Effects of Changing Levels of Market Concentration on the Australian Economy

| ✅ Paper Type: Free Essay | ✅ Subject: Economics |

| ✅ Wordcount: 2624 words | ✅ Published: 03 Nov 2020 |

Executive Summary

In the last decades, the growing trend of rising market concentration around the globe has created key concern as many industries become less competitive and more concentrated. Similar observations have been noted in the Australian economy where big firms are usually dominating the market. This paper examines the increasing market concentration in the Australian economy by taking into account the things that influence its existing competition, naming industries that have become more concentrated, and the effects of such economic trends. Two major factors found to make the Australian markets weak are economies of scale and heavy regulation. Not so many industries have contributed to the growing market concentration and Manufacturing takes the first spot. Lastly, as detailed in the last part of the paper, there are three primary areas impacted by the rising market concentration in Australia. These include productivity, profitability, and wage growth.

Introduction

Through the use of Herfindahl–Hirschman Index, the Australian economy can still be considered as competitive. It scored with lower than 0.23 for over 90% of the industry and smaller than 0.04 for over half of the industry (Bakhtiari, 2019). It was claimed that a significant change in market concentration that can harm competition and restricts firm entry spurs concern for job creation and future growth of the economy. The focus of this report is to show the effects of increasing levels of market concentration on the Australian economy by looking at highly concentrated industries.

In the modern economy, high competition or competitive pressure is equated to good economic performance. It prompts firms to be innovative and utilise resources to their best use. However, in the past years, Australia and other countries around the globe have been worrying that competition is not as healthy as it should be. More specifically, big concerns were expressed over findings showing that industrialised nations have been controlled in the hands of fewer firms. The concept of market concentration is very essential as it is taken as a proxy measure of the intensity of competition in an economy. In Australia, has competition weakened? If so, how? Which industries have turned more concentrated? The report will address these questions.

Analysis of Market Concentration in the Australian Economy

Many studies reveal that the increasing trend in market concentration is responsible for explaining the decreasing labour share of production. This was documented in the economies of the U.S., North America, and Europe, as well as across the OECD nations (Autor et al, 2017; Guschanski & Onaran, 2018; & Bajgar et al., 2019). It is, therefore, in the interest of this paper to analyse the case of Australia.

Factors Shaping Competition in the Australian Economy

There are a number of factors that shape competition in the market, also referred to as ‘barriers to entry’. The most significant factor that shapes the Australian economy is economies of scale wherein larger firms incurred lower costs than smaller ones. This is very prevalent in sectors that are often served by a few firms while remote and relatively small economies in Australia have lower productivity as they are not equipped to exploit economies of scale (Minifie, 2017). If there are very high or powerful economies of scale, the market is characterized by a natural monopoly, which, in turn, adversely affects competition (Gittins, 2018).

Another key factor impacting competition, in many ways, is heavy regulation. First, it can potentially increase the costs of business operations in particular sectors, most especially the smaller ones. Additionally, it can also restrict the number of firms and explicitly limit competition between firms by strictly controlling where competitors can open their businesses (Azar et al., 2017). In market sectors where these barriers to entry are present, there may be weaker competition. In the Australian economy, market sectors identified with those barriers relatively have a comparably little share of the entire gross value added (15%) according to the National Accounts reported by the ABS (2017).

Figure 1. Majority has lower entry barriers, Figure 2. Concentration is more in sectors with barriers to entry.

is trade-exposed, or is mostly publicly provided.

Source: ABS (2017). Source: Grattan Analysis of IBISWorld (2017).

As illustrated in Figure 1 above, most of the sectors identified with barriers to entry are considered to be highly concentrated. In fact, on average, the biggest four firms under those marked sectors provide more than half the market share, supplying around 70% of firms with strong economies of scale, over 60% of those with heavy regulation. Whereas market players in the sector of natural monopoly provide 100% of their local markets. However, it can also mean that not a single firm holds the monopoly but various firms do in different locations. On the contrary, the same firms supply lower than 20% of the market in the bigger low barriers sectors.

Measuring Market Concentration Through HHI

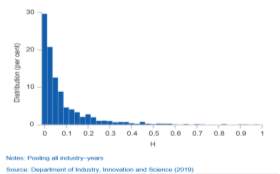

While there are many ways to measure market concentration, most of them present errors and problems but one tool remains to be widely accepted in academia – the Herfindahl–Hirschman Index or HHI. This measure calculates the square of the market share of every firm competing and sums up the resulting figures, giving a score that ranges from almost zero to 10,000 (DAF, 2018). One of its greatest advantages is that it considers the relative size distribution of the firms existing in the market. Essentially, it rises as the number of firms competing in the market goes down as well as the variation in firm size goes up. In this case, the study of Bakhtiari (2019) revealed that very few industries in Australia are dominated by a small number of big firms as shown by the skewness in the graph of the distribution of HHI on Figure 3. Moreover, the HHI (less than 0.23 for over 90% of the industry and smaller than 0.04 for over half of the industry) statistics also further confirmed that Australian industries are not that concentrated.

Figure 3. The distribution of HHI.

Australian Industries That Have Become More Concentrated

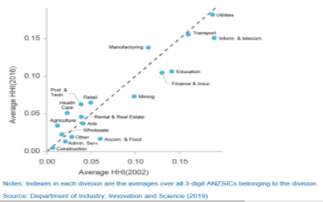

It is imperative to emphasise that on average, market concentration in Australia prior to 2007 has been going lower but from that year onwards until 2016, HHI results have shown an increasing trend (Bakhtiari, 2019). Interestingly, industries with HHI lower than the median demonstrated no noticeable changes in market concentration but for those with HHI higher than the median, nearly all the rise in concentration occurred among them. The following graph (Figure 4) illustrates the changes in market concentration levels in various industries according to Australian and New Zealand Standard Industrial Classification or ANZSIC divisions.

Figure 4. The shift in HHI from 2012-2016 by ANZSIC divisions.

Industries above the 45-degree line have increased in their concentration, with the manufacturing industry as the leading one while those below have dropped from 2002 until 2016 (Department of Industry, Innovation and Science, 2019). Other concentrated industries include Healthcare, Professional, Scientific & Technical, Retail, and Agriculture. Market concentration in most other industries that experience very little change in HHI does not incur significant change from 2002 to 2016. They are from the Construction ANZSIC division.

While it is established that barriers to entry play the biggest role in making certain industries highly concentrated, it is crucial to consider that the rising market concentration is not directly related to a diminishing demand (Kollmorgen, 2016). In fact, the majority of the increase in market concentration among the concentrated sectors occurs where there is an expansion in the demand side of the market (Department of Industry. Innovation and Science, 2019). This suggests that a big chunk of the increase in demand has been absorbed by some firms. Thus, it is imperative to determine what particular industry characteristics have been contributing to increasing concentration.

Bakhtiari (2019) attempted to consider digital maturity as one possible contributing factor as innovation on digital technologies is a key driver of growth and productivity. However, his findings revealed that digital maturity is not likely to be causing the observed rising pattern in market concentration. Another factor looked into is productivity distribution. Theoretically, when resources in the industry reallocate into the most productive units, the dominance of such units is expected to grow, resulting in higher market concentration (ACCC, 2013). In effect, higher productivity dispersion provides more space for better reallocating resources. An alternative interpretation would be a larger productivity skewness in indicates the existence of firms that have the advantage to control the industry. However, the same conclusion was reached that both the productivity dispersion and productivity skewness do not contribute to the increasing average HHI (Bakhtiari, 2019).

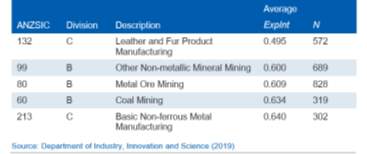

One last factor considered is export orientation. Several researchers argued that export-oriented industries have higher market power because they are in an advantaged position to undercut the prices of their rivals while still able to get high markups exporting firms (De Loecker & Warzynski, 2012; Zingales, 2017). As such, these exporting industries can curb competition and are capable of controlling the market. According to the same data from the DIIS (2019), as reflected in Table 1 below, the most export intensive firms are those from the Manufacturing and Mining industries. On average, the manufacturing and mining industries export no less than 50% and 60% of their outputs, respectively. The analysis of the connection between export intensity and HHI exhibits a positive result, suggesting that market concentration is increasing where an industry is export-oriented and highly concentrated (Bakhtiari, 2019).

Table 1. Most export intensive industries

In sum, market concentration in Australia started to increase post-2007 and it happens in industries that are already concentrated or those with HHI higher than the median. However, only a few industries, with Manufacturing on the lead, that have an increasing trend of market concentration while others have decreased. Among three possible contributing factors evaluated, the export intensity has a substantial correlation with increasing average HHI in concentrated industries like manufacturing and mining.

The Impact of Increasing Market Concentration on 3 Key Economic Areas

Now, how does this rising trend in market concentration has impacted the Australian economy? This report identifies and discusses three key areas where the effects of this changing level of concentration have the most impact. These include productivity, profitability, and wage growth.

#1. Effects on productivity. As shown in the tested analysis of Bakhtiari (2019) on the effects of rising market concentration on the productivity of firms, the two variables change in opposite directions. This means at times when market concentration grows, the average productivity of firms goes down. Conversely, in cases where market concentration is decreasing, productivity increases. This verifies the assumption of most studies that increase in market concentration harms competition. However, it is a noteworthy finding that when great performance or innovation and export intensity go hand-in-hand in highly concentrated industries, such as manufacturing, the average productivity of firms rises. Finally, as found by Campbell et al. (2019) in their working paper with ABS and the Treasury, there has been a significant decline in labour productivity dispersion among the six Australian industries from 2001 to 2014. These include the Manufacturing which has been found out earlier to be the top industry that gained the highest increase in market concentration.

#2. Effects on profitability. With their market power, some big firms in Australia are deemed to make high profits and these earnings are even higher behind barriers to entry. As presented in the report of Minifie from Grattan Institute (2017), firms in high-barrier sectors all enjoy above-average returns whereas those competing in low-barrier sectors get below-average returns. The report indicated that average profitability is about 20% higher in the sectors with barriers to entry. Moreover, highly concentrated industries are more profitable on average and markets expect profits in these sectors to remain higher than those elsewhere (Bakhtiari, 2019). Despite this higher profitability of firms in high-barrier sectors and highly-concentrated industries, the presence of concentration explains lower than 10% of the disparity in returns across industrial sectors (Minifie, 2017). This only means that firms competing in a concentrated industry that has weak competition is not a guarantee of great profitability. However, the fact still stands that more than $10 billion of super-normal profit (above average) is earned in monopoly and other regulated industries. This only implies that regulators have not done everything to make sure that consumers’ welfare is not highly considered in these industries.

Figure 5. Wage growth

#3. Effects on wage growth. While corporate profits in Australia have been increasing

in the last ten years, the opposite is happening with wage growth that has been stagnant and remains low as seen in Figure 5. This same pattern is also observed not just in Australia but in other advanced or high-income economies like the U.S. (Ayala, 2018). One significant finding corroborates with the results reported by the Grattan Institute discussed above, that is highly-concentrated industries do earn higher returns compared to non-concentrated ones (Azar et al., 2017). As large firms have the power to affect prices in markets, they can also do so in the case of wages in the labour market. More specifically, a study by Benmelech et al. (2018) that uses HHI showed that firms with monopsony power are able to lower wages by up to 3% yearly. Thinking about its long-term effects, it can be a huge reduction in the future if the same trend in wage growth in Australia is observed.

Conclusion

The increasing trend of market concentration has caused major concern across countries. The same pattern is being observed in the Australian economy in which the top four large industries are dominating the market while earning too much bigger than other industries. This paper analysed the issues associated with the rising market concentration in Australia through the lens of the Herfindahl–Hirschman Index. It further identified the factors that shape the competition in the Australian market, particularly economies of scale and heavy regulation. The findings show that only a few industries have seen an increase in their concentration with Manufacturing at the top list. It was also discovered that export intensive industries are more likely to contribute to such an increase. Lastly, the report discussed the biggest impact of the increasing market concentration on three economic aspects of firms among the different Australian industries. These include firm productivity, profitability, and wage growth.

Reference List

- Autor, D., et al., 2017. Concentrating on the fall of the labor share, NBER Working Paper No. 23108. American Economic Review, 107(5), 180–185. DOI: 10.3386/w23108.

- Australian Bureau of Statistics, 2017. Australian System of National Accounts, 2016-17. cat. no. 5204.0. http://www.abs.gov.au/ausstats/abs@.nsf/mf/5204.0.

- Australian Competition & Consumer Commission, 2013. Thoughts on market concentration issues. Retrieved from https://www.accc.gov.au/speech/thoughts-on-market-concentration-issues.

- Ayala, M., 2018. Is market concentration undermining wage growth? Essa. retrieved from http://economicstudents.com/2018/05/market-concentration-undermining-wage-growth/.

- Azar, J., Marinescu, I. & Steinbaum, M. I., 2017. Labor market concentration. NBER Working Paper No. 24147. DOI: 10.3386/w24147.

- Bajgar, M, et al., 2019. Industry concentration in Europe and North America, OECD, Productivity Working Paper, No.18. https://doi.org/10.1787/24139424.

- Bakhtiari, S., 2019. Trends in market concentration of Australian industries. Department of Industry, Science, Energy, and Resources, Office of the Chief Economist. Retrieved from https://www.industry.gov.au/data-and-publications/trends-in-the-market-concentration-of-australian-industries.

- Benmelech, E., Bergman, N., & Kim, H., 2018. Strong employers and weak employees: How does employer concentration affect wages? NBER Working Paper No. 24307. DOI: 10.3386/w24307.

- De Loecker, J. & Warzynski, F., 2012. Markups and firm-level export status, American Economic Review, 102(6), 2437–2471. DOI: 10.1257/aer.102.6.2437.

- Directorate For Financial And Enterprise Affairs Competition Committee, 2018. Market concentration. OECD Secretariat. Retrieved from https://one.oecd.org/document/DAF/COMP/WD(2018)46/en/pdf.

- Gittins, R., 2018. Weak competition may be key to economy’s problems. The Sydney Morning Herald. Retrieved from https://www.smh.com.au/business/the-economy/weak-competition-may-be-key-to-economy-s-problems-20181102-p50dkr.html.

- Guschanski, A. & Onaran, O., 2018. The labour share and financialisation: Evidence from publicly listed firms, Greenwich Papers in Political Economy 19371, University of Greenwich, Paper No. GPERC59, Greenwich Political Economy Research Centre.

- Kollmorgen, A., 2016. Market monopolies in Australia: Is Australian suffering from a market concentration crisis? CHOICE. Retrieved from https://www.choice.com.au/shopping/everyday-shopping/supermarkets/articles/market-concentration.

- Minifie, J., 2017. Competition in Australia Too little of a good thing? Grattan Institute, Report No. 2017-12. Retrieved from https://grattan.edu.au/wp-content/uploads/2017/12/895-Competition-in-Australia-Too-little-of-a-good-thing-.pdf.

- Zingales L (2017) Towards a Political Theory of the Firm, Journal of Economic Perspectives, 31(3), 113–130.

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this essay and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal