Fiscal Dominance and Monetary Dominance

| ✓ Paper Type: Free Assignment | ✓ Study Level: University / Undergraduate |

| ✓ Wordcount: 1829 words | ✓ Published: 12 Oct 2017 |

Fiscal Dominance and Monetary Dominance and Policy Instruments Used by the Bank of England for Inflation Targeting

1. Introduction.

The government often employs fiscal policy, monetary policy or a combination of both to sway the economy back to an equilibrium position. The manner in which the government employs both policies may result to either fiscal or monetary dominance. This paper is aimed at defining fiscal and monetary dominance so as to employ the distinction between the two policies to determine whether the Bank of England has enough policy instruments to control inflation. To achieve this objective, the IS/LM model will be employed to see how various policy measures affect the interest rate, national income and inflation rates[1]. We begin by defining fiscal policy, monetary policy, fiscal dominance and monetary dominance in section 2 below. The study later provides a description of the IS/LM model in section 3 and finally, an evaluation of the instruments used by the bank of England in controlling inflation is done in section 4.

2. Fiscal Policy, Monetary Policy, Fiscal Dominance and Monetary Dominance

2.1. Fiscal Policy

Fiscal policy refers to a situation whereby the government restores equilibrium in the economy by making changes to taxes or government expenditure on public goods and services[2]. When there is under-utilisation of capacity, the government can increase capacity utilisation by reducing taxes (that is through a reduction in tax rates or tax base) or by increasing spending on public goods and services as well as subsidising the production of certain goods and services[3]. Fiscal policy aimed at increasing money supply is referred to as easy fiscal policy[4]. On the other hand, when there is over-utilisation of capacity, the government either increases taxes (through and increase in tax rates or tax bases) or reduces spending on public goods and services[5]. It also reduces subsidies and transfer payments. This type of fiscal policy is referred to as tight fiscal policy[6].

2.2 Monetary Policy

Monetary policy is referred to as a means by which the central bank tries to sway the economy to equilibrium by influencing the supply of money[7]. This is achieved through four main approaches, which include: printing more money; direct controls over money held by the money sector; open market operations and influencing the interest rate. Both tight and easy monetary policies can also be identified. Like easy fiscal policy, easy monetary policy is one whereby the central bank embarks on a policy to increase the supply of money. On the other hand tight monetary policy is a policy whereby the central bank embarks on a policy to limit the circulation of money such as increasing interest rates.

2.3 Fiscal Dominance

Fiscal dominance occurs when government can determine the stock of debt, and the path of total expenditures and taxation[8]. Under these conditions, the government can influence the inflation rate, the future flow of monetary base by raising the permanent level of expenditures without at the same time raising taxes[9]. Fiscal dominance is therefore a scenario whereby monetary policy is driven by fiscal policy[10].

2.4 Monetary Dominance

Monetary dominance refers to a situation whereby fiscal policy is influenced by monetary policy[11]. Liviatan[12] states, that: “the benchmark definition of monetary dominance is that the fiscal policy has to accommodate any monetary policy”. This implies that fiscal policy must ensure that the liquidity of the government is maintained for any monetary policy[13].

3. The IS/LM Model

The IS/LM model is made up of two curves, the IS curve and the LM curve[14]. The IS curve, which represents the equilibrium conditions of the real (investment-savings equilibrium) side of the economy[15]. For an open economy, the IS curve can be represented by the following equation[16]:

(1)

(1)

Where

Y= national income,

Z= private expenditure (consumption and investment),

i = interest rate,

T= taxes,

G= government spending,

Ex = exports (receipts on the current account of balance of payments),

e= exchange rate,

Im = imports (payments on the current account of balance of payments).

The LM curve is influenced by balance of payments, because differences in imports and exports affect the money supply:

Md = Ms

Md = Md(Y,i)

Ms = m.C

Where Md = money demand,

Ms = money supply,

M = money multiplier,

C = volume of base money.

The central bank creates base money by granting domestic credit as well as through open market operations such as the purchase of foreign exchange.

Following from Visser[17], the base money supply at any point in time should be equal to the base money supply one period behind plus the change in the domestic credit supply D during that period and the change in the foreign-exchange reserves V. This change is equal to the balance-of-payments balance X of the non-financial sector[18].

C = C-1 + ∆D + ∆V

∆V = X

The central bank uses open-market operations through the sales and purchase of domestic debt instruments such as bonds and other debt issues as the instrument of monetary policy. The volume of this purchase can be denoted by H = ∆D.

Following from above C = C-1 + X+H

Ms = m(C-1 +X+H)

This gives us the equation for the LM curve as follows[19]:

Md (Y, i) = m(C-1+ X+ H)(2)

Equating the real side of the economy (equation (1)) to the monetary side (equation (2)) leads to the IS/LM model.

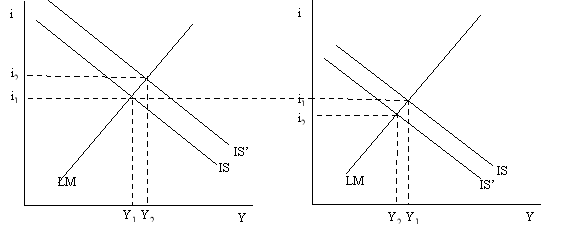

Figure 1. Fiscal Policy

a). Easy fiscal policy b). Tight fiscal policy

At equilibrium, the equation for the IS curve is equal to that for the LM curve, that is the real side of the economy is equal to the monetary side of the economy and it is at this point that the LM curve cuts the IS curve[20]. It should be noted that the IS curve has a negative slope, while the LM curve has a positive slope. Figure 1 above represents the initial equilibrium position of the IS/LM model. The equilibrium national income is given by Y1; the equilibrium interest rate is i1. Lets assume that the government embarks on an easy fiscal policy and reduces taxes T, this will result in a shift in the IS curve to the right from IS to IS’, establishing a new equilibrium point between the IS’ curve and the LM curve at a higher level of national income Y2 and at a higher rate of interest i2. This is shown in the figure 1a above. Conversely if the government decides to embark on a tight fiscal policy by say increasing tax rates or the tax base so as to increase the overall tax liability, this will lead to a decrease in the national income from Y1 to Y2 and as well as a decrease in the interest rate from i1 to i2, resulting in a leftward shift in the IS curve from IS to IS’. This establishes a new equilibrium position to the left. This effect is shown in figure 1b above.

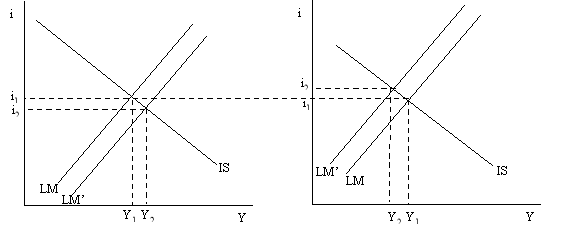

Figure 2 Monetary Policy.

Figure 2 Monetary Policy.

a). Easy monetary policy b). Tight monetary policy

In the IS/LM model above, the intersection of LM and IS represent the equilibrium state of the economy. At this point, the national income is given by Y1, and the interest rate by i1. In the first case lets assume that the central bank embarks on an easy monetary policy by purchasing debt securities in the open market. This will lead to an increase in the supply of money and thus the national income. The LM curve will shift to the right creating a new equilibrium position at a higher national income Y2 and a lower interest rate i2. This is represented in figure 2a above. On the other hand, if instead the central bank decides to embark on a tight monetary policy by raising interest rates from i1 to i2, it will result to a decrease in the national income from Y1 to Y2 and a shift in the LM curve from LM to LM’. This is represented in figure 2b above.

4. Bank of England and Inflation Targeting

The main instrument employed by the bank of England in fighting inflation is the interest rate. For example, the bank has raised interests rates 5 times since the beginning of the year 2007[21]. The last increase in interest rates was on 5th July 2007, which saw an increase in the interest rate from 5.5% to 5.75%[22]. Inflation in the UK is currently running at 2.5% and the bank of England is targeting 2% in the course of the year[23]. The bank is also worried that mortgage costs were also part of the official inflation target because they represent the biggest expenses for many households but despite this, mortgage costs are not included in the consumer price index (CPI). According to Clarke[24] from the BBC World Service, the Governor of the bank Mervyn King explained that the omission of mortgage costs from the CPI is “controversial” making it difficult for the bank to meet its objective of reducing inflation to its target level. From the foregoing, one can conclude that the Bank of England’s main policy instrument is the interest rate. It rarely employs policies such as open-market operations and direct control over the money held by the non-financial sector. It therefore has limited instruments in targeting inflation. This is also an indication of monetary dominance whereby any fiscal policy must accommodate any monetary policy, which in this case is an influence on the interest rate.

BIBLIOGRAPHY

Black J. (2002). Easy fiscal policy.A Dictionary of Economics.. Oxford University Press, 2002. Oxford Reference Online.

Blackden R. (2007). Bank of England set to raise interest rates. Telegraph.co.uk. 1:48am BST05/07/2007. Retrieved from:

http://www.telegraph.co.uk/money/main.jhtml?xml=/money/2007/07/04/bcnrates104.xml

Clarke J. (2007). The Governor of the Bank of England, Mervyn King, has told the BBC he wishes mortgage costs were part of the official inflation target. BBC Radio 4’s Money Box. Retrieved from:

http://news.bbc.co.uk/1/hi/programmes/inside_money/6906592.stm

Fratianni M., Spinelli F. (2001). Fiscal Dominance and Money Growth in Italy: The Long Record. Explorations in Economic History, vol. 38, pp 252-272.

Kennedy S. (2007). Bank of England raises key rate to 5.75% U.K. rates hit six-year high; further hike may be in the cards. Marketwatch.com news 10:06 AM ET Jul 5 2007. Retrieved from:

Liviatan N. (2003). Fiscal Dominance and Monetary Dominance in the Israeli Monetary Experience. Bank of Israel Research Department Discussion Paper No. 2003.17

Sabaté M., Gadea M. D., Escario R. (2006) Does fiscal policy influence monetary policy? The case of Spain, 1874–1935. Explorations in Economic History, vol. 43, pp, 309–331

Smullen J., Hand N. (2005). Monetary Policy. A Dictionary of Finance and Banking. Oxford University Press. Oxford Reference Online.

Visser, H. (2004). A Guide to International Monetary Economics : Exchange Rate Theories, Systems and Policies 3rd Ed. Cheltenham, UK, Northhampton, MA Edward Elgar Publishing, Inc.

1

Footnotes

[1] Visser (2004: p. 40).

[2] Smullen and Hand (2005)

[3] Smullen and Hand (2005); Visser (2004: p. 43)

[4] Smullen and Hand (2005)

[5] Black (2002)

[6] Ibid.

[7] Ibid

[8] Frantiani and Spinelli (2001: p. 255).

[9] Ibid

[10] Sabate´ et al. (2006: p. 319)

[11] Liviatan (2003: p. 1)

[12] Ibid

[13] Ibid

[14] Visser (2004: p. 40).

[15] Ibid (p. 41)

[16] Ibid (p. 41)

[17] Visser (2004: p. 42)

[18] Ibid (p. 42)

[19] Ibid (p. 42)

[20] Visser (2004: p. 42)

[21] Kennedy (2007); Blackden (2007).

[22] Ibid

[23] Ibid

[24] Clarke (2007)

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

DMCA / Removal Request

If you are the original writer of this assignment and no longer wish to have your work published on UKEssays.com then please click the following link to email our support team:

Request essay removal