Strategic Options After Conducting Environmental Analysis

| ✅ Paper Type: Free Essay | ✅ Subject: Management |

| ✅ Wordcount: 2912 words | ✅ Published: 21 Dec 2017 |

Introduction

The success of a company is strongly influenced by its ability to identify and implement strategies which will help it in maintaining or enhancing its competitive position. The objective of this essay is two folds: to review the use of environment analysis in generating strategic options, and to measure the performance of a strategy. The business environment is changing rapidly, and companies need to change their strategies to adapt to changes in environment to prosper or just to survive (Wu, 2010). With external environment, and to some extent internal environment, of a firm changing quickly, it is important for a firm to review them when formulating and evaluating strategic options. The BCG matrix, Porter’s generic strategies and the Suitability, Feasibility and Acceptability framework are useful in generating strategies. The application of an environment analysis in generating strategies by using these three strategic management tools is reviewed in this essay.

The success of a strategy in achieving its objectives is also dependent upon the ability of a business to measure its performance so that corrective actions can be taken to improve performance. The two tools analysed in this essay for measuring the performance of a strategy are the benchmarking and the Balanced Scorecard.

Generating strategic options

“A strategy of a corporation forms a comprehensive master plan that states how the corporation will achieve its mission and objectives” (Wheelen and Hunger, 2006, p. 14). Strategies are developed to maintain or enhance the competitive advantage of a firm. According to Saloner et al. (2001), the two main groups of competitive advantage are based on the firm’s position and the firm’s capabilities. The firm’s position reflects its place in an external environment, and the firm’s capabilities corresponds to its internal environment. This implies that external and internal environmental analyses has a vital place in generating strategic options.

An analysis of external and internal environments helps in identifying the strategy that fits the firm most. Porter’s Five Forces and SWOT analysis show the information which can be collected from the external and internal environment analysis to be used for developing a strategy. The tools reviewed in this essay for generating strategic options after conducting an environment analysis are BCG matrix, Porter’s generic strategies and the Suitability, Feasibility and Acceptability framework.

Porter’s Five Forces

The external environment analysis is useful in understanding the factors which are influencing a firm, but are beyond its control. External environment analysis can be done with strategic tools, such as PESTEL (political, economic, social, technological, environmental and legal) and Porter’s Five Forces. The Porter’s Five Forces framework helps in understanding the position of a firm relative to customers, suppliers, competitors, new entrants and substitute products, and these are useful in generating strategic options.

SWOT

The SWOT (strengths, weaknesses, opportunities and threats) analysis is useful to a firm wishing to follow the cost leadership strategy to understand whether it has the desired set of resources to do that. A review of resources and capabilities can show whether the firm has the cost leadership abilities, and which can be maintained in the future. The internal resources of a firm play a significant role in deciding the strategic option that a firm can use to grow its business (Becerra, 2009). The SWOT analysis can also help in identifying the internal weaknesses and external threats which should be factored in deciding which one of the Porter’s generic strategies should be adopted by a firm. The selection of generic strategies would be less effective if the firm does not know whether it has the desired set of resources to defend the strategy. The SWOT analysis is useful in deciding the strategic option to choose by making the best match of the abilities of a company with market opportunities (Spulber, 2004).

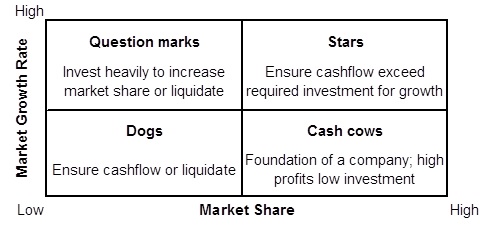

BCG Matrix

The BCG matrix is a useful tool for evaluating the relative performance of markets in which an organisation operates. The BCG matrix analyses each business segment in terms of a company’s market share and market growth (Figure 1) (Grant, 2013). The four categories are Star, Cow, Question mark and Dog. The BCG matrix can be used to identify the markets that the firm should focus on to improve its performance. This is based on the results of the external environment analysis which shows growth and relative positions of competitors in different market segments.

Figure 1: BCG matrix

Porter’s generic strategies

Competitive advantage, and thus higher profits, can be achieved by producing products at lowest cost or establishing a brand in a niche market for which the customer is willing to pay a premium that exceeds the marginal cost of the differentiation. Michael Porter’s three generic strategies – cost leadership, differentiation and focus – are based on a firm’s choice of scope (broad versus narrow market segment) (Grant, 2013). A firm will find it extremely difficult to be a leader simultaneously in all three generic strategies.

A firm can decide whether it wants to operate in niche markets or exit the market altogether by understanding customers’ bargaining power. Understanding the power of suppliers can be used to determine whether a firm can leverage it to become a producer of goods with lowest costs, and thus achieve competitive advantage (Spulber, 2004).

Grant (2013) argues that the industry structure analysis is useful in understanding factors which determine industry profitability, and thus can be utilised in developing strategic options to maintain/increase competitive advantage of the firm. If the external analysis reveals that competition is fierce, it indicates that the cost leadership strategy would be useful as it would allow the firm to compete on price. Whether or not a company is able to adopt the cost leadership position depends upon the results of the internal environment analysis as the firm would require constant efforts to keep its costs lower than those of competitors, which may significantly reduce profit margins. If a firm is unable to compete on the lowest cost strategy, it would have to find a niche market for its products where it can command premium price. Depending on the outcome of review of threats from new entrants, strategies can be developed to create barriers to safeguard competitive advantage of the firm.

Suitability, Feasibility and Acceptability

It is possible that a number of strategic options are possible to achieve the desired objective, which makes it difficult for the management to select the optimal option. The Johnson and Scholes framework of Suitability, Feasibility and Acceptability (SAF) is useful as a selection criteria to select the optimal strategic option (Wu, 2010). When evaluating strategic options, the suitability criterion suggests that the first step should be to determine if the strategic choices are suitable and compatible with within the current and expected external environment (Wu, 2010). One way to do this is to check if the strategic option can help a firm to exploit an opportunity or avoid a threat. The strategy should also be based on strengths of the firm and congruent with its culture (Wu, 2010), as otherwise it would be difficult to implement the strategy. This implies that the external and internal environment analyses are useful in checking the suitability of a strategic option.

Feasibility reviews whether the firm has resources to pursue a strategic option. Feasibility analysis focuses on the evaluation of the internal capabilities of the firm to see if it has adequate resources to follow a strategic option. If the firm does not have the adequate resources, the issue it would face is whether those resources can be acquired externally. If the firm either does not have the resources or it cannot acquire the desired resources from third parties, the corresponding strategic option is not feasible and should be dropped.

Acceptability looks at two other aspects of the strategic options: the financial aspect and the stakeholder aspect (Wu, 2010). The financial aspect focuses on the return to risk profile of each strategic option. In order for a firm to adopt a strategic option, it is important that the choice should increase the wealth of shareholders. The risks of each strategic option should be evaluated using tools such as sensitivity analysis. If potential changes in the external environment can result in substantial negative impact on the firm’s value if it adopts a strategic option, the acceptability of such an option would be low. Though profit generation for shareholders is one of the main objectives of a firm, concerns about the social and environmental impacts of a firm imply that a firm should take into consideration impacts of each strategic option on a wide range of stakeholders. The stakeholder aspect evaluates how each strategic option will affect the stakeholders and their likely reactions. Ignoring potential reactions of a stakeholder can sometimes result in disastrous impacts for a firm. BP has suffered huge losses because of the explosion in the Gulf of Mexico in 2010 (Crooks, 2014). The firm opted for a technology which had lower cost, but it failed to protect an explosion. The cost of cleaning the pollution and reimbursing businesses has cost BP billions. If BP had given more weightage to government as a stakeholder, it may not have suffered the adverse impact of the explosion by rejecting the low-cost, but technically weaker strategic option.

The above review shows that the strategic position of a company is driven by its external environment and internal environment analyses. Strategic options are based on the strategic position analysis (Wu, 2010), which imply that environment analysis helps in generating strategic options.

Measuring performance of a strategy

Successful implementation of a strategy depends upon the ability of a firm to measure its performance so that timely and corrective actions can be taken to achieve the objectives of the strategy. A number of tools for measuring performance of a strategy have been suggested, such as Balanced Scorecard and benchmarking.

Balanced Scorecard

The Balanced Scorecard provides a comprehensive tool to translate a strategy into a set of performance measures (Kaplan and Norton, 1996), because it relies on a number of perspectives to measure performance as opposed to just financial measures in a traditional performance measurement tool. The traditional financial performance measures are restricted in terms of their usefulness to managers by being late and backward looking (Chow and Stede, 2006). This is overcome in the Balanced Scorecard by combining a wide range of performance measures to obtain a comprehensive view of performance of an organisation (Anderson and Fagerhaug, 2002). The Balanced Scorecard combines financial performance measures with other non-financial performance measures that represent the drivers of performance so as to assess the success or failure of a strategy (Anderson and Fagerhaug, 2002).

Kaplan and Norton (1996) suggest four perspectives in a Balanced Scorecard to be Financial, Customer, Internal Business Process and Learning and Growth. These four performance measurement perspectives can evaluate the success or failure of a strategy. Kaplan and Norton (2001) also argue that the four perspectives can be changed/increased to reflect the specifics of each firm.

The Financial perspective in a Balanced Scorecard measures financial performance on the basis of parameters, such as growth in revenue, returns on equity and assets, and profit margins (Jones, 2011). A cost leadership strategy can have financial measures of ratios of sales, general and administrative expenses to revenue. Comparing the pre and post-strategy ratios can show whether the strategy has yielded the desired outcomes.

The Customer perspective analyses the success of a business in terms of customers by using performance measures, such as market share and brand perception (Kaplan and Norton, 1996). The success of a differentiation strategy designed to increase profits of a firm depends on its ability to attract customers. Measuring changes in market share and/or growth in revenue can show whether a strategy has resulted in increase in customer numbers.

The third perspective is Internal Business Process perspective which focuses on internal operating processes important for achieving customer satisfaction (Niven, 2010). Revenue and profits will increase in the medium and long-term if customers are happy with the service and products. The Internal Business Process perspective can measures parameters, such as number of returns, to review the efficiency of operating processes.

The Learning and Growth perspective places emphasis on those aspects of a strategy that result in continuous innovation and growth in a business (Niven, 2010). The strategy of a firm may be to grow business in the long-term by investing in research and development. If only financial measures are used, then the initial lower profits due to research and development expenses will indicate that the strategy has failed. The Learning and Growth perspective can include measures such as the number of patents or new product launches to measure the success of the strategy.

The above-mentioned four perspectives suggest that the Balanced Scorecard is among the best-known strategy scorecards to help firms align with their strategy (Person, 2013). The four performance measure perspectives show that the Balanced Scorecard can be used in measuring comprehensive performance in both short and long-run. Therefore, the Balanced Scorecard is useful in translating a company’s strategy into a set of performance measures.

Benchmarking

Benchmarking is the process of comparing business processes and performance of a firm to industry best practices (Bhandari, 2013). Benchmarking is a comparative method of performance enhancement where a firm finds practices in an area and then tries to bring up its performance in that area (Bhandari, 2013).

Benchmarking is especially useful when analysing the performance of a cost-leadership strategy which relies on the ability of a company to lower costs less than its competitors. Benchmarking can be used to evaluate various aspects of a business in relation to best processes. This can be used to develop a strategy on how to make improvements or adapt best practices, usually with the aim of improving performance.

In addition to comparing performances with other firms in the sectors, a strategy of a business unit may be to compare its performance against units of the same company but located in different places. The internal benchmarking strategy allows easy access to information for comparison (Bhandari, 2013).

Benchmarking can be used to evaluate the performance of a strategy with regards to different aspects of performance, such as financial and operational (Cimasi et al., 2014). This is helpful in analysing the performance of a strategy in terms of both short and long-run objectives of an organisation.

Conclusion

The external and internal environment analyses helps in identifying factors which influence the performance of a firm. The ability of a business to maintain or enhance its competitive position depends upon it success in developing strategies which combine results of external analysis with internal resources and capabilities. Porter’s Five Forces and SWOT analysis are useful in the external and internal environment analyses. BCG matrix uses the external environment analyses to suggest markets in which a firm should focus on. Porter’s generic strategies use both the external and internal environment analyses to identify one of the three strategies – cost leadership, differentiation and focus. While a number of strategies can be generated to achieve corporate objectives, the suitability, feasibility and acceptability of a strategic option should be checked against the results of the external and internal environment analyses.

The Balance Scorecard is one of the performance measurement tools to measure the overall performance of a strategy. The Balanced Scorecard is a comprehensive framework to translate a company’s strategy into a set of performance measures by broadening the performance measurement perspectives. The four perspectives – Financial, Customer, Internal Business, and Learning and Growth – help in measuring the performance of a business in short and long-terms. Benchmarking is also a useful tool for measuring the success of a strategy by comparing the performance – financial and operational – against the best performance in the sector in which the firm operates.

References

Anderson, B. and Fagerhaug, T. (2002). Performance management explained. American Society for Quality.

Becerra, M. (2009). Theory of the firm for strategic management: Economic value analysis. Cambridge: Cambridge University Press.

Bhandari, J. (2013). Strategic management: A conceptual framework. New Delhi: McGraw Hill.

Chow, C.W., and Stede, V.D. (2006). The use and usefulness of nonfinancial performance measures. Management Accounting Quarterly, Vol. 7, Issue 3, pp. 1-8.

Cimasi, R.J., Zigrang, T.A., and Sharamitaro, A.P. (2014). Research and financial benchmarking in the healthcare industry. In: Marcinko, D.E. and Hetico, H.R. (ed.) Financial management strategies for hospitals and healthcare organisations. Boca Raton: CRC Press, pp. 299-318.

Crooks, E. (2014). BP seeks lower penalty for Gulf of Mexico oil spill. [Online] Financial Times, 22 December 2014. Available at: http://www.ft.com/cms/s/0/1df61b62-89b8-11e4-9dbf-00144feabdc0.html#axzz3bbvCC5eq

Grant, R.M. (2013). Contemporary strategy analysis. 8th edn, Chichester: John Wiley & Sons.

Jones, P. (2011). Strategy mapping for learning organisations: building agility into your Balanced Scorecard. Farnham: Gower Publishing Limited.

Kaplan, R.S., and Norton, D.P. (1996). The Balanced Scorecard. Boston: President and Fellows of Harvard College.

Kaplan, R.S., and Norton, D.P. (2001). Transforming the balanced scorecard from performance measurement to strategic management: Part I. Accounting Horizons, Vol. 15, Issue 1, pp. 87-104.

Niven, P.R. (2010). Balanced Scorecard step-by-step: Maximising performance and maintaining results. 2nd edn, Hoboken: John Wiley & Sons.

Person, R. (2013). Balanced Scorecards & operational dashboards with Microsoft Excel. 2nd edn, Indianapolis: John Wiley & Sons.

Saloner, G., Shepard, A., and Podolny, J. (2001). Strategic management. Danvers: John Wiley & Sons.

Spulber, D.F. (2004). Management strategy. New York: The McGraw-Hill Companies.

Wheelen, T.L., and Hunger, J.D. (2006). Concepts in strategic management and business policy. 10th edn, Upper Saddle Trust: Pearson Education.

Wu, T. (2010). Strategic choice – Johnson and Scholes suitability, feasibility and acceptability model. [Online] Available at: http://www.tolobranca.nl/Bestanden/SFA%20Matrix%20learning_strategic_choice.pdf

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this essay and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal