Costcutter Business Analysis

| ✓ Paper Type: Free Assignment | ✓ Study Level: University / Undergraduate |

| ✓ Wordcount: 1236 words | ✓ Published: 12 Oct 2017 |

Introduction

The firm under consideration is Costcutter Supermarkets, a chain of small supermarkets founded in 1986. It now has 1200 stores in the UK and has a European presence with 65 stores in Southern Ireland and 52 in Poland. This assessment focuses on Costcutter’s operations in the UK market.

Source: www.costcutter.co.uk

The UK Supermarket Industry – background

The UK supermarket industry is semi-oligopolistic with a small number of very large multi-store firms (e.g. Tesco, Sainsbury, Asda, Morrisons) dominating the market. Tesco is the largest grocery retailer in the UK, having overtaken Sainsbury in the 1990s.It has around 800 stores with a variety of formats, varying in size from an average of around 2000 square feet of net sales area for Tesco Express stores to 80,000 square feet for Tesco Extra stores. Costcutter store sizes are more comparable to the Tesco Express stores.

Market structure and competition

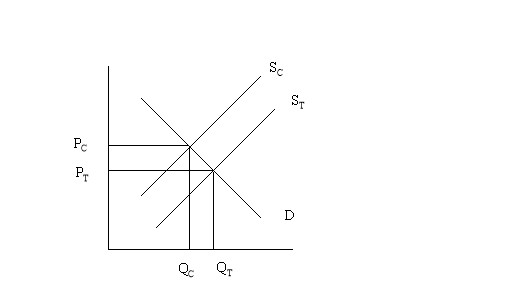

Costcutter faces fierce competition on price by the four large supermarket firms and therefore has to differentiate its products/services in ways other than price in order to be competitive in this market. Because the four large multi-store supermarket firms in the market benefit from huge economies of scale, the supply conditions they experience are different from those of Costcutter and other smaller chains. This is likely to mean that Costcutters supply curve is higher than that of Tesco, for example. The situation is illustrated in the diagram below where SC is the supply curve for Costcutter Supermarkets, ST is the supply curve for Tesco Supermarkets, D is the demand curve. This shows that the equilibrium price for Costscutters (PC) is higher than the equilibrium price for Tesco (PT) and the corresponding quantity (or output) is lower for Costcutter than Tesco.

However, it may also be possible that the two firms have different demand curves since the product is not identical. Although they may sell the same brands etc (i.e. literally the same stock), the overall product may be different because of the location of the firm’s stores and the service provided (e.g. longer opening hours represent increased convenience and can, therefore, shift the demand curve upwards). Supermarket products are mostly normal goods and therefore have a positive price elasticity of demand.

Industry cost structure

The cost structure of supermarkets is such that the fixed costs are limited (in the short and medium term) to building costs and staff overheads (in the long run, even these are not fixed). The key variable costs are stock. However, staff employed on casual or flexible contracts whereby their working hours can be changed at short notice may also represent variable costs. Because a high proportion of costs are variable, firms within the industry can react quickly to changes in demand without incurring too high costs (or corresponding significant changes in the supply curve). However, this only works for relatively small changes in demand. If there is a huge contraction in demand, the fixed costs (building rent, staff costs etc) will become much higher as a proportion of overall costs. Conversely, a big expansion in demand may require larger premises and this is not achievable in the short and medium term.

Problems facing the industry in the next five years

Grocery store saturation

In many areas of the UK, grocery store saturation is approaching (Guy 1996) and there is limited scope for existing firms to expand by opening new stores. According to DEFRA (2006), ‘a stable population limits growth of food consumption, although trends vary between food types as demographics and consumer preferences change (e.g. more single-person households; increasing awareness of health issues)’ and ‘food expenditure (other than eating out) accounts for a declining share of household budgets.’ Over the next five years, grocery store operators will have to consider alternative methods of expansion.

Competition

The large multiple retailers, especially Tesco and Sainsbury’s have recently moved into the convenience sector thus entering into direct competition with firms such as Costcutter (and Spar) which have been specializing in this sector for some time. Tesco and Sainsbury’s are likely to continue their expansion in the convenience sector and this means the product (or service) Costcutter is offering (e.g. longer opening hours, close to home etc) will become less and less differentiated from that of these very large multi-store firms.

Internet shopping

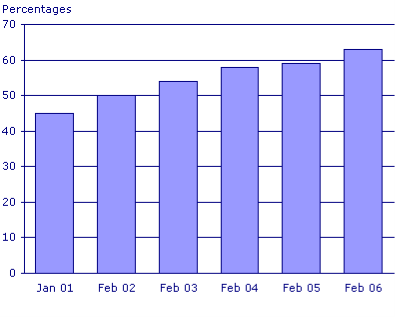

The growth of internet shopping is likely to continue over the next five years and the big multiple store retailers have already established themselves in this market. This is taking convenience shopping to a new level – instead of opting to shop at a store which is close to home, the ultimate in convenience for a shopper is to have groceries delivered to the door. As more and more people are getting broadband internet at home, and becoming more confident using the internet for a variety of tasks, the market for internet shopping looks set to grow massively over the next five years.

Adults who have used the Internet in the 3 months prior to interview, GB

Source: http://www.statistics.gov.uk/cci/nugget.asp?id=8

Business Strategy

In order to expand, Costcutter would be well advised to consider methods of expansion other than increasing the number of stores within the UK as in most areas of the UK the market is approaching saturation. Before opening any new stores, Costcutter needs to carefully consider the local market to check whether there is sufficient local demand to justify opening an additional store in that area or whether competition from the convenience stores operated by the larger firms will be too fierce. Where it is not appropriate to open a new store, Costcutter should consider how they can expand or increase profitability by alternative methods. For example, Costcutter should research into changes in consumer preferences and demographics and adjust their products and services accordingly. This may involve expanding the range of premium brands that are stocked. As incomes increase, so does the demand for ‘luxury goods’. Therefore this is one potential area for expansion. The increase in single-person households may effect the demand for convenient, quick, one person ready meals and so Costcutter should also consider stocking a bigger range of these products. Furthermore, Costcutter may benefit from diversifying into non-grocery products and services.

As the larger firms continue their expansion into the convenience sector, Costcutter should ensure that they maintain a differentiated service since they cannot compete on price. Costcutter should seek to carve out a niche in the market which may come from gaining a reputation for excellent customer service, a good own brand luxury product range, or the provision of additional services such as dry-cleaning or DVD rental.

Costcutter should investigate the possibility of entering the internet shopping market. IT may be that it would be too difficult or unprofitable for Costcutter to compete with the larger firms in this market but they should undertake a cost-benefit analysis to find out before they decide either way. Over the next five years, this is likely to be the fastest growing area of retail shopping and if Costcutter is going to enter the market, they should consider doing so sooner rather than later in order to establish their brand in this market.

Bibliography

Costcutter (2006) www.costcutter.co.uk

DEFRA (2006) ‘Economic Note on UK Grocery Retailing’ (downloaded from http://statistics.defra.gov.uk/esg/reports/agri.asp on 10 August 2006)

Guy (1996) ‘Grocery store saturation in the UK – the continuing debate’, International Journal of Retail & Distribution Management 24(6)

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this assignment and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal