Financial System and Formal Credit Services in Vietnam

| ✅ Paper Type: Free Essay | ✅ Subject: Economics |

| ✅ Wordcount: 2907 words | ✅ Published: 01 Feb 2018 |

An overview of the Vietnamese financial system

Over a 4-year period from 1988 to 1992, the Vietnamese government have initiated a wide ranges of economic reforms in order to enhance the transition itself from a centrally-planned to a market-oriented economy. Along with the implementation of state enterprise reforms and external trade liberalization, the Vietnamese government have promoted a huge number of banking sector reforms, which has resulted into a diversification of the financial system. First, a Soviet-style mono banking system has switched to a two-tier banking system in 1988s with the four sector-specialised state-owned banks separated from the State Bank of Vietnam (SBV) and playing a key role in the banking system. These four state-owned banks include the Bank for Foreign Trade of Vietnam (Vietcombank), the Vietnam Bank for Industry and Trade (Vietinbank), Vietnam Bank for Agriculture and Rural Development (VBARD) and the Bank for Investment and Development of Vietnam (BIDV). The SBV acts as the central bank, providing both on-site and off-site inspection and supervising the operations of both banks and non-bank financial institutions.

The public banking sector is comprised of the five state-owned commercial banks which altogether dominates the market. Second, the Vietnamese government also encouraged and created various opportunities for the influx of new players into the financial sector. These newcomers consisted of foreign banks, non-bank financial institutions such as insurance companies, join-stock commercial banks, join-venture banks, even credit funds and cooperatives. In addition, this policy has led to a dramatic rise in the quantities of branches and representative offices of existing state-owned commercial banks at that period. Bank for Foreign Trade, for example, has totalled 32 municipal and provincial branches (World Bank 2002). The branch network of the banking sector totally covers nearly 10,000 wards and communes throughout the nation.

The economic reform process has, additionally, brought about the marked transformation in agriculture production sector. The presence of private family farms and non-farm enterprises in rural sites has increased pressures on the government for the establishment of credit institutions. Vietnam Bank for Agriculture and Rural Development (VBARD) and Vietnam Bank for Social Policy (VBSP) has then become the dominant financial service providers to the low-income population, and used the extensive network of political mass organizations to mobilize, appraise, and monitor clients (BWTP 2008).

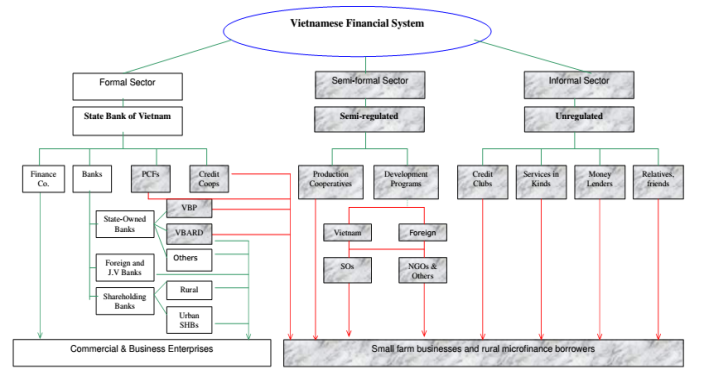

Like many other developing countries, Vietnamese credit markets is the coexistence of formal and informal credit markets. In general, rural financial system in Vietnam can be grouped into three main categories: formal sector, semi-formal sector and informal sector (Marsh et al. 2004; Lan and An 2005). The formal sector includes Vietnam Bank for Agriculture and Rural Development (VBARD), Vietnam Bank for Social Policy (VBSP) and People Credit Funds (PCFs) (World Bank, 2002). Semi-formal credit is provided by the National and International programs targeting at a selective range of borrowers and conforming to certain development targets (Pham and Lensink, 2007), and by Microfinance Programs of Mass Organizsations as well as by Savings and Credit Schemes supported by NGO and donors. The informal sector consists of private moneylenders, revolving credit associations (RCA), relatives, friends and other individuals. The informal sector has been the traditional provider of credit in rural areas, as the result of an underdeveloped formal credit market (Marsh et al. 2004).

In programs towards poor and vulnerable households, the Vietnamese Government included credit provision through microfinance institutions (MFIs) in their anti-poverty programs for the rural areas (Commins et al., 2001). These are programs focusing on female clientele who often join in groups, providing small loans for them to invest in income-generating activities (Armendariz and Morduch, 2005). The expected outcome is that rural female entrepreneurs can cope better with emergencies such as unfavorable natural events or be protected from further impoverishment during economic stress (Rutherford, 2002).

The formal sector has been the key credit provider in the Vietnamese rural credit market, in which VBARD and VBSP are both the dominant. VBARD has the largest percentage of outstanding loans in the year 2010, accounting for 63%, followed by VBSP at 30%. The third position belongs to PCFs, at 6%. In contrast, microfinance institutions occupies merely 1% of outstanding loans.

Figure: Percentage of outstanding loans of main sourcesto household borrowers

Source: (PCFs 2010; VBARD 2010; VBSP 2010; Mix Market 2012)

Source: Microfinance Resource Centre (2001)

Regulations regarding banks

With the aim of improving the provision of credit for individuals, households and firms in need and enhancing the effectiveness as well as the soundness of credit providing institutions, the Vietnamese government has promulgated a wide range of regulations on banking operations. These laws set numerous regulations for credit products offered, as well as for activities of credit institutions, ranging from capital norms, restrictions on asset/liability management and limits on credit institutions’ investment in real estate.

In 2010, the government has issued the Decree No.41/2010/ND-CP on a wide range of credit policies aimed at agricultural and rural development. First, credit institutions should, under the decree, be encouraged to provide their credit services for rural areas with appropriate interest rates, in accordance with commercial lending mechanism. Second, lending procedures should be simplified, facilitating rural borrowers to get access to loans. Moreover, assistance policies for rural borrowers should also be built up so as to curb expected risks, say, natural disasters, earthquakes or epidemics. Third, the decree will operate as a legal framework for the political system and the whole society in the enhancement of the lending provision for the agricultural and rural development.

Interest rate policy

Interest rate policy is among crucial policies for the reform of banking sector regulated by The Law on Banks and Credit Institutions. Since 2000, the government has gradually liberalised interest rates. And it is the liberalization of the interest rate that gives financial institutions a little more freedom in determining the rates on lending and saving (WB, 2002). The replacement of the base interest rate mechanism plus margins for the ceiling mechanism regarding the domestic currency-based lending has then been applied for all formal financial institutions. Both base lending rate and margin, under this mechanism, acts as limits for the lending rate requirements of the banks. This new mechanism provides adequate flexibility to credit institutions and should help to enhance firms’ access to credit (IMF, 2002a). Furthermore, the Vietnamese government has also undertaken the regulation for the difference between lending rates and saving rates. According to this regulation, this spread cannot exceed 0.3% and 0.5% per month for short-term loans and medium-term and long-term loans respectively, which has in turn discouraged rural financial institutions from extending small loans to the rural poor and low-income households, given the high transaction costs for small loans (Dao, 2002).

Lending technology

In Vietnam, there are two prevailing lending methods namely individual lending and group lending. As shown in the table below, group lending has become more popular than individual lending, with the proportions for the year 1995, 1998 and 2001 standing at 98.1%, 92.1% and 87.6% respectively. Meanwhile, the percentages for individual lending method was much lower between 1995 and 2001. While individual lending technology typically focuses on the role of monitoring each individual borrower, the mechanism for group lending technology relies on the enforcement of joint liability of joining members. Generally, lending technologies can be distinguished based on different dimensions such as the primary source of information, screening and underwriting policies/procedures, structure of the loan contracts, and monitoring strategies and mechanisms (Berger and Udell 2006, hereafter BU06).

Source: McCarty (2001)

Collateral

Under Decree No.41/2010/ND-CP, the mechanism of collateral for loans has been regulated as follows: First, credit institutions may take the provision of loans to customers with or without security assets into consideration under current regulations. Second, collateral-without lending conditions, procedures, and loan amounts must be in compliance with current provisions of law on credit institutions’ provision of loans to borrowers. For individuals and households engaged in agriculture, forestry, fishery or salt production, the amount of loan can total up to 50 million VND, whereas the figure for households operating business or production activities or providing services for agriculture and rural areas is up to 200 million VND. And up to 500 million VND for cooperatives and farm owners. Third, credit institutions consider providing trust-reliant loans for individuals and households on the basis of guarantee by sociopolitical organizations in rural areas under current regulations. Sociopolitical organizations have responsibility of coordinating and performing all or some of the credit operation stages after reaching agreement with the lending credit institutions.

In reality, collateral is regarded as one of mandatory requirements for loans by formal credit institutions. Credit institutions often ask for collateral from borrowers in order to ensure the probability of loan repayment, as well as reduce the asymmetric information between borrower and formal lender. The asymmetric information occurs since most of the banks stay far away from potential rural borrowers, and they find it difficult to acquire previous credit history information as well as current production/business information about those borrowers. In such a case, collateral requirements are given so as to mitigate these problems. Collateral is usually in the form of immovable assets such as land use certificates, buildings, fixed assets, bank accounts, and other valuable assets, in which land use certificates and real estate are the most preferred collateral by banks. In rural areas, there has been a small number of households that have met the collateral requirements imposed by formal financial institutions, whereas a markedly bigger number of rural borrowers have faced the lack of of collateral for their loans. This has, in turn, confined rural borrowers from having access to loans from formal credit institutions. In such cases, these rural borrowers have to search for other credit providers that do not require collateral, say, private moneylenders, friends, or neighbours which all belong to the informal sector.

Therefore, giving households the possibility to obtain land-use rights and use them as proof of collateral can give rise to the asymmetric information alleviation between borrower and formal credit lender, thus fostering credit transactions in rural credit markets accordingly.

The formal sector

Vietnam Bank for Agriculture and Rural Development (VBARD)

Established in 1998 along with the the intense reform of the financial system and the reintroduction of commercial banks in Vietnam, the Vietnam Bank for Agriculture and Rural Development (VBARD) has been regarded as a state policy bank and received subsidy from the Vietnamese government. VBARD has also been known as a legal entity with the sharp focus on the agriculture sector and rural areas. By the end of 2001, VBARD has become among leading commercial banks in Vietnam, having the most extensive branch network in Vietnamese rural areas. The bank then had an operating network of more than 2,300 branches and transaction offices nationwide at the end of 2010.

There are the three following credit methodologies that VBARD has utilized for its lending operations. The first methodology is the the provision of individual loans for rural borrowers and enterprises. The mandatory requirement for this loan type is a proof of collateral, in which a land use certificate – the so called “Red Book” for agricultural land or “Green Book” for forest land – is the most widely used. Second, VBARD has also applied group lending mechanism in order to increase its coverage of rural households, as well as to reduce transaction costs associated with small loan collection. According to this method, each member of lending group bears equally the joint responsibility of loan repayment before a new round of loans is initiated. The eventual methodology involves the existence of guarantee groups formed by members of mass organizations, say, Vietnamese Women’s Union, Farmer’s Union or Youth’s Union in lending process. These mass organizations play an important role in guaranteeing the loan repayment, and loans offered by VBARD are then channed through these groups to the target borrowers who are mainly unable to provide a proof of collateral.

VBARD specializes in lending to rural households and small-scale enterprises involved in agriculture or off-farm enterprises, but the bank has recently expanded its urban branch network to capture the market of urban small enterprises (BWTP 2008).

The outstanding loans granted by VBARD to the economy totalled up to 414,755 billion VND in the year 2010. While the percentage of loans for households accounted for 51%, the figure for non state-owned company was 43%. The proportions of loans supplied to state-owned company and to small cooperative enterprises were considerably lower, at 5% and 1% respectively.

Figure. Outstanding loans of VBARD by sector

Source: VBARD (2010)

The flow chart 1 indicates the credit procedures adopted by VBARD. It is clear that there are thirteen distinct stages in the process of loan provision, beginning with the collection of loan application forms by bank officials and ending with the delivery of appropriate loans to the borrower.

Chart 1: Lending procedures by VBARD in Vietnam

Notes:

1. Bank officials receive loan application forms from the applicant;

2. After receiving loan application forms, bank officials report to the head of the credit department;

3. The head of the credit department assigns a bank official to examine the loan application forms to see if it is filled in properly;

4. The assigned bank official appraises the applicant, mainly based on collateral;

5. The assigned bank official informs the head of the credit department about the applicant;

6. The head of the credit department assesses the information and reports it to the director of the bank;

7. Director of the bank decides on the loan and informs the head of the credit department;

8. The head of credit department informs the assigned bank official about the decision;

9. The assigned bank officer informs the applicant;

10, 11, 12. Internal information among the bank’s specialized departments;

13. The treasury department disburses loans to the applicant, if accepted.

Source: Adapted from Ninh (2003)

Vietnam Bank for Social Policy (VBSP)

The Vietnam Bank for Social Policies was established under Premier’s Decision No. 131/2002 QD-TTg dated October 4th, 2002 and the Government’s Decree No. 78/ND-CP dated October 4th, 2002 on the provision of credit for the poor and other policy beneficiaries. VBSP was set up on the basis of the reorganization of the Bank for the Poor and separated from VBARD with the aim of detaching the lending policy mechanism from the commercial lending mechanism. Since then, VBSP has developed its own network of 610 branches in 63 provinces/cities throughout the country and has extended loans to 46% of the poor in rural and mountainous areas (GSO Report on the results of VHLSS 2006).

VBSP’s operations are under the supervision of the State Bank of Vietnam, whose the primary objective is to provide non-collateralized preferential loans of different rates and maturities to poor individuals, households, and organizations eligible for social benefits and policies. VBSP is conducting the method of entrusted lending via the four mass organizations, namely Women Union of Vietnam, Farmer Union of Vietnam, War Veteran Union of Vietnam and Youth Union of Vietnam. These four organizations take charge of some lending steps of VBSP such as establishing savings and credit groups; organizing certifying poor households, supervising borrowers in using loans properly etc, whereas VBSP has responsibility for conducting loan disbursement, loan collection and safe treasury management.

The credit programs provided by VBSP has become increasingly diversified and appropriate with different borrowers. First, for the purpose of the implementation of the National Target Program on Hunger Eradication and Poverty Elimination initiated in 1988s, VBSP has established credit programs particularly targeting at poor households living in rural areas. The second customer group of VBSP is university/college students whose families are ranked as poor households at the commune level or village level. The objective of this lending is to support financially for those students in order that they have opportunities to fulfill their study. The third credit program of VBSP is for households living in disadvantaged and remote areas where there is very poor infrastructure or challenging climate conditions. The fourth credit program involves an implementation of the national strategy on clean water supply and environmental sanitation in rural areas for living conditions improvement, and the target customers are still poor households in rural places. Fifth, VBSP also builds up credit programs for job creation aimed at poor households and small business enterprises. Apart from credit programs listed above, there are still other various programs supporting for poor households in rural areas.

The table below gives a comparison in terms of the percentages of outstanding loans allocated by VBSP for numerous credit programs between 2004 and 2010. It is evident that credit programs for production and business of poor households made up the largest percentage in both years, with 82% in 2004 and 40% in 2010. The second largest in 2010, which occupied 29% of the total outstanding loans, was credit programs for education. In contrast, that for migrant workers to go abroad accounted for only 1%.

Table: The proportions of outstanding loans by credit programs.

Source: (VBSP 2004; VBSP 2010)

In regard to the loan interest rate, in 2013, the annual lending interest rate of the market was 10.8%, while the figure for VBSP was merely 6.0%. That means VBSP subsidized 4.8% of the lending interest rate for the poor (World Bank 2004). Since the decision No. 579/QÄ-TTg dated May 6, 2009 on the support of the lending interest rate for VBSP’s loans was issued, the annual interest rate on loans for agricultural production and off-farm jobs reduced by 5%, from 7.8% to 3.8%, while that of the market was standing at 10.5% on average. By late 2010, VBSP’s total outstanding loans mounted to 89,461 billion VND, 14 times higher compared to that in 2001.

People’s Credit Funds (PCFs)

People’s Credit Funds were established in 1993 after the collapse of rural credit cooperatives. According to Hung (1998), PCFs were constructed on the model of the Caisse Populaire system in Quebec, Canada, with the technical support from the Development International Desjardins (DID). PCFs were funded by the Canadian International Development Agency (CIDA) and supervised by the State Bank of Vietnam.

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this essay and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal