Porter’s 5 Forces Analysis Guide

Info: 1958 words (8 pages) Marketing Guides

Published: 04 Feb 2021

Studying business, marketing, or strategic management? If you need help with an assignment using Porter’s Five Forces analysis, get in touch with our experts today. Check out our Business assignment help page for more information.

One of the most critical aspects of successful business management is the capability to analyse the environment. Developments in firms’ internal (e.g. industry level) and external (macro) environment notably shape strategic feasibility business leaders need to continually monitor to effectively organise the factors of production and to allocate resources to the most efficient use to generate value for stakeholders (Nieuwenhuizen and Badenhorst, 2016).

What is Porter’s Five Forces Analysis?

The five forces framework is a common strategic planning model focusing on the actual level of competition in a particular industry. The determinants thereof to direct managers on adjusting corporate tactics (that may as well include the complete withdrawal from a particular sector) to maximise revenue and to minimise competitive pressures (Porter, 1979).

This free Porter’s 5 Forces guide focuses on the practical applicability of Porter’s (1979) model by examining each force, and how they come together to perform as an effective business analysis tool. Each aspect of the Porter’s 5 Forces model will be explored in detail, with an explanation of how each aspect should be considered, along with some helpful examples. Our introduction to Porter’s 5 Forces is perfect for helping you to gain a better understanding of this analysis technique, as well as guiding students towards effectively implementing the Porter’s 5 Forces model.

Implementing a Porter’s Five Forces Analysis

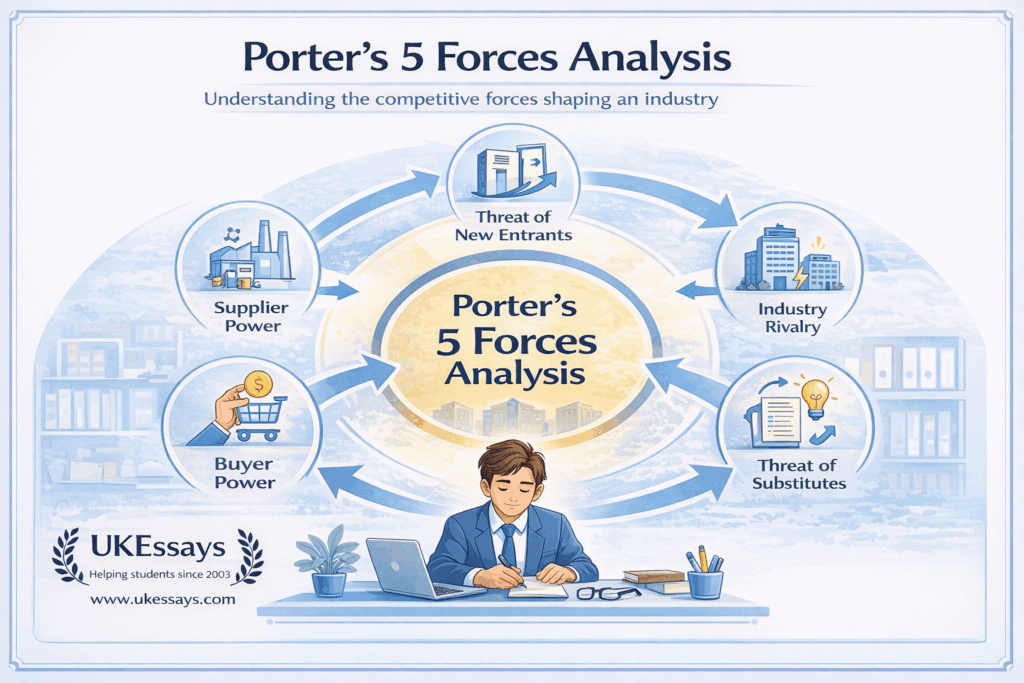

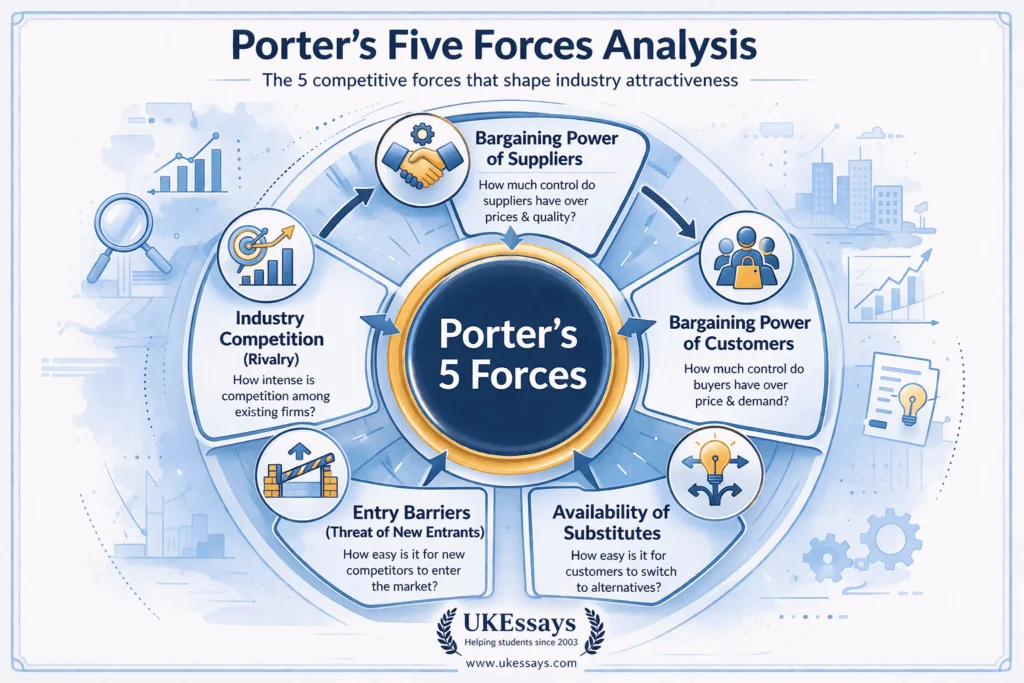

Just in case of any industry analysis, it is first indispensable to possess an in-depth understanding of the market dynamics and structure to draw relevant conclusions from Porter’s model (1979), consisting of five elements (i.e. forces) that shape industry competitiveness. These include:

- Bargaining power of suppliers (providing the input for production)

- Bargaining power of customers (the end-users of the product)

- Availability of substitute products/services (any comparable product/service with similar characteristics serving as an alternative)

- Entry barriers (the ease of entering a new market)

- Resultant level of industry competition (also referred to as internal rivalry)

(Porter, 2017).

Once these forces are thoroughly understood in a particular industry context, appropriate responses and plans to address competition and to reduce firms’ vulnerability to rivals’ strategy can be formulated.

1. Bargaining Power of Suppliers

Most organisations do not produce all raw materials and components internally either due to the lack of expertise or the lack of economic feasibility of producing generic components in-house, hence it is worthwhile to look at supplier relationships as well when performing an industry analysis (Palepu, 2009). For example, car manufacturers tend to outsource non-key activities to suppliers with accumulated technical expertise in one particular field of automotive technology –such as windshields and tyres to take advantage of specialised firms’ technological supremacy as well as cost advantage due to economies of scale and scope (McIvor, 2005).

By Porter’s (1979) definition, there are several factors determining suppliers’ bargaining power: switching costs, the availability of suppliers, the number of suppliers (relative to buyers), suppliers’ relationship-specific investments to support a particular transaction, buyers’ dependence on suppliers and the possibility of suppliers’ forward integration. Just as in the case of the previous forces, the higher power suppliers possess, the lower the attractiveness and the consequent profitability of the industry (Porter, 1979).

Most organisations tend to carefully negotiate supplier relationships to mitigate this force by selectively outsourcing only non-critical components that may be procured from elsewhere (e.g. car tyres or other modules with minimum asset specificity) should suppliers decide to alter agreements at the detriment of the buyers (Marin and Schnitzer, 2002). A high supplier power may push organisations to vertically integrate operations to control more stages of the supply chain as the means to eliminate opportunistic supplier behaviour and to improve overall profitability.

2. Bargaining Power of Customers

The bargaining power of customers element shares many similar characteristics with the previous force discussed (suppliers), although there are some key differences worth discussing to assess industry competitiveness. Customers are usually positioned at the very end of the supply chain and thus constitute the market of output (Porter, 2008). The number of customers/the market size served is one of the primary determinants of buyer power: if there are only a few buyers to several suppliers, customers are known to possess a dominant bargaining position. Further to this, the size of actual orders (relative to suppliers’ designed capacity) is another key variable determining the relative strength of this force.

If a buyer orders in high quantity, the opportunity cost of not adhering to the buyer’s request (e.g. price reduction or quality changes) can be sufficiently high to enable the buyer to bargain favourable terms and conditions, especially in the presence of many close, cheap, and qualitatively comparable substitutes with minimal switching costs for the buyer (Palepu, 2009). In the age of information, buyers’ option to compare and contrast different products/services benefits customers and limits sellers’ options to mitigate competition (Spread, 2018), though product differentiation and cost leadership strategies may offer some temporary relief for sellers from competitive pressures in the short-term (Porter, 2008).

3. Threat of Substitution

In the very beginning of products’ and/or services life cycle, competitive pressures are relatively weak, and as rivals may be incapable of imitating innovative products (either due to strategic or structural barriers), firms’ exposure to competitive threats is temporarily limited (Naga, 2012). However, as industries mature, more and more substitute products and services emerge that may compromise incumbents’ market share as well as profitability. Although substitutability can be a highly subjective factor, there are a few general criteria to identify the actual strength of this force in a particular market being analysed (Porter, 1979).

In principle, a substitute product/service should offer similar benefits to users, implying that (assuming perfect substitution) customers do not experience any decline in perceived value after switching to a comparable product/service. This also necessitates low switching costs, identical (if not lower) retail price for substitute products/services and comparable functional and qualitative attributes (Naga, 2012). For instance, in the budget small car category, multiple models compete for customers, and since list prices and product characteristics tend to be similar, the threat of substitution in the market for budget cars can be concluded as severe. In contrast, if product characteristics are difficult to imitate (e.g. Tesla cars’ range), the threat of substitution is weak (although this may only be temporary).

4. The threat of New Entrants

Highly profitable industries with remarkable growth opportunities always attract new entrants to generate profit and to satisfy shareholder demands (Porter, 2008). However, merely designating an industry as lucrative does not, under all circumstances, warrant an immediate success after entering a new industry unless other factors in Porter’s (1979) model are methodically examined. Entry barriers can be categorised as either structural and strategic (Geroski, Gilbert and Jacquemin, 2001) – if any of these is remarkably present, it is reasonable to conclude that entry threats are not substantial in a given industry.

Principally, structural barriers are the strongest deterrents which progressively develop over time without significant incumbent efforts to protect market share. Structural barriers generally incorporate such factors as the total cost of entry (including investments in machinery and technology, the cost of advertising to attract clients and a threshold capacity level to attain economies of scale and scope to imitate incumbents’ cost advantage) and control over critical resources (e.g. airlines holding capacity slots at busy airports). These barriers should be carefully analysed before assessing an industry’s potential for entry to avoid costly marketing failures (Geroski, Gilbert and Jacquemin, 2001).

On another note, strategic (or artificial) barriers involve deliberate efforts on behalf of incumbent firms to ‘lock-in’ customers and to increase new rivals’ cost of market entry (Porter, 2008) – these options comprise of branding, patents and other forms of legal protection that may limit new entrants’ access to the factors of production (e.g. proprietary technology). A less common but otherwise highly effective method of increasing strategic entry barriers includes vertical integration to control a substantial fraction of supply chains to limit rivals’ access to crucial resources (George, Joll and Lynk, 1992).

5. Internal Rivalry

The last force is jointly influenced by the strengths of the above forces and determines the industry’s overall attractiveness and profitability (Porter, 1979). Rivalry is expected to be substantial if there are several vendors of similar size selling comparable products to brand-neutral customers in a market that is no longer capable of exhibiting growth tendencies (i.e. markets in the maturity or the decline stage). In addition, the size of market entry investments influences the barriers to exit: on the condition that incumbents have a substantial amount of capital tied up in non-transferable assets (e.g. machinery), intensified competition is expected beyond the growth stages (Besanko, 2010).

Substantial exit barriers amplify competition, although it shall be added that the presence of exit barriers may provide valuable acquisition opportunities for successful firms to enhance competitiveness and to reduce rivalry (Besanko, 2010). On the bottom line, an intensive rivalry moderates profitability for all incumbent firms: intensive advertising campaigns and price wars are standard features in competitive markets and whilst these ultimately benefit buyers, a severe rivalry is a major impediment to profitable operations (Porter, 2008).

Potential Limitations

Porter’s five forces framework is arguably one of the most widely cited models to conduct a comprehensive industry analysis, yet there are certain limitations and shortcomings worth taking into account when solely using this model to examine industry dynamics (Kew and Stredwick, 2008). First, the model describes industries ‘as is’; thus, the long-term applicability of the model is dubious. Second to this, the model does not fully incorporate the role of regulators/governments shaping the competitiveness and profitability of any given industry. Third, the model falsely assumes stable market conditions and that firms solely operate in one industry, whereas, in reality, none of these accurately portray the business landscape in the 21st century.

For further reading, two strong follow-on topics are PESTEL Analysis Guide and SWOT Analysis Guide. They work well alongside a Porter’s Five Forces article because PESTEL helps readers widen the lens from industry competition to the broader political, economic, social, technological, legal and environmental pressures shaping a market, while SWOT brings the focus back to the business itself by assessing strengths, weaknesses, opportunities and threats in a more rounded strategic view

Studying business, marketing, or strategic management? If you need help with an assignment using Porter’s Five Forces analysis, get in touch with our experts today. Check out our Business assignment help page for more information.

For those that like to that like to have these theories explained this is an in-depth video exampling the topic further.

References

- Besanko, D. (2010). Economics of strategy. Hoboken, NJ: John Wiley & Sons.

- George, K., Joll, C. and Lynk, E. (1992). Industrial organisation. London: Routledge.

- Geroski, P., Gilbert, R. and Jacquemin, A. (2001). Barriers to entry and strategic competition. London: Routledge.

- Kew, J. and Stredwick, J. (2008). Business Environment: Managing in a Strategic Context. United States: Kogan Page Publishers.

- Marin, D. and Schnitzer, M. (2002). Contracts in trade and transition. Cambridge, Mass.: MIT Press.

- McIvor, R. (2005). The Outsourcing Process: Strategies for Evaluation and Management. United States: Cambridge University Press.

- Naga, A. (2012). Strategic Management. United States: Vikas Publishing House.

- Nieuwenhuizen, C. and Badenhorst, J. (2016). Business management for entrepreneurs. United States: Juta and Company Ltd.

- Palepu, K. (2009). Business analysis and valuation. London: South-Western Cengage Learning.

- Porter, M. (1979). How Competitive Forces Shape Strategy. Harvard Business Review, 57(2), pp.137-145.

- Porter, M. (2008). On Competition. United States: Harvard Business Press.

- Porter, M. (2017). Competitive Strategy: Techniques for Analyzing Industries and Competitors. CreateSpace Independent Publishing Platform: United States. Spread, P. (2018). Economics for an information age. New York: Routledge

Cite This Work

To export a reference to this article please select a referencing stye below: