic, equilibrium is a balance between total expenditures and total production.

There are particulars of equilibrium in the Keynesian model. Firstly, Keynesian equilibrium is a balance between total expenditures and total production. Total expenditures are the sum of expenditure on all four macroeconomic sectors. Total production is the sum of market value of all final goods and services.

Secondly, the adjustment tool that reaches or maintains equilibrium is total production. If total expenditures are different to total production, then total production should make changes to meet balance. On the other hand, the adjustment tool for the total market model is the price level. If total demand is different to total supply in the market, then the price level should increase or decrease to meet balance. However, price level is an external force in Keynesian model.

Thirdly, Keynesian equilibrium is only a balance between total expenditures and total production. Other aggregate markets like resource markets does not need to be in equilibrium. Shortage and surpluses can exist and always in resource markets. Therefore, full employment is not reach automatically with Keynesian equilibrium.

Three Variations

The Keynesian model has three common variations, each variations established on a different combination of the four macroeconomic sectors.

Two sector model is the simplest Keynesian model which only refer to the household and business sectors, also called as the private sector. This variation is often used to demonstrate the basic operation of the model, including changes for equilibrium and the multiplier process. Two sector model gains the role of encouraged expenditures by household consumption and the role of self-directed expenditures by business investment.

Three sector model probably is the most generally analysed variation of the Keynesian model. This variation adds the government sector into the household and business sectors. This variation is used to examine government stabilization policies, especially how fiscal policy apply in government purchases and taxes that could close the gaps of recessionary and inflationary.

Four sector model consists of all four macroeconomic sectors such as household, business, government, and foreign. Interaction between domestic economy and the foreign sector often used to capture by four sector model, and also offers basis for detailed, empirically estimated models of the macroeconomics.

The Multiplier

An important moment of analysis carry out using Keynesian model is the multiplier. Cumulatively reinforcing encouraged interaction between consumption and production that increases self-directed expenditure changes, investment, government spending, and exports is basic of Keynesian multiplier.

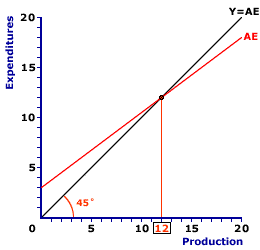

The core of the multiplier is that pretty small changes in independent expenditures cause fairly large overall changes in total production and income. The resulting changes in total production are typically a “multiple” of the first expenditure changes, hence the term “multiplier.” To understand how the multiplier procedure, reflect the Keynesian cross equilibrium presented. At total production of $12 trillion, total expenditures line (AE) intersects with the 45 degree line (Y=AE). This production level would change if the total expenditures line shifts.

The subsequent multiplier is due to marginal propensity to consume. Increases in government purchases would increases production and income, which then encourages increase in consumption based on marginal propensity to consume. Increase in consumption would cause further changes in production and income, which then brings more impacts in consumption. Thus, a larger multiplier is based on larger marginal propensity to consume.

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this essay and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal