Petrozuata Case Study

| ✅ Paper Type: Free Essay | ✅ Subject: Finance |

| ✅ Wordcount: 1495 words | ✅ Published: 29 Nov 2017 |

Petrolera Zuata, Petrozuata C.A.

- Voilis Athanasios

1) Introduction – Case Study

In 1976, after nationalization of the domestic oil industry a stated owned enterprise Petroleos de Venezuela S.A. (PDVSA) was established for the purposes of managing the country’s hydrocarbon resources and promoting economic development. It was the world’s second largest oil and gas company with reserves in Venezuela and refineries across the Europe, United States, and the Caribbean. Domestically, PDVSA provided 78% of Venezuela’s export revenues, 59% of the government’s fiscal revenues, and 26% of nation’s GDP and had a reputation of being one of the best managed national oil companies.

In 1990, PDVSA started an ambitious long-term project, which main aim was to double its domestic production and expand international markets. For the implementation of this venture, the company needed to raise investments for approximate amount of USD$ 65 bn. At that time neither PDVSA nor Venezuelan government had the possibility to finance the underlined expansion. As a solution, it was decided to establish a strategy called “La Apertura”, which opened the Venezuelan oil sector to foreign companies through profit sharing agreements, operating service agreements, and strategic joint ventures associations.

Unfortunately, such initiative overlapped with political instability and economic turmoil in the country. Only in the early 1990s two failed military coups and the impeachment of President Perez took place. In late 1993, because of the severe crisis in the banking system, the administration suspended a number of constitutional rights, imposed price control on basic goods and services, and took direct control over most of the banking system. Moreover, the foreign exchange markets were closed and began rationing foreign currency to the private sector. Few years later, by the time of the deal closing, due to an economic and social reform program of President Caldera, the economy had begun to recover, but with coming presidential elections, public tension was also growing. All in all, the feasibility of the project was under the pressure of the sovereign risk. The rating agencies were considering three principal risks: possible government action, currency market volatility, and Venezuelan business conditions.

The first development project of reopening Venezuelan oil sector to foreign investments was Petrozuata. It is a USD$ 2.424 bn joint venture between Conoco and Maraven as a part of PDVSA. Conoco was the petroleum subsidiary of one of the largest chemical producer in the world E.I. du Pont de Nemours and Company (DuPont). That time Conoco recently completed projects in Russia, Norway, USA and was a recognized leader in refining technology and project development.

Underlined parties started feasibility studies and negotiations for a joint project in 1992. After four years of planning, Conoco and Maraven had made a mutual decision to finance this deal on a project finance basis, because of financial and organizational benefits provided by such structure. PDSVA could not have built the project alone because of its lack of specialized assets needed to extract and upgrade syncrude oil. On the other hand, foreign ownership of domestic hydrocarbon resources is prohibited by law, closing all ways for a sole expansion by Conoco.

In terms of ownership structure, it was strategically decided that PDVSA subsidiary contributed less than 50% of the total equity amount but, through its preferred shares, would retain voting control. Because PDVSA would be the minority shareholder, the company would be classified as private. As a consequence, it would not consolidate into PDVSA’s balance sheet and, more importantly, they would not be bound by legislation for public companies (public procurement bidding procedure, excessive accountability, etc.). Final association agreement had a term of 35 years beginning once production started in 2001. The equity ownership contributions were set up in such way that Maraven had 49.9% of shares and 50.1% for Conoco. After accomplishing of the agreement, Conoco has an obligation to transfer its shares to Maraven at no cost.

Also, to give incentive to the project, the government agreed to decrease the royalty rate during early operation years and the Congress agreed to lower the income tax rate from 67,7% to 34%.

The sponsors agreed to use USD$ 975 mn of equity and USD$ 1.45 bn of debt to finance the project, which corresponded to 60% of debt-to-equity ratio. Such high percent of equity contributions to the project were chosen to show the sponsor’s commitment to the project. In 1996, for the beginning of the project, sponsors contributed USD$ 79 mn of paid-in capital.

Additional contributions including contingency fund were projected to infuse in the following 4 years for the total amount of USD$ 366 mn. For the outstanding sum of USD$ 530 mn, shareholders chose a risky plan to use cash flows from the sale of early production crude, after completion of the oil fields and pipeline in August 1998. It is necessary to mention that risks peculiar to underlined financial mechanism were mitigated through a good execution plan and strong sponsor guarantees.

Concerning the sources of debt financing, Petrozuata raised USD$ 450 mn as a loan from commercial banks with loan guarantees from bilateral and multilateral agencies, such as U.S. ExIm Bank, Export Development Corporation of Canada, OPIC and IFC. Those agencies would mitigate Venezuela’s political and economic instability by providing political risk insurance.

However, the major funding source of the project was the American private placement market. Petrozuata received USD$ 1 bn of debt from the Rule 144A market. These bonds were chosen because of the additional advantage of speed and less onerous disclosure requirements imposed by the Securities and Exchange Commission.

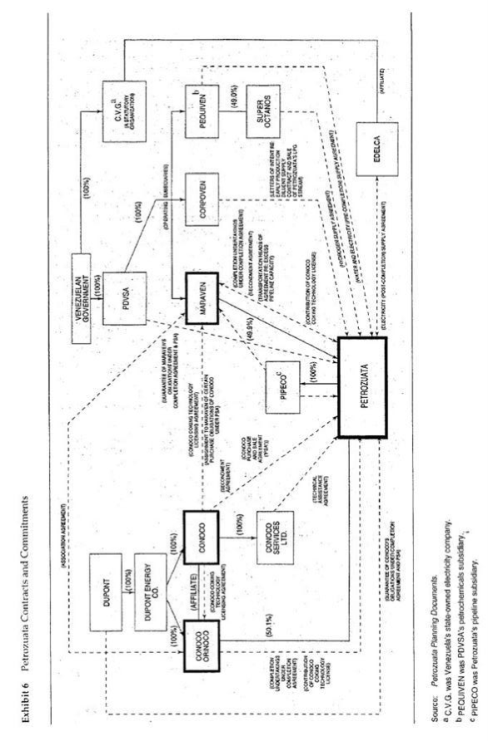

Petrozuata project had three main components: a series of inland wells to produce the crude, a pipeline system to transport the crude to the coast, and an upgrader facility to partially refine the crude. It was unusual and a highly complicated to finance multiple component projects on a standalone basis. A special system of contracts and commitments were designed and implemented to make the project feasible. A detailed scheme of contracts and commitments is provided in Figure 2.

For instance, sponsors mitigated the incentive problem and managerial inefficiency by creating a small board of directors comprised of two directors from each sponsor, and using compensation contracts for managers that were linked to the project performance. Also was realized the major benefit of project finance: public-sector management was substituted for private-sector.

The construction risk was allocated to sponsors. Conoco and Maraven agreed to provide funds for any cost overruns prior to completion. Also, the parent companies guaranteed these obligations. The guarantee has a unique structure in terms of the difference in ratings between parties – DuPont (AA-) and PDSVA (B). The parties agreed to include severe penalties for failing to meet their obligations and incentives to cover the other party’s shortfalls. It was a good example of how project finance could substitute the lack of development in emerging countries.

After construction would be completed, together with major risks, the sponsor guarantees would also end and the project would become non-recourse to the sponsors.

Figure 2: Petrozuata contracts and commitments

Source: (Esty 1998)

25

Secondly, sponsors considered within the budget, a USD$ 38 mn contingency for upstream facilities, a USD$ 139 mn contingency for downstream facilities, and sufficient funds to pay premiums on a construction all risk insurance policy covering up to USD$ 1.5 bn of physical loss or damage.

Another risk allocation mechanism in the current project was the use of an off-take agreement with the guarantee from the parent company DuPont. According to this agreement, Conoco took an obligation toward Petrozuata to purchase the first 86.6% of Petrozuata’s syncrude, for the whole 35-year life of the project, based on the market price. Moreover, the project company had the right to sell the syncrude to third parties if it could get a higher price. Such scheme eliminate ex post bargaining costs, and deter opportunistic behavior by providing incentives to both sponsors to act in the project’s best interest in the area where contracts would have been costly or impossible to write.

Also, with an arrangement authorized by the Venezuelan government the project had a prioritization of cash flows as a main element of the contractual agreements. Petrozuata’s customers would deposit their dollar-denominated funds from the purchases into and offshore account maintained by Banker Trust, governed by the law of New York. Afterwards, the Trustee would disburse the money according to a payment hierarchy. First, the Trustee would make the transfer to a 90-day operating expense account; second, to service the project’s debt obligations; and, third, make deposits to a Debt Service Reserve Account as needed to maintain six months of principal interest. Finally, the project implemented a “cash trap” basically meaning that if the project maintains an one-year historical and one-year projected Debt Service Coverage Ratio of 1.35X, then the Trustee would transfer any remaining funds to Petrozuata for distribution to its equityholders.

To sum up, Petrozuata is an example of the effective use of project finance in developing countries. The adverse circumstances following financial closure provide further evidence of the durability and merits of the project finance structure. The deal set numerous precedents in the bank and capital markets. For these

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this essay and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal