Capital Structure Effect on Performance in Renewable Energy

| ✅ Paper Type: Free Essay | ✅ Subject: Economics |

| ✅ Wordcount: 1513 words | ✅ Published: 19 Mar 2018 |

Sarah Sophia Hamdi

“Capital Structure Effects on Firm Performance in the Renewable Energy Sector: Evidence from Germany”

1. Explanation of your dissertation topic (about 800 words)

Overall motivation and objectives:

The Kyoto Protocol induced a growing number of countries to establish targets for renewable energy supplies to reduce greenhouse gas emissions as well as to increase energy security. These targets are either expressed in terms of installed capacity or as a percentage of energy consumption. These targets have served as important catalysts for increasing the share of renewable energy throughout the world.

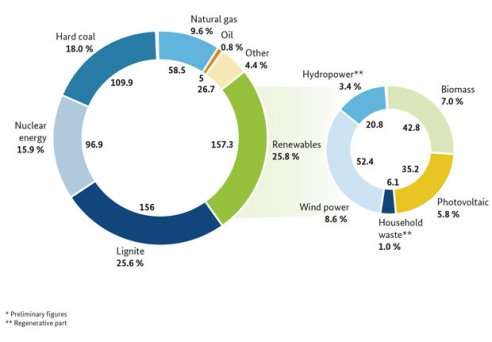

As a result of the growing share of energy generated from renewable sources such as wind, water and biomass Germany’s energy supply is becoming “greener” from year to year. As shown in graph 1 in 2014 renewables already accounted for 25.8 per cent of the gross power production in Germany. On 1 April 2000 the Renewable Energy Sources Act (EEG) went into force and lead to a massive increase of the renewable energy production in the electricity sector, from under 40 to over 140 billion of kilowatt per hours (see graph 2).

Graph 1: Gross power production in Germany in 2014

Source: AG Energiebilanzen, as of: December 2014

Graph 2: Gross electricity generation in billions of kilowatt-hours

Source: BMWi based on Working Group on Renewable Energies – Statistics (AGEE-Stat, August 2014; Preliminary figures)

The German government wants to further expand this share by the year 2025, the aim is to produce 40 to 45 per cent of electricity from renewable sources and 55 to 60 per cent by the year 2035. These numbers indicate that renewable energy companies increasingly need to compete efficiently against existing companies generating energy through other power sources such as oil, nuclear and hard coal energy etc.

As investments in renewable energy plants grow, so do the risks inherent in owning, building and operating such plants. Excluding debt, business risk is the basic risk of firms operations and one of the factors that influence a company’s capital-structure decision making. The level of business risk is shaped not only by the companies’ decisions but by what’s happening to the industry and the economy. The renewable energy industry is effected by numerous sector specific risks such as building and testing risk, business, environmental, financial, market, operational, political/regulatory and weather related volume risk. In such a risky industry, what otherwise would be an appropriate and safe amount of debt becomes more dangerous and unstable, so that normally equity financing is safer than through debt. However firms that are in the growth stage of their cycle typically finance that process through debt and borrow money to enable their growth. The conflict that arises with this method is that the revenues of growth firms are typically unstable and unproven. Meaning that a high debt load is usually not appropriate due to the danger of financial embarrassments. Hence as companies expand their investments in renewable energy projects, funding is a particular challenge and questions about firms’ capital structure decisions are not easily answered.

Theoretical background:

Over the last few decades much research has been done on whether a relationship between capital structure and a firms’ financial performance exists. At this point I would like to include a detailed literature review.

Franco Modigliani and Merton Miller formed with their theorem the foundation for modern thinking on capital structure. They developed the Capital Structure Irrelevance Proposition where they hypothesized that in perfect markets the capital structure of a firm does not influence its performance. Nevertheless the theorem is generally viewed as a highly theoretical hypothesis, since it disregards important factors such as transaction costs and uncertainty, it was often used as the basis for further research in the last decades. The pecking-order theory, the agency theory and the trade-off theory are the three main theories discussing the optimal capital structure of a firm. All of them follow different approaches which I will summarise and contrast with each other.

The different theories and findings raise key questions such as whether it is possible to identify an optimal capital structure for firms operating in the important and future-oriented industry of renewable energies.

Research analysis and methodology:

Following to the introduction of the key theories and the literature review on this topic I would like to carry out my own quantitative study and run a regression analysis with financial data of 20 companies operating in the renewable energy sector, including wind, solar, bio and water energy in Germany. Due to the fact that non-listed firms are not required to disclose their financial accounts my data will be gained from listed companies that are obligated to share the relevant information. I would like to examine whether there exists a relationship between the implemented capital structure and the firms performance measured in return on equity and share price.

Equations:

(1)

(1)

(2)

(2)

Where:  return on equity for firm i in year t.

return on equity for firm i in year t.  : price of a share for firm i at year t.

: price of a share for firm i at year t.  : financial leverage for firm i at year t .

: financial leverage for firm i at year t . : tangible assets for firm i at year t.

: tangible assets for firm i at year t.  : size of the firm i at year t.

: size of the firm i at year t.  : growth of the firm i at year t.

: growth of the firm i at year t.

Tangible assets, size and growth serve as control variables whereas financial leverage of the firm is considered as the main variable to express the capital structure.

My aim is to be able to match one of the three theories and to identify an optimal capital structure for renewable energy firms. In order to interpret the findings of the quantitative analysis I would also like to include a complementary qualitative research analysis for example through directors’ statements on their financing decisions.

2. List of References (no minimum number required, but as acceptable by your supervisor)

Agnihotri, A. (2014): Impact of Strategy – Capital Structure on Firms’ overall Financial Performance, Strategic Change, Vol. 23, No. 1-2, pp. 15-20.

Ben Ayed, W. H., and Zouari, S. G. (2014): Capital Structure and Financing of SMEs: The Tunisian Case. International Journal of Economics and Finance, Vol. 6, No. 5, pp. 96-111.

Bouraoui, T., and Li, T. (2014): The Impact of Adjustment in Capital Structure in Mergers & Acquisitions on us Acquirers’ Business Performance. The Journal of Applied Business Research, Vol. 30, No. 1, pp. 27-41.

Economist Intelligence Unit (2011): Managing the risk in renewable energy. A report from the Economist Intelligence Unit Sponsored by Swiss Re. file:///C:/Users/Sarah/Downloads/Managing-The-Risk-In-Renewable-Energy.pdf

Gill, A. and Biger, N. and Mathur, N. (2011): The Effect of Capital Structure on Profitability: Evidence from the United States. International Journal of Management, Vol. 28, No.4, pp. 3-.

Green, J. (2010): Renewable energy projects: Risk and insurance elements. Technical feature – Construction & Engineering, www.meinsurancereview.com, pp. 41-42.

Hatfield, G. B. and Louis, T. W. and Davidson, W. N. (1994): The determination of optimal capital structure: The effect of firm and industry debt ratios on market value. Journal of Financial and Strategic Decisions, Vol. 7, No. 3, pp. 1-14.

Holz, C. A. (2002): The Impact of the Liability-Asset Ratio on Profitability in China’s Industrial State-Owned Enterprises. China Economic Review, Vol. 13, pp. 1-26.

Majumdar, S. K. and Chhibber, P. (1999): Capital Structure and Performance: Evidence from a Transition Economy on an Aspect of Corporate Governance. Public Choice, Vol. 98, pp. 287-305.

Margaritis, D., and Psillaki, M. (2007): Capital structure and firm efficiency, Journal of Business Finance and Accounting, Vol. 34, No. 9, pp. 1447-1469.

Modigliani, F. and Miller, M. (1958): The Cost of Capital, Corporation Finance and The Theory of Investment, The American Economic Review, Vol. 48, No. 3, pp. 261-97.

Modigliani, F. and Miller, M. (1963): Corporate Income Taxes and the Cost of Capital: a Correction. The American Economic Review, Vol. 53, pp. 443-53.

Myers, S. (1984): Capital structure puzzle, The Journal of Finance, Vol. 39, Issue 3, pp. 574–592.

Omondi, M. M., and Muturi, W. (2013): Factors Affecting the Financial Performance of Listed Companies at the Nairobi Securities Exchange in Kenya. Research Journal of Finance and Accounting, Vol. 4, No. 15, pp. 99-105.

Onaolapo, A. and Kajola,O. (2010): Capital Structure and Firm Performance: Evidence from Nigeria. European Journal of Economics, Finance and Administrative Sciences, Vol. 25, pp. 70-82.

Pathirawasam, C. (2013): Internal Factors which Determine Financial Performance of firms: With Special Reference to Ownership Concentration. pp. 62-72.

Rajan, R. G., and Zingales, L. (1995): What Do We Know about Capital Structure? Some Evidence from International Data. The Journal of Finance, Vol. 50, No. 5, pp. 1421–1460.

Shyam-Sunder, L. and Myers, C. (1999): Testing static trade off against pecking order models of capital structure. Journal of Financial Economics, Vol. 51, No. 2, pp. 219–244.

Soumadi, M. and Hayajneh, O. (2012): Capital structure and corporate performance, Empirical study on the public Jordanian shareholding firms listed in the Amman stock market. European Scientific Journal, Vol. 8, No. 22, pp. 173-189.

Stiglitz, J. E. (1969): A Re-Examination of the Modigliani-Miller Theorem. American Economic Review, Vol. 59, No. 5, pp. 784-794.

Tailab, M. M. K. (2014): The Effect of Capital Structure on Profitability of Energy American Firms. Journal of Business and Management Invention, Vol. 3, No. 12, pp. 54-61.

Titman, S. (1988): The Determinants of Capital Structure Choice. The Journal of Finance, Vol. 43, No. 1, pp. 1-19.

Umer, U. M. (2014): Determinants of Capital Structure: Empirical Evidence from Large Taxpayer Share Companies in Ethiopia. International Journal of Economics and Finance, Vol. 6, No. 1, pp. 53-65.

Wippern, R. (1966): Financial Structure and the Value of the Firm. The Journal of Finance, Vol. 21; No. 4, pp. 615-633.

Links:

Bundesministerium für Wirtschaft und Energie (BMWi): http://www.bmwi.de/EN/Topics/Energy/Renewable-Energy/renewable-energy-at-a-glance.html

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this essay and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal