Japanese Asset Price Bubble

| ✅ Paper Type: Free Essay | ✅ Subject: Finance |

| ✅ Wordcount: 3048 words | ✅ Published: 04 Sep 2017 |

Introduction

A financial crisis is said to happen when an asset loses a huge part of its face value. This can prompt to an extensive variety of hostile outcomes such as currency crashes, fall in output and as worse as sovereign defaults. Such striking emergencies have been happening since fourth century BC and have proceeded on various scales and levels.

Among various crises, the Japanese asset price bubble was one of the greatest financial bubbles in history with incredibly increased stock and real estate prices. It is believed that the Japanese possess an ability to develop what they receive from the Americans. Unfortunately, the Japanese have taken up on crashes as well and made theirs much bigger than that of America.

This price bubble broke down in early 1992. The bubble was characterized by rapid increase of asset prices and overheated monetary movement, and additionally an uncontrolled cash supply and credit expansion. All the more particularly, over-confidence and conjecture regarding asset and stock prices had been closely connected with extreme monetary easing policy at that time.

By August 1990, the Nikkei stock index had plunged to a large portion of its crest by the time of the fifth monetary tightening by the Bank of Japan. By late 1991, prices of asset started to decline. Despite the fact that asset prices had clearly collapsed by mid 1992, the economy’s decline proceeded for over 10 years. This decline brought about an enormous aggregation of non-performing assets loans (NPL), bringing on challenges for various financial institutions. The bursting of the Japanese asset price bubble added to what many call the Lost Decade.

Main Causes That Led To The Crisis

Japan’s exceptionally traditional society faced substantial changes after they were defeated in the Second World War due, to a limited extent, to the Westernizing impacts of the possessing Allied Forces (Molasky, 1999).

Post World War 2, Japan’s booming export economy and strict fiscal strategies that were intended to encourage household savings brought about a cash surplus in the nation’s banking framework that in the long run prompted to more lenient lending.

The nation’s solid exchange surpluses and the Plaza Accord in 1985, which sought to debilitate the U.S. dollar against the Yen and German Deutsche Mark, made the Yen currency to appreciate against different currencies, which thus made foreign capital investments comparatively modest for Japanese organizations.

The blend of abundance liquidity in the banking system, financial deregulation and the nation’s export miracle inevitably prompted to overconfidence and over extravagance in Japan’s economy, which turned into the second biggest economy on the planet after the USA in only a couple of decades. Banks began to take extreme risks that were partly funded by 186 trillion worth of Yen acquired from different capital markets.

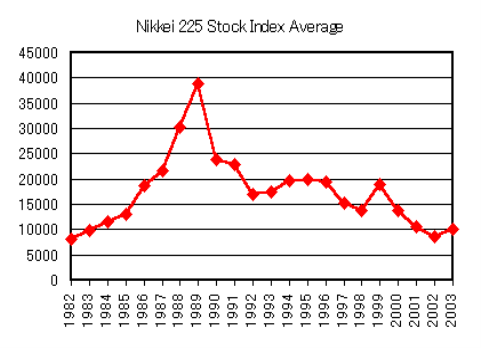

The Japanese stock price index started to ascend in the early 1980s and kept on ascending to more than five circumstances the 1980 level. Then, from 1990 it started a long stretch of decline with medium-term variations. From 1985 to 1989, Japan saw an increase in Nikkei stock index to 39,000, which was three times of the 1985 level and accounted for more than one third of the world’s stock market capitalization (Economist, 2011).

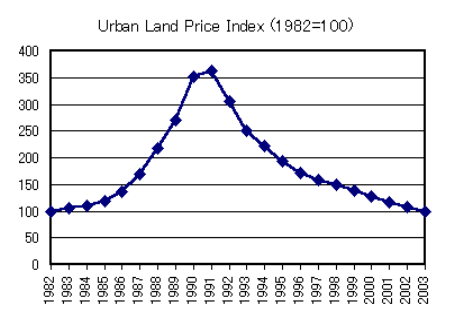

The Japanese land saw similar price movements however with little amplitude. The average land price witnessed an increase an increase that was double the previous price. One year later, in 1991, the land price began to decline.

There were various events that are considered responsible for causing the asset price bubble in Japan. Fukao (2001) and Kamigawa (2001) both consider financial deregulation as one of the major factors responsible in creating a favourable environment for a land price bubble, allowing firms to borrow severely in order to invest in commercial real estate, golf courses, private land and golf club memberships for households.

The increasing growth in terms of Japanese asset prices is firmly linked with a noteworthy fall in short-term interest rates, between 1986 and 1987. The Bank of Japan had dropped the official discount rate from 5.00% to 2.50%. The official discount rate stayed unaltered until May 30, 1989.

Post 1991, the land showed a decline and kept on falling till mid 1998, triggering the quality of loans to the real estate industry to worsen significantly. Besides, collateral value declined as before 1991, borrowers could acquire up to 90% of their land security, which dropped to half from 1991 to 1998, leaving 40% of such credits revealed. Loans to industries with land as their collateral became non-performing, leading to the bad-loan problem of Japanese banks (Hoshi 2001).

The value of problem debt was recalculated by Financial Supervisory Agency (FSA) as 123 trillion yen (Lincoln 1998), raising the ratio of bad debt to GDP to 25 percent.

Impact of Japanese Asset Price Bubble

The years from 1991 to 2000 are referred to as the Lost 10 Years or the Lost Decade in which the Japanese asset price bubble collapsed within its economy. The explosion of the Japanese Asset Price Bubble activated materialization of adverse effects, which made the structural adjustment further arduous, thereby leading to a downward move in growth trend in the 1990s. This further reduced the asset price beyond the boom-bust cycle. It took longer to recover from the impact of these events because the new conditions imposed by the new environment were not favourable to the Japanese management style at that time.

In this incident, the economy undesirably failed to resuscitate. Although, in the beginning there was a recovery in spending due to the instantaneous impact of the consumption tax hike wore off. Unfortunately, in late 1997 output toppled again and remained to fall all along the whole year of 1998. Japan had experienced the worst recession due to this downturn. After the consumption tax hike in 1997, the unexpected shock led to a terrible reduction in household spending. Also, in the later part of the year, weakness was aggravated due to the financial factors which consisted of several failures of the large firms as well as the failure of the major banks. Moreover, the increased in crisis in emerging markets of Asia disable external demand which led to additional blow to confidence.

Even though there was a shift towards macroeconomic policies yet recession perpetuated 1998. In the beginning of the 1999, the interest rates were taken down to nearly zero and consistent amount of fiscal stimulus embossed fiscal deficit of general government to about 10 percentage of GDP. At last, in 1999 the economy again started to recoup. The turnaround was started by a blast of open venture spending ahead of schedule in the year and recuperation of buyer confidence as compelling activity by the government to manage feeble banks and infuse public capital into the banking system mitigated fears of financial crisis. Nonetheless, a rapid increase in the yen from its low point in mid-1998, connected to a limited extent to external improvements and in addition enhancing sentiment about the Japanese economy, has raised worries about the effect on the still delicate recuperation and prompted to calls for further facilitating of monetary policy even though short-term interest rates are as of now practically at zero.

Furthermore, a wide scale of Japanese economy is until now recuperating from the effects of the 1991 collapse. Japan also lacked in terms of producing a significant level of output per capita. In 1991, Japan had a higher percentage than Australia in real output per capita but unfortunately in 2011 Japan was overpowered by Australia. Japan was a global leader in gross output as well as labour efficiency. However, in a period of 20 years, Japan was overtaken in both the areas. Moreover, it costed them 12 excruciating years for Japan’s economy to revive back to its original level as was in 1995.

Policy Response to The Crisis

Initially the Ministry of Finance of Japan implemented a policy that aimed at safeguarding the weak banks through regulatory forbearance as well as other forms of monetary support while buying time for an anticipated revival of the economy and asset prices. The very first bank failure to take place in the post war period in Japan was the crash of Toho Sogo Bank in 1991. This was followed by collapse of other small financial institutions in 1995-1996. However, in those years, the government shelled out JPY 680 billion to help the jusen and non-banking housing loan companies to recover. This policy came under a lot of criticism as it aimed at aiding only the nonbanking financial institutions.

In the June of 1996, the Deposit Insurance law was amended to bolster the deposit insurance system that consisted of a brief suspension of limits on deposit protection which was initially till March 2001 but was later extended to 2002 after which it was further prolonged till March 2005. The amendment of the Deposit Insurance Law also led to an increment in the insurance premium from 0.012% to around 0.84% on all deposits that were outstanding. This was primarily done to manage the problems of credit cooperatives instead of the major banks.

In the December of 1997, the government declared that up to JPY 30 trillion of public funds will be made accessible to the Deposit Insurance Corporation of Japan (DICJ) by 1998 March. This consisted of JPY 13 trillion to revitalize the bank balance sheets while JPY 17 trillion were to boost the deposit insurance system. The funds were increased to a total of JPY 60 trillion which was higher than 12% of the country’s GDP to assist the banks in 1998 October.

In March 1998, 21 prime banks were rendered with JPY 1.8 trillion to help them meet the requisite capital adequacy standards. Regardless, the government interceded to aid two major banks namely Nippon Credit bank and the Long-Term Credit Bank of Japan which had to be provisionally nationalized in October 1998 as they faced difficulty in managing their loan portfolio post the bubble period.

However, JPY 1.8 trillion was not sufficient to completely revive the ailing banking system. Thus, the government injected JPY 7.5 trillion more funds into 15 banks by the March of 1999. By the April of 1999, the banking system experienced a little stability for the first time after the lost decade and the “Japan Premium” reduced considerably. An authorized inspection manual was released by the Financial Regulatory Authority which enforced the banks to endorse stricter asset classification of NPLs.

The Bank of Japan decided to implement a zero-interest rate policy (ZIRP), after nearly two decades of stagnant growth rate, to tackle the deflation and boost up the economy. ZIRP is a technique to keep the interest rate close to zero while at the same time triggering economic growth. The Central Bank, under this policy, cannot reduce interest rates anymore thus leaving the traditional monetary policy futile. Thus, the unconventional monetary policy like quantitative easing is used effectively to expand the monetary base. In 1991, the consumption and investment looked promising. The GDP growth rate was up by 3% while the interest rates were secure at 6%. However, after the tumbling of the stock prices in 1992, the Japanese economy experienced stagnation. The Consumer Price Index, a standard to measure inflation rate, fell from 2% to 0% by 1995, at the same time the period interest rates plunged to 0%. Therefore, the ZIRP was unable to revive the economy from deflation and stagnation hence leading japan into a liquidity trap. Despite the unsuccessful run of the ZIRP, this policy is still used in Japan till date.

Lessons Learnt and What Could Have Been Done Differently

The after math of the crisis led to the zombie decade. An era in the Japanese economy that took years to overcome once the bubble burst. There were many lessons that could be learnt from the collapse of the bubble. These can be classified into two categories. The first one being the lessons that were learnt towards the prevention of the bubble and the second being the lessons learnt from the handling of the bubble. This section will analyse the ramification the bubble had and how such an incident could be avoided in the future.

It is always important to gauge the sustainability of economic and financial systems while assessing economic risks. During the bubble period, there was no stress testing when it came to the banking system. This can be seen through the analytical value of risk (VaR) done by Shimizi and Shiratsuka (2000) to predict the magnitude of non-performing assets in the Japanese banking system. It is essential for banks and central banks to perform stress tests to prevent further collapses through the formation of bubbles. Although it is necessary for banks to restructure their debt, it is essential to note that if zombie firms stick around in the market, the shrinkage of the businesses will be lasting. Caballero, Hoshi and Kashyap (2008).

The central banks can act pre-emptively when it comes to matters of potential inflationary pressure Bernanke and Gertler (1999). There was an excessive amount of inflationary pressure that existed in the Japanese economy. Taylor (1993) gave the rule, named the Taylor rule as a guide post for central banks to deal with asset price fluctuations. According to the Taylor Rule, the operational target levels of interest rates must be set based on the divergence of the output gap and the inflation rate when held at equilibrium.

During the end of the bubble there was an upswing in the money supply and credit and not much attention was given to it. This is an indicator to signal an increase in interest rates; which the Bank of Japan did not pay heed to. Therefore, it is significant to pay close attention to the conduct of the monetary policy in avoiding unpleasantness in the economy.

There was a lack of regulation in the part of the government in managing credit risk products. To gauge the extent of a banking crisis, the total amount of loan losses should be aggregated at the earliest. This gives the agencies and policy makers an idea about the extent of the crisis and act accordingly. Fuji and Kawai(2010) suggested that once the value of NPLs has been gauged, recapitalization should be done at a faster rate than it was conducted in Japan. According to Caballero, Hoshi and Kashyap (2008), theoretically, this is possible, but practically it takes longer and most of the publicly funded recapitalization programs need parliamentary/senate approval so at times it is too late as the market developments outpace the recapitalization process.

Steps Taken to Prevent Similar Crisis

There has been various crises after the crisis in Japan, but the lessons learnt here have been implemented across the world to mitigate the effect of crisis or to prevent them to some extent.

Krugman (1998) said that the Japanese Asset Bubble Crisis was like a “full dress rehearsal” or a blue print for prevention and handling of further crisis. He was right in saying so. The policies and the measures taken were mirrored and implemented across the world, most notably in Sweden, Germany, USA, and England. IMF also departed from its austerity stance for an expansionary fiscal and monetary policy. The European Central Bank implemented a series of Quantitative Easing programs.

In Sweden, the vice president of the Swedish Central Bank, Riksbank implemented one of the most expansionary monetary policies as a counter to the crisis in the US. The interest rates were dropped from 4.5% to 0.25%. Currently, they are negative, which could be considered as a repercussion of the policy implemented. The quick and unconventional response aided the economy during the time of crisis. Elmer, Nessen, Guibourg, and Kjelleberg(2012)

The US and Japan, both have a negative feedback loop when it comes to the economy. Although the economic conditions across the globe were different when both the crisis are compared, but it almost seemed like déjà vu, when it came to dealing with the crisis. Both countries had taken similar measures, although the US was quicker in implementing it. The USA adopted the policy of public capital injections quicker, thus preventing the crisis from becoming deeper and more severe. On the monetary policy front, the US had been more aggressive in lowering rates. Shirakawa (2008).

In 2015, European Central Bank President Mario Draghi implemented quantitative easing. This was done to revitalise the EU economy, wake it up from the slump it was undergoing, to stimulate the depreciating Euro and counter deflation. Although it had many critics, it has been successful and has helped in preventing a full-blown crisis.

Conclusion

The research study of the crisis suggests that the government of Japan failed in handling the banking sector issues in 1990s in a timely and critical manner since the crisis developed slowly and the gravity of the matter was underestimated. The government had a positive prediction for the growth while no domestic or external pressure prevailed during that time as well as there was a lack of a systematic legal framework to aid ailing banks.

However, post the crisis, the authorities became more assertive in dealing with the problems. Several policies were introduced by the government to help revive the economy. They also implemented an extensive legal framework for bank resolution to help the distressed banks.

Essentially, deterioration of the real economy can lead to another round of financial crisis, which can further damage the real economy. If the authorities do not address the banking sector problem promptly, then the crisis may prolong, and a full-fledged economic recovery will be significantly delayed. This could result in a “lost decade” for the economy.

References

Fujii, K., Fujii, M. and Kawai, M. (2010) ADBI working paper 222 Asian development bank institute. Available at: https://www.adb.org/sites/default/files/publication/156077/adbi-wp222.pdf (Accessed: 19 February 2017).

Fund, I.M. (2000) Post-bubble blues–how Japan responded to asset price collapse. Available at: https://www.imf.org/external/pubs/nft/2000/bubble/ (Accessed: 19 February 2017).

Nath, T. (2015) ‘What is Zero interest-rate policy (ZIRP)?’, in Available at: http://www.investopedia.com/articles/investing/031815/what-zero-interestrate-policy-zirp.asp (Accessed: 19 February 2017).

Bubble burst (no date) Available at: http://www.grips.ac.jp/teacher/oono/hp/lecture_J/lec13.htm (Accessed: 19 February 2017).

compuirv (2017) The Japanese deflation myth • inflation matters. Available at: http://inflationmatters.com/japanese-deflation-myth/ (Accessed: 19 February 2017).

JAPAN’S BUBBLE ECONOMY (1992) Available at: http://www.sjsu.edu/faculty/watkins/bubble.htm (Accessed: 19 February 2017).

Japan’s bubble economy of the 1980s (2017) Available at: http://www.thebubblebubble.com/japan-bubble/ (Accessed: 19 February 2017).

Revolvy, L. (no date) ‘Japanese asset price bubble’ on Revolvy.Com. Available at: https://www.revolvy.com/main/index.php?s=Japanese%20asset%20price%20bubble&item_type=topic (Accessed: 19 February 2017).

The causes of the Japanese lost decade: An extension of graduate thesis (no date) Available at: http://daigakuin.soka.ac.jp/assets/files/pdf/major/kiyou/16_keizai3.pdf (Accessed: 19 February 2017).

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this essay and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal