Internal Audit Effectiveness Study on the Public Sector

| ✅ Paper Type: Free Essay | ✅ Subject: Accounting |

| ✅ Wordcount: 2978 words | ✅ Published: 25 Apr 2018 |

- Agus Setiawaty

Determinant of Internal Audit Effectiveness in Public Sector Organizations: Which factors matter?

Abstract

Internal audit (IA) play a pivotal role in reinforcing good governance in both public and private organizations through a value-adding role. Yet very few research conducted on the IA effectiveness especially in public sector. The current study aims to examine empirically determinant of effectiveness of IA within organization. Effectiveness scale developed through structured interview with top manager before delivered to real participant. Data in this study collected through questionnaire given to top manager and internal auditor to explore participant perception on IA effectiveness and its determinants. Conventional multiple regression and path analysis is used to examine the association between internal audit effectiveness and four principal factors, namely; professional proficiency, quality of audit work, independence of audit internal department and top management support.

Keywords: internal audit effectiveness, effectiveness scale, good governance, balanced scorecard

INTRODUCTION

Internal Audit (IA) facing higher demands in the line of duty. The role of internal audit now is not only overseeing the operational of organization activities, but has been extended to support the organization through evaluating and improving risk management, control and governance process (IIA, 2004). In this concept, the existence of internal audit is needed by management in order to help them to provide assurance that any risks in organization were identified and prevented effectively, and organizational activities has been controlled in effective and efficient ways. Moreover, Ridley (2008) declared that the construction of modern IA derived from the three “E”s concept namely effectiveness, efficiency and economy, which defined by as doing the right thing for effectiveness, efficiency describe as doing them well to describe efficiency and doing them cheaply for economy. Of all three factors, effectiveness is viewed as the most important factor because ineffective IA will ultimately cause to futile regardless how efficiently or economically the service is being provided. IA effectiveness is defined as a “risk-based audit that support the organization to achieve its objectives through significantly influencing the corporate governance quality” (Lenz, 2013). Effective IA is expected to encourage the formation of good governance within organization.

The changing of IA role from compliance and safeguarding assets to value-added audit also impact that role in public sector organizations. However, some research findings (Mihret and Woldeyohannis, 2008; Cohen and Sayag, 2010) show that this role has not been effectively implemented in public sector organizations. In Indonesia context, audit findings issued by supreme audit board reveal that there is still problem relate to internal control in government institution although financial statement has been given unqualified opinion. These condition lead to the question about the effectiveness of internal audit function and further the related factors contribute to the IA effectiveness.

The purpose of this study is to empirically investigate determinant of effectiveness of IA in public sector, an important concept rarely examined in the scientific literature. Most of previous study focused examining IA effectiveness empirically in the private institution (Cohen and Sayag, 2010; Arena and Azzone, 2009; Karagiorgos, Drogalan and Giovanis, 2011) while research on IA conducted in the context of the public sector has been done with a qualitative approach (Mihret and Yismaw, 2007; Mihret and Woldeyohannis, 2008), none has to conduct it empirically. To the best of our knowledge, there has never been a previous research which examines the determinants of the internal audit effectiveness in Indonesia context especially in public sector. Therefore, according to study of Cohen and Sayag (2010), this research will examine relevant factors to IA effectiveness with development in IA measurement using balanced scorecard framework proposed by Frigo (2002). This measurement claim to be more comprehensive in describing the effectiveness of IA in a organization than used in previous research.

This study contributes to the literature by developing a conceptual understanding of IA effectiveness in public sector organizations using comprehensive framework of balanced scorecard which address fundamental issues influencing IA effectiveness in public sector context. This research also contributes to the literature by exploring the determinants of IA effectiveness. It is important to understand which factors determine IA effectiveness because of virtuous influence of effective to organizational performance (Mihret, James and Mula, 2010).

This is a proposal paper, consequently, in the next section of this paper, the discussion address to relevant literature on IA Effectiveness and development of research expectation, followed by discussion of research methodology.

CONCEPTUAL FRAMEWORK AND RESEARCH EXPECTATION

The importance of internal audit function has been realized as an essential contributor to effective corporate governance and quality external financial reporting (Prawitt, Smith and Wood, 2009). The Institute of Internal Auditor (IIA) model offers IA as a key element of establishing high quality corporate governance, as well as management who principally responsible for regular monitoring of management’s actions . As mentioned previously, The IIA has extended main function of IA to value adding focus by ensuring compliance to policies, rules, and regulations, which are largely of a financial nature, and by working in partnership with management to help improve operations and manage risk. Although the value-adding notion of IA is assumed shape the IA more effective, this is never guaranteed. In fact the literature suggests that IA effectiveness more influenced by the situational dynamics factor in audit environment (Mihret et al, 2010).

Internal Audit Effectiveness

As mentioned above, IA function has received greater attention according to its vital contribution to good governance, surely also occur in public sector context. Therefore, effective is needed for answering that challenge. There are two main approaches to the concept of IA effectiveness. The first approach associates effective IA with compliance to some set of auditing standard, such an approach proposed by Sawyer (1988) who assert five standard internal auditing, namely: interdependence, professional proficiency, the scope of work, the performance of the audit and management of the internal audit department. The second approach linking IA effectiveness with subject evaluations from management who act as supply side. In later approach, development of systematic and general valid measurement is needed to gauge IA effectiveness (Schneider, 1984; Dittenhofer, 2001). The early effort was conducted by Hoag (1981) through designing questionnaire to gain feedback about internal auditing performance from management. The measurement of effective IA consist of planning and preparation, the quality of audit report, the timing of the audit, and qualify communication between the relevant parties.

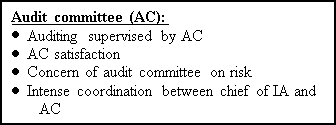

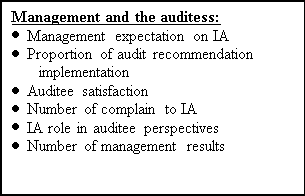

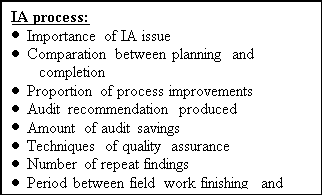

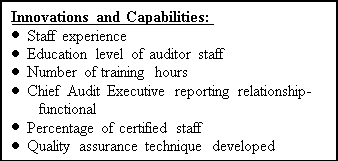

Study accomplished by Albrecht, Howe, Schueler and Stocks (1988) which sponsored by The IIA identified 15 factors contribute to the evaluation of IA effectiveness, such as the congruence between auditing work and the goal sets of managers, competence of internal auditor, support from top management to IA function, and several characteristics of IA department. More recently, Ziegenfuss (2000) developed a questionnaire which comprises 84 effectiveness criteria classified into four groups: the IA environment, input, process and output. Results of the study identified five top performance measures, that is: staff experience, supervision form audit committee, management expectation on IA function, audit recommendation followed up by management, and auditor education level. The development of effective IA measurement continue to evolve and sensitive to current issue so that Frigo (2002) introduced balanced scorecard (BSC) framework. For constructing the model, Frigo (2002) confirm his premises with BSC concept which built from IA customer perspective, internal audit process, innovations and capabilities. Model developed by Frigo (2002) will be presented next.

This study modifies model proposed by Frigo (2002) to precisely adapt with public sector context. Modification is made to audit committee factor because its existence prevail in private institution. As noted before, research on the effectiveness IA is restricted to private sector companies while study in public sector have accomplished qualitatively. The current study takes this line of research a step further by designing and testing such a scale to gain understanding of IA effectiveness in public sector.

Determinant of IA Effectiveness

Determinant in this study adopted from the model proposed by Lenz and Hahn (2015) which divides effective IA determinant into micro and macro factors. However, this research largely focus the discussion in micro factor. Micro factor categorized into four factors: IA resources, IA process, IA relationship and organization. IA resources measured by staff professional proficiency (Prawitt, 2003; Cohen and Sayag, 2010; Mihret et al, 2010; Pforsich, Kramer, and Just, 2006,2010; Soh and Martinov-Bennie, 2011), IA process explained by quality work of IA department (Cohen and Sayag, 2010), while IA relationship and organization illumined by top management support (Halimah, Othman and Kamaruzaman, 2009; Christopher, Sarens and Leung, 2009; Mihret and Yismaw, 2007, Cohen and Sayag, 2010) and organizational independence (Mihret et al, 2010; Cohen and Sayag, 2010), respectively.

Professional proficiency of internal auditor

The IIA’s Standards for Professional Practice of Internal Auditing require that internal auditors possess the knowledge, skills and expertise needed to accomplish audit work (Institute of Internal Auditors, 2008). Technical competence and continuous training are considered essential for effective IA. Consistent with this thinking, Gramling and Meyers (1997) found that certified internal auditors is perceived as an expert auditor which reflect auditor’s competence. Professional such as auditor requires a set of expertise in conducting their complicated duty that collectively granted from education, training, experience and professional qualifications (Al-Twaijry, Brierley and Gwillian, 2003). The few studies that concern to this issue indicated that the greater the professional competencies of the IA staff, reflected by their professional training and educational level, the more effective IA department (Albrecht et al. 1988). Nanni (1984) at the same ways, found that auditor experience positively impact the evaluations process of internal accounting control. Therefore, it es expected that Greater professional proficiency of staff within the internal audit department will be related to greater auditing effectiveness (H1).

Quality of audit work

Compliance with standards, policies and procedures is main concern of internal auditor. One of IA objectives is ensure that company’s activities accordance with predetermined rules. Glazer and Jaenike (1980) in Cohen and Sayag (2010) asserted that audit work which sufficiently perform according to internal auditing standards contributes significantly to the effectiveness of auditing. The similar point also claimed by Ridley and D’Silva (1997) that complying with professional standards is the most important contributor to IA’s added value. It can thus be argued that greater quality of IA work -defined by compliance with formal standards, as well as a high level of efficiency in the audit’s planning and execution – will improve the audit’s effectiveness (H2)

Independence of IA department

Independence has long been seen as a crucial factor in conducting audit role. Although initially only intended for the independence of the external auditor, but lately also addressed to the demands of the independence of internal audit, something that might be a serious problem because of auditor position and responsibility lay on under management. The independence of the internal audit department has been identified as a key element of audit effectiveness. Van Peursem (2005), based on interviews with Australian internal auditors, concluded that independence from management is a dominant feature of successful auditing programs. Those auditors able to set their own. It can thus be argued that organisational independence will increase the internal auditor’s effectiveness (H3).

Top Management Support

The interaction and relationship between top management and internal auditors is both important and complicated. Management support to IA is considered as a determinant of IA effectiveness (Mihret and Yismaw, 2007). This support could, for instance, be by allocating sufficient human and material resources to IA. It could also be by showing the level of cooperation offered by management. Greater level of auditee cooperation will influences the extent to which IA properly accomplishes its objectives (Al-Twaijry et al., 2003; Mihret and Yismaw, 2007). the relationship between the internal audit staff and the company’s management is clearly important in determining the independence and objectivity of the internal auditor (Al-Twaijry et al. 2003;IIA 2006).Management support for IA is thus important both in the abstract (managers must see the activity of the audit department as legitimate) and in ensuring that IA departments have the resources needed to undertake their duty. Therefore, it is argued that higher support from top management, the more effective the IA (H4).

RESEARCH DESIGN

The participants

The target population for this study is managers and internal auditor from all Indonesian public sector organizations that conduct internal audit. Data in this study will be acquired through questionnaire which will be initially tested for validity and reliability before delivered to each participant. Each organization will accept two questionnaires, one for manager (deal with IA effectiveness) and the other for auditor (answering for independent variables).

Variabel measurement

Effectiveness of internal auditing

Given the lack of IA effectiveness research in public sector organizations, this study will developed own effectiveness scale based on BSC framework proposed by Frigo (2002), supporting with measurement scale fostered by Ziegenfuss (2000). In this study, new effectiveness scale will be designed and adjusted with Indonesian auditing environment. Structured interview will be undertaken with several public sector top managers to gain advice and consideration about developed questionnaire before it comes to statistic analysis for the validity and reliability assessment.

Independent variables

Professional proficiency, measured by four indicators, consist of educational qualifications, professional certification, work experience and continuous development,

Quality work, measured by six indicator, comprises of annual audit plan, access to all organization, significance of audit, auditee response, follow up action, additional activities performed.

Independence, measured by nine items, these being: independence level, reporting level, direct contact to senior management, conflict of interest, interference, unrestricted access to all departments and employees, appointment and removal of the head of internal audit, and performing non-audit activity.

Top management support, measured by four factors, those are: involvement in the internal audit plan, providing management with reports about the work the internal audit team performs, the management’s response to internal audit reports, the resources of the internal audit department.

Data Analysis

Two methods of data analysis will used in this study. First, straightforward OLS multiple regression (Ghozali, 2013) was performed to estimate the magnitude of the effect of the independent variables, the four factors identified above, on the effectiveness of internal audit (the dependent variable). Second, beyond the straightforward use of conventional OLS multiple regression, path analysis (Ghozali, 2013) was conducted to investigate further the associations and linkages among the variables of interest.

References

Al-Twaijry, A.A.M., Brierley, J.A., & Gwilliam, D.R. (2003). The development of internal audit in Saudi Arabia: an institutional theory perspective. Critical Perspectives on Accounting, 14 (5), 507-31.

Arena M., & Azzone G (2009). Internal audit effectiveness: Relevant drivers of auditees satisfaction. Sixth European Academic Conference on Internal Auditing and Corporate Governance. London. Retrieved from http://www.cass.city.ac.uk/__data/assets/pdf_file/0003/37335/Marika-Arena.pdf.

Christopher, J., Sarens, G. & Leung, P. (2009). A critical analysis of the independence of the internal audit function: Evidence from Australia. Accounting, Auditing & Accountability Journal, 22 (2), 200-220.

Cohen, A., & Sayag, G. (2010). The effectiveness of internal auditing: An empirical examination of its determinants in Israeli organizations. Australian Accounting Review, 20 (3), 296-307.

Dittenhofer, M. (2001). Internal auditing effectiveness: An expansion of present methods. Managerial Auditing Journal, 16, 443-50.

Frigo, M.L. (2002). A balance scorecard framework for internal auditing departments (Paperback). The Institute of Internal Auditors Research Foundation. Altamonte Springs. Florida.

Ghozali, Imam. (2013). Aplikasi analisis multivariate dengan program SPSS. Semarang: Badan Penerbit Universitas Diponegoro, Semarang.

Gramling, A.A., & Myers, P.M. (1997). Practitioners’ and users’ perceptions of the benefits of certification of internal auditors. Accounting Horizons, 11 (1), 39-53.

Halimah, N.A., Othman, R., & Kamaruzaman, J. (2009). The effectiveness of internal audit in Malaysian public sector. Journal of Modern Accounting and Auditing, 5 (9), 53-62.

Hoag, D.A., (1981). Measuring audit effectiveness. Internal Auditor, April: 70-8.

Institute of Internal Auditors. (2004). Definition of internal auditing. Retrieved from https://na.theiia.org/standards-guidance/mandatory-guidance/Pages/Definition-of-Internal-Auditing.aspx.

Institute of Internal Auditors Belgium (2006). Internal audit in Belgium: the shaping of internal audit today and the future expectations – survey results. Retrieved from: www.iiabel.be/.

Institute of Internal Auditors. (2008). International standards for the professional practice of internal auditing. Retrieved from: www.theiia.org/guidance/standards-and-practices/professional-practices-framework/standards/standards-for-the-professional-practice-ofinternal-auditing/.

Karagiorgos, T., Drogalas, G., & Giovanis, N. (2011). Evaluation of the effectiveness of internal audit in Greek hotel business. International Journal of Economic Science and Applied Research, 4 (1), 19-34.

Lenz, R., & Hahn, U. (2015). A synthesis of empirical internal audit effectiveness literature pointing to new research opportunities. Managerial Auditing Journal, 30, 5-33.

Lenz, R. (2013). Insights into the effectiveness of internal audit: a multi-method and multi-perspective study. Dissertation at the Université catholique de Louvain – Louvain

School of Management Research Institute. Retrieved from https://drrainerlenz.files.wordpress.com/2013/03/2013-02-rainer-lenz-public-defense.pdf

Mihret D. G., & Yismaw A. W. (2007). Internal audit effectiveness: An Ethiopian public sector case study. Managerial Auditing Journal, 22 (5), 470-484.

Mihret D. G., & Woldeyohannis G.Z. (2008). Value-added role of internal audit: An Ethiopian case study. Managerial Auditing Journal, 23 (6), 567-595.

Mihret, D. G., James, K., & Mula, J. M. (2010). Antecedent and organizational performance implications of internal audit effectiveness. Pacific Accounting Review, 22 (3), 224-252.

Nanni, A.J. (1984). An exploration of the mediating effects of auditor experience and position in internal accounting control evaluation. Accounting, Organizations and Society, 9, 149-63.

Prawitt, D.F. (2003). Managing the internal audit function. IIA Research Foundation, Altamonte Springs, FL. Retrieved from: https://na.theiia.org/iiarf/Public%20Documents/Chapter%206%20Managing%20the%20Internal%20Audit%20Function.pdf

Pforsich, H.D., Peterson Kramer, B.K., &Just, G.R. (2006). Establishing an effective internal audit department. Strategic Finance, 87 (10), 22-29.

Pforsich, H.D., Peterson Kramer, B.K., & Just, G.R. (2008), Establishing an internal audit department: The case of the Schwan food company. Global Perspective on Accounting Education. 5, 1-16.

Prawitt, D., F., Smith, J., L., & Wood, D., A. (2009). Internal audit quality and earnings management. The Accounting Review, 84 (4), 1255-1280.

Ridley, J., & D’Silva, K. (1997). A question of Values. Internal Auditor, June: 16-19.

Ridley, J. (2008), Cutting edge internal auditing, John Wiley & Sons, Ltd, Chichester, England. Retrieved from: http://www.gbv.de/dms/zbw/548154120.pdf.

Sawyer, L.B., (1988). Sawyers’ internal auditing. Institute of Internal Auditors. Altamonte Springs, FL.

Schneider, A. (1984). Modeling external auditors’ evaluations of internal auditing. Journal of Accounting Research, 22, 657-78.

Soh, D.S.B., & Martinov-Bennie, N. (2011). The internal audit function, perceptions of internal audit roles, effectiveness and evaluation. Managerial Auditing Journal, 26 (7), 605-622.

Van Peursem, K.A., (2005). Conversations with internal auditors, the power of ambiguity. Managerial Auditing Journal, 20 (5), 489-512..

Ziegenfuss, D.E. (2000). Measuring Performance. Internal Auditor, February: 36-40. Retrieved from http://findarticles.com/p/articles/mi_m4153/is_1_57/ai_62599893/?tag=content;col1.

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this essay and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal