An Analysis of Impact of Bonus Issue Announcement on Share Price

Info: 8202 words (33 pages) Dissertation

Published: 11th Dec 2019

AN ANALYSIS OF IMPACT OF BONUS ISSUE ANNOUNCEMENT ON SHARE PRICE

Abstract

The proposed study aims to find the impact of bonus issue announcement on share price. For this purpose data pertaining to bonus issue announcements of NIFTY 50 stocks in last 10 years is taken into consideration. Event study has been used to calculate abnormal returns, average abnormal returns, cumulative abnormal returns, t-tests and correlation. Paired sample t-test has been employed to check whether there is a significant difference before and after bonus issue announcement on share price. Analysis is carried out on the sample as a whole, the IT industry and Refineries industry limited to the NIFTY 50 Index. The study has been conducted for a 10 year period, from 2008 to 1st September, 2017. Results reveal there is a significant difference before and after in share price for sample as a whole and the IT industry.

Introduction

Bonus share is a free share distributed by a company to its existing shareholders based on the proportion of shares held by them. This practice of issuing bonus shares is a tool used by companies to retain their shareholders for a longer duration. Issue of bonus shares increases total number of outstanding shares of the company and the value of ownership of shareholders while value of the company does not get affected. Hence, value of the company remains unaltered even after resorting to bonus issue. However, bonus issue of a company may have an announcement effect on its share price. Shareholders, who are the real owners of a company, should be aware of the impact which might be exerted by bonus announcements on share prices and market movements. In addition, bonus announcements also influences investor’s decision whether to dispose their shares or hold them back. This study has been conducted to assess the impact of bonus announcement on share prices.

Literature Review

Mr. Fakru Khan.Y and Mr. Thoufiqulla conducted a research in 2013 to analyze the impact of bonus share issue on Share price with Reference to NSE Listed Stocks in India with a view to better understand the movement in stock price one day before the bonus issue allotment date and the movement in stock price one day after the bonus issue allotment date. The sample consisted of 12 companies listed on NSE in different sectors and the period of study was from December 2012 to November 2013 by using random sampling method and the statistical tool used is Paired T-test to arrive the result. The study found that 9 out of 12 companies had a negative difference in share price one day after bonus issue allotment and one day before bonus issue allotment, while only 1 company was neutral i.e. price remained unchanged and the other 2 showed a positive impact (share price went up). In general, the study defers that bonus issue is a powerful financial event that made the market spiral into a negative effect which in turn made the investors to be cautious before investing in it.

Mr. Prashant Poddar conducted a research in 2013 to assess the Impact of Bonus Issues on Share Prices with reference to BSE Listed Stocks in India and the significant difference in impact on financial vs non-financial sector. The study was conducted between January 2008 to December 2012 with the help of Average Abnormal Return (AAR), Cumulative Average Abnormal Return (CAAR) and a series of paired sample T-tests. The sample consisted of 40 companies from 24 different sectors listed on BSE, which were further divided into financial and non-financial sector. The study found that there is a significant difference between the shares prices before and after the bonus issue announcement which could be because of informational leakages and the sentiment in the market is that bonus shares will increase the stock of shares in the market which dilutes equity and unchanged profits make investors cautious thus bringing down the share price. Fall in share price is not always bad news, usually fall in CAARs and share price in short term is a pattern of price correction. The study further found that there is a significant difference in impact of bonus issue on share price on the financial sector vs non-financial sector due to the difference in CAARs post the bonus issue announcement. The market shows a negative trend in share price post bonus issue announcement.

Mr. Denis Oliech Ayoma conducted a research in 2012 to analyze the Impact of Bonus Issue on Share Price of Companies quoted in Nairobi Securities Exchange. The study comprised of a sample of 14 companies who had bonus issues between the years 2009 to 2012. Mr. Ayoma used t-test statistic to test the significance of the average abnormal returns and cumulative average abnormal returns from zero. The study made use of daily adjusted prices for sample stocks for the event window of 29 days consisting of 14 days before and 15 days after the event date. The study revealed that the market overreacts in anticipation of the bonus announcement but corrects itself after a formal bonus issue announcement. T-tests identified the p value as 0.275, from this we can defer that it is possible to make profits or abnormal returns from bonus issue announcement as the stock prices do not assimilate such information instantly but do so in a lagged manner.

Ms. Sharmila R, Mr. Nanjundaraj Prem Anand, and Mr. Thiyagarajan. R conducted a research study in 2014 to understand the Volatility of Stock prices around Bonus share Announcements. The study aims to analyze the market reaction to bonus share announcements in the Indian Stock Market of CNX 500 stocks for the period of 2013 to 2014 using event study methodology. The sample consists of 18 stocks that have announced bonus issue in the time frame. The AAR on -15 day is found to be positive and significant which shows the leakage of information before the event. The CAAR is found to be positive from -15 day to +7 days supporting the signaling hypothesis of bonus share announcements. The negative CAAR from +8 to +30 days supports the trading range hypothesis. The significant negative returns of AAR and trend of CAAR in the post announcement period shows the stock price adjustment to bonus issues which supports the trading range hypothesis and liquidity hypothesis.

Mr. Rajesh Khurana and Dr. D. P. Warne conducted a research study to analyse the Market behavior around the Bonus Announcement Date. The goal of this study is to test the semi-strong form of market efficiency by studying the reaction of stock prices to bonus issue announcements of stocks related to NSE 100.

For analyzing the reaction during bonus issue announcement, they chose 34 companies from 11 different sectors in the time period from 2006 to 2012. It was found that on an average the stocks start demonstrating positive abnormal returns from the day t-ninth day. On the day of bonus announcement there is negative AAR of -0.01% which is very low at 1% level (z value = 3.84). The AAR for the day t-1, t0, t+1, t+2 shows insignificant negative returns. Overall the behavior of AARs and CAARs is found to be in sync with expectation, therefore supporting the hypotheses that the Indian Stock market is Semi Strong Efficient.

Prof. Suresha B and Dr. Gajendra Naidu conducted a research study in September 2012 to assess the Effect of Bonus announcement on Share Price Volatility and Liquidity and its Impact on Market Wealth Creation of informed investors in Bangalore, with special reference to CNX NIFTY stocks of NSE. To test these objectives, the companies in the last 15 years, that went for bonus issue had been taken from a sample frame of current constituents of CNX Nifty.

The event study methodology was used to determine the effects of bonus issue. Abnormal returns were computed using the market model and t-tests were conducted to test the significance. The study depicted that the bonus issue announcement has a positive average abnormal return of 0.620% on the day of bonus announcement and it is significant at 5% level with t value of 2.545. Hence, in conclusion the bonus issue announcement creates positive wealth effect with higher liquidity.

Dr. Satyajit Dhar and Ms. Sweta Chhaochharia, conducted a research study in January 2008, to analyze Indian Stock Market Reaction around Stock Splits and Bonus Issue. Event study methodologies were used, Capital Asset Pricing Model was used to calculate abnormal returns and significance was calculated using t tests. The sample consisted of 90 stock splits and 82 bonus issues announced by companies listed on the BSE 500 index, in the sample time frame of April 1, 2001 to 31st March 2007. In respect of bonus issues, the study found a positive AAR of 1.8% which is relatively high and very significant at 0.01% level. In the case of stock split, the AAR is of 0.8% which is also very positive and highly significant at 0.01% level. Therefore, overall the pattern of CAAR is found to be in conformity with expectations, therefore lending support to the hypothesis that Indian stock market is efficient in semi strong form.

Subhendu Kumar Pradhan and Dr. R Kasilingam conducted a research to assess the Impact of Bonus Announcements on Share Price. The sample for the study consisted of ten companies listed in S&P BSE 500 index, for a seven year period, sample time frame being 1st January 2005 to 31st December 2012. The abnormal returns and cumulative abnormal returns of the companies were calculated using the event study methodology. Paired sample T-test had been employed to compare share prices prior to and post bonus announcements. Six of the ten companies had positive cumulative abnormal returns while the other four had negative cumulative abnormal returns during short run as well as long run. Paired sample t-test indicated that bonus announcement exerted an impact on share price. Correlation analysis showed that share price changes majorly due to the bonus announcement effect as change in share price is irrelevant to market movements. Overall, the company analysis showed that abnormal return is positive prior to bonus announcement and negative immediately after announcement. In conclusion, it can be said that market reacts to bonus announcement positively ahead of the announcement and negatively after the announcement.

In 2014, Mr.Kamanja Kawira conducted a research on the Effect of Bonus Issue Announcements on Share Price of Commercial Banks listed at the Nairobi Securities Exchange. The research aimed at studying the impact on the performance of the share price for the period of three months prior and three subsequent of the bonus issue. The study involved a sample of 8 stocks listed on the NSE (Nairobi Stock Exchange) using the 2 tailed t-test .It was analyzed that there was a critical negative reception one month prior to the bonus declaration signaling the panic and the vulnerability regarding such news. This continues till the period of three months after the bonus issue until then the reception was found to be positive. This suggested that within this period shareholder had adjusted themselves and accepted the issue. The results indicated that the Kenyan markets are efficient and any deterioration in the share price dude to the bonus issue would be recovered in the following months.

Mr. M.Muthukmu and Dr.S Rajamohohan in 2014 analyzed the Stock Price Reaction to Bonus Issue from an Indian Equity Market Perspective. For the purpose of the research the only the 30 stocks comprising of the Nifty index which had issued a bonus were selected. The daily closing prices of the selected scripts for a period of 30 days prior and post the issue were taken. Wilcoxon matched pairs method a non-parametric test was used as a tool for analysis. The study found out that 26 stocks out of the 30 selected stocks had an impact on their share price due to the bonus issue. Out of which 20 stocks reacted positively to the bonus issue while the remaining 6 had a negative reaction. One of other findings of the research were the correlation between the size of the bonus issue and the price impact of shares. The shares which had a higher bonus payout ratio received a good response from the investors and vice versa. This analysis proved that the Indian Share markets has similar behavior to Global Equity markets with respect to issue of bonus shares.

Mr.Dhanya Alex in 2017, Analyzed the Market Reaction around the Bonus Issues in Indian Market. The sample size included 57 companies which issued a bonus in 2015 using the t-tailed test on the Average Abnormal Returns (AAR) and cumulative abnormal returns (CAR).

An event window of 20 days was taken for estimating the expected return i.e. 0 being the event date and 20 days prior and post to the event date the returns were estimated. The AAR was found to be 1.8% for bonus issues and 0.8% for stock splits. It was found through the study that the sample companies had the highest AAR on the 5th post day of the event date but it was not statistically significant. It was further found that the highest abnormal returns were highest on the day of the bonus an announcement but even this was statistically insignificant. The study concluded that the Indian markets are efficient based on the analysis of the cumulative abnormal returns.

In 2014, Mr.Nishanthini A and Mr. Nimalasthasan B conducted a study on the Market Efficiency and its Impact on Share Price with respected listed Manufacturing Companies in Sri Lanka. For the purpose of the study 10 companies were selected out of the 36 listed at the Colombo Stock Exchange for a period of 5 years. The Standard Event Study Method was the tool used to derive the abnormal and the average abnormal returns. The impact was studied upon with the event window of 21 days post and pre announcement. The study showed that the dividend announcement did not surprise the investors and markets react later than the dividend announcements. The finding were not statistically significant as it was found out that the AAR was 2.9 percent on dividend date but t value less than 1.96. It was also concluded that the investing community reacts before the 2nd day after from the date of dividend announcement.

Ms.Madhuri Malhotra,Dr. M.Thenmozhi and Dr. G. Arun Kumar conducted a research in the year 2007 to study the reaction and the changes in the share prices to the announcement of bonus shares. For this purpose, they identified the bonus issues made by the chemical firms listed on the Bombay Stock Exchange, for a period of 5 years(January 2001-January 2006). The total portfolio consisted of 24 bonus issue announcements. The standard event study methodology was used for this purpose. The impact was studied around the announcement date for a window of 11,21 and 41 days. The study shows that, on an average, bonus share announcements raise negative CARs(Cumulative abnormal returns) around the announcement date. Also, positive CARs in the intervals of dates -20 to -1 before the announcement imply that the market had sensed it beforehand. The analysis shows that the bonus issues have a signaling effect but the effect is inversely related to stock price changes.

A. F. M. Mainul Ahsan, Muhammad Ashadur Rahman Chowdhury & Ahasan Habib Sarkar conducted a research in the year 2003 to study the reaction of the stock prices to the announcement of bonus shares in Bangladesh. For this purpose, the right issues of firms of 6 different sectors,namely Engineering, Textile, Pharmaceuticals & Chemicals, Fuel & Power, Cement and Food & Allied for the period of 2009-2012 were studied. The right issues were a total of 136 in number and the standard event study method was used. All these issues were of the firms listed on the Dhaka Stock Exchange. After a study of the ARRs(Average abnormal returns), it was deduced that the Food & Allied sector and the Textile sector had the highest(0.16%) and the lowest(-0.10%) ARRs respectively. The ARR for the entire sample is 0.02%. However, the severe market crash of Bangladesh in 2010 dented the market returns. It was hence concluded that the significant rise in the prices before and after the announcement date show a signaling effect and implies that the market had sensed it in advance. Sector Wise, there is a positive market reaction to the bonus shares announcement of Fuel & Power, Food & Allied, Cement and Pharmaceuticals & Chemicals sector and a negative market reaction to Engineering and Textile sector.

Ms. Geetika under the guidance of Ms.Ruchika Wadhwa conducted a study of the effect of stock split and bonus announcements on the share price and liquidity of the stock market. For this purpose, companies that issued bonus shares and went for stock splits from January 2007 to December 2011 and are listed on the National Stock Exchange(NSE) have been sampled. A total of 125 companies were taken,25 for each year. Event study methodology has been used and an event window of 61 days has been taken. As per the findings of the study, the CAAR for stock split is positive 3.71% and also there is a significant variation in the ARR before and after the stock split. As far as the bonus issues are concerned, the CAAR is positive 8.24% and there’s a difference in the before and after bonus issue ARRs too. According to the study, investors trade more near the dates of stock split and bonus issue and more trading takes place after stock split and bonus issue as compared to the period before it.

Problem Definition

The study aims to examine the impact of bonus issue announcement on the share price or returns or shareholder value. The problem can be defined as “The market reaction to bonus issue announcement of NIFTY 50 stocks”.

Hypothesis

Aim – Testing whether the bonus share announcements have significant impact on the share prices of the stocks comprised in the NIFTY 50 INDEX.

H0 (Null Hypothesis) There is no significant difference between the share prices of the companies before and after issue of bonus announcement.

H1 (Alternative Hypothesis) There is significant difference between the share prices of the companies before and after issue of bonus announcement.

The hypothesis testing is carried out for the entire sample, the IT sector stocks within the sample and the Refineries sector stocks within the sample.

OBJECTIVES

- To examine and analyze the impact of bonus issue on share price of stocks in NIFTY 50 Index.

- To examine and analyze further the differential impact of bonus issue on sectors in the NIFTY 50 Index.

METHODOLOGY

Sources of Data: The research study conducted is based on secondary data i.e. data collected from existing databases and publications. The data collected pertains to share price, bonus issue announcement date, ratio of bonus issue, value of NIFTY 50 index for event window, and companies that announced bonus issue in the last 10 years. The study gathers the information from money control, yahoo finance, bse guide and capital line.

Method of Collection: This study focuses on bonus issue by NIFTY 50 companies for a time frame of 2008 to current date 2017 in 13 different sectors. The sample consists of as of date NIFTY 50 stocks that carried out an announcement of bonus issue in the last 10 years, which equated to 27 bonus issue announcements from 13 different companies. The period of the study was selected so as to get a true reflection of market trends and evaluate the consistency of trends.

Design of the Study: The study is based solely on secondary data, regarding share prices of the companies composed in the NIFTY 50 Index. The study computes daily returns for individual securities on the basis of daily closing stock prices. The market return is calculated as the change in the NIFTY 50, which is the benchmark index of National Stock Exchange, composed of 50 of the largest and most actively-traded stocks on the NSE for 4 months prior the bonus issue.

Data Analysis and Technique: The study conducted uses the “ Standard Event Study Methodology”(Brown and Warner), which is a statistical method to analyze and assess the impact of an event on the value of a firm. The standard event study was used to compute Abnormal Returns (AR), Average Abnormal Returns (AAR), Cumulative Abnormal Returns (CAR) and Cumulative Average Abnormal Returns (CAAR) in the event window of the bonus issue announcement. The event window is taken as +/- 10 days from the bonus issue announcement date. Thus, in total we have 21 days surrounding the bonus issue, with the actual date of announcement taken as 0 i.e. the event day, and +1, +2, +3….. +10 as the following event window and – 1, – 2, -3…- 20 as the prior event window to get a sum total of 21 days.

Event Study Methodology: An event study analyzes the impact of a certain piece of news or event that is directly or indirectly related to a company and its share price. It can further be used as a macroeconomic tool to analyze the impact of an event on an industry, sector or overall market. The study aims to understand the effect of a specific event on a business’ or economy’s financial performance. An event study which is company specific analyzes the changes in the share price relative to the news or event. The “event” could be a merger and acquisition, bankruptcy, stock split, dividend announcement, bonus issue, etc. The aim of the study could be to analyze or further predict the impact of such announcements on the stock of a company. To carry out an event study we need to find the event date, event period and event window. The event date (t = 0) in the study conducted is the date of bonus issue announcement by the sample companies. The event window is set as 21 days and is considered as t-10 to t+10 relative to the event day t = 0. To identify the expected returns on day t, the market model is used. The market model is based on the assumption of a constant and linear relation between individual asset returns and the return of a market index:

Where,

- Rit is the daily return on security i at day t

- Rmt is the daily return on NIFTY 50 INDEX at day t

- αi, βi is regression intercept and slope coefficient estimators respectively

- Eit is the error term of the stock i on the day t.

This equation is modified to get the expected returns as : ERit = αi + βiRmt

Expected return is the estimated/predicted return of security “i” on a given day “t” by the use of regression analysis.

Where,

- ERit is the expected return on security i at day t

- αi, βi is regression intercept and slope coefficient estimators respectively

Stages of Event Study Methodology

Stage 1: The extensive data is collected pertaining to the companies comprised in NIFTY 50 who have announced bonus issue in the past 10 years, from 2017 to 2008. In the first stage, the data pertaining to the relative days of bonus issue is collected. The day the bonus issue is announced i.e. the event day is 0, and +/- 10 days share price values are found to give a “21 day” event window. This process is repeated 27 times, i.e. the sample size.

Stage 2: The NIFTY 50 Index Values were found for the event window for each event in the sample to serve as a benchmark for individual comparison.

Stage 3: Data relating to share price value and index value prior to 4 months of event day was found and was thus regressed to help us find true “alpha” and “beta” values for all 27 events. The holding period return ((P1-P0/P0)) is calculated for each day in the event and used in the regression equation to help us find predicted/expected daily returns of the security using the market model(formula stated above).

Stage 4: Once the expected daily returns were calculated, these values are then compared to the actual daily returns to see if there are any “abnormal returns”. Abnormal returns are calculated for the entire event window, but the main basis of comparison is the event day or the 0 day. Abnormal returns in the event window are calculated as:

ARit = Rit – ERit

Where,

- ARit is abnormal return of security ‘i’ at day ‘t’

- Rit is actual return of security ‘i’ at day ‘t’

- ERit is expect return of security ‘i’ at day ‘t’

Once the abnormal returns for the sample stocks have been calculated, we take out the average of the daily abnormal returns of the event window by aggregating the abnormal returns of each day in the event window for all the securities. Average abnormal returns (AARs) are used to analyze the information content of bonus issue announcements. The Average Abnormal Returns (AARs) of various securities on a particular event day ‘t’ is calculated as:

Where, ‘N’ denotes Number of Securities

The cumulative average abnormal return (CAARs) has been computed by cumulating the daily average abnormal returns for the entire event period. It is used to analyze the adjustment of prices to new information. The Cumulative Average Abnormal Returns (CAARs) are the sum of daily Average Abnormal Returns (AARs) during the event window.

Where, -k to +k denotes -10 to +10 days during the event window.

Stage 5: The average abnormal returns in all the trading days in the event window and cumulative average abnormal returns during the event window are analyzed by using ‘t’ test to identify whether they significantly differ from zero or not.

SCOPE OF THE STUDY

The scope of the study is limited to the bonus issue announcements by stocks that comprise or make up the NIFTY 50 Index as of today for the past 10 year i.e. from 2017-2008.

LIMITATIONS OF THE STUDY

- The study has a limited scope of 27 bonus issue announcement.

- The study only considers bonus issue announcements by NIFTY 50 stocks that make up a very small portion of the stock market as a whole.

- The study only focuses on bonus issue announcements, and does not take into consideration other factors that would affect share price movements like mergers, acquisitions, any news pertaining to financial performance, other corporate actions, fundamental news, etc.

- The study has a time period of 10 years.

RESULTS AND ANALYSIS

1. Regression

The study first identifies the companies in the NIFTY 50 with bonus issue announcement in the last 10 years. For the sample companies, 4 months prior bonus issue announcement, the share price is found along with the corresponding NIFTY 50 values. The Holding Period Return (HPR) for both the stock and the index individually is calculated as:

The HPR values are then regressed to find out the α (constant) and β (sensitivity) coefficients for the respective companies according to the market model equation.

The α and β thus found were then used to find the expected return for the company using the already known nifty 50 values.

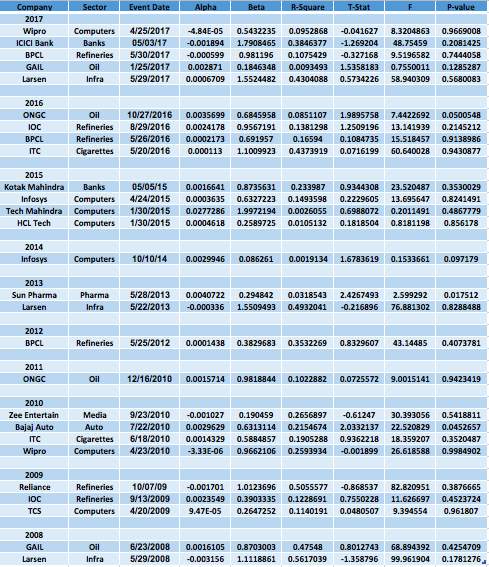

A summary table below shows the α (constant) and β (sensitivity) of companies with bonus issue announcement and the NIFTY 50 index.

The above table displays the summary of all the significant parameters which were collected from our research covering 8 sectors over the period of past 5 years namely 2017-2012.

Alpha is a measure of an investment’s performance compared to a benchmark, in this case the NIFTY 50. It’s a mathematical estimate of the return, based usually on the growth of earnings per share. The alpha for event window in all cases

is < 0.05 except Tech Mahindra in 2015. 20 out of 27 companies generate a positive alpha during the event window, indicating that investors are getting a higher return for taking the higher risk.

Beta, on the other hand, is based on the volatility—extreme ups and downs in prices or trading—of the stock or fund, something not measured by alpha. Beta is measured with respect to the market, in this case it is the NIFTY 50 as the benchmark. 7 companies have a beta > 1, indicating that their volatility is even greater than that of the market, i.e. if market goes up their share price will go up in higher proportion. Beta of selected stocks are usually high due the speculation around the event increasing the volatility. Beta on an average is also relatively high, indicating the market sentiment around a bonus issue announcement.

The R-squared, significance value and the f value were found out by regression analysis of the individual stock with the market index on the daily returns.

The average R-squared for the all the sample companies comes to 0.2201which can be interpreted as that 22% of the variation in the sample is caused due to the variation of the benchmark index i.e. Nifty 50.

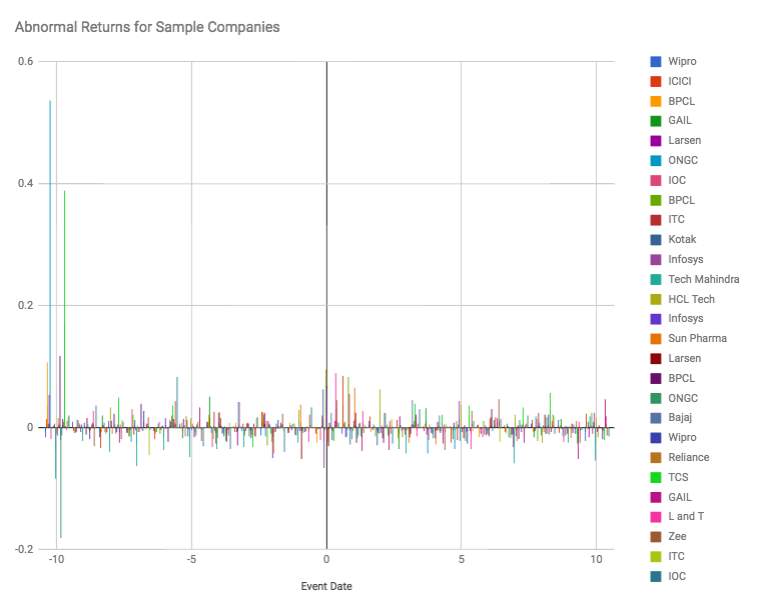

2. Abnormal Returns

If investors reacted favorably to an event, the expectation was that there would be positive abnormal stock returns around the event date. Conversely, if investors reacted unfavorably to an event, there would be negative abnormal stock returns.

Below is a graphical representation of the abnormal returns of each sample event.

3. Average Abnormal Returns And Cumulative Average Abnormal Returns

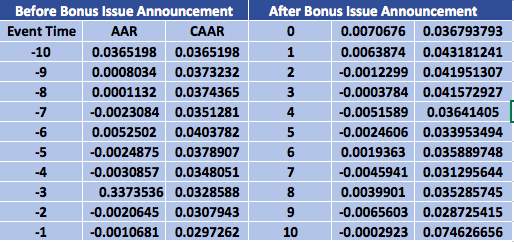

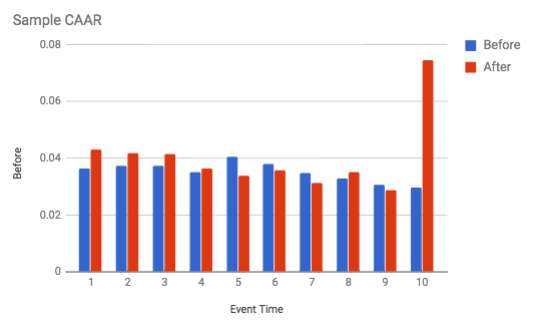

- All Sample Companies: The table below shows the Average Abnormal Returns (AARs) and Cumulative Average Abnormal Returns (CAARs) for all 27 bonus issue announcements, before and after the event date. It can be seen that the CAARs preceding the bonus issue announcement (-10 to -1) i.e. 3.47418431 are greater than the CAARs after the bonus issue announcement (0 to +10) i.e. 0.439690018. This could be because as the bonus issue nears, there is information leakage and in anticipation the demand is increasing. However, post bonus issue announcement, the CAARs decrease as theoretically the dilution of equity results in the same amount of profits being distributed in a larger number of equity shares.

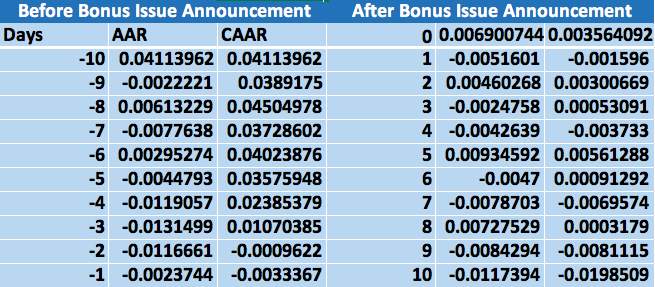

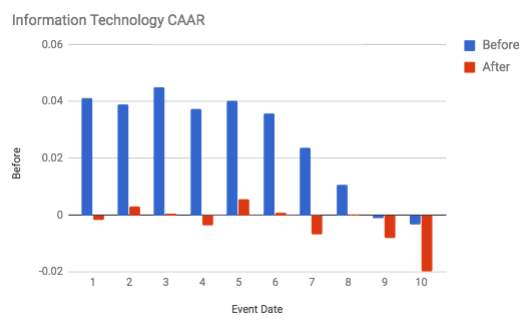

- Information Technology Sector: The table below shows the Average Abnormal Returns (AARs) and Cumulative Average Abnormal Returns (CAARs) for all 27 bonus issue announcements, before and after the event date. It can be seen that the CAARs preceding the bonus issue announcement (-10 to -1) i.e. 0.2686499 are greater than the CAARs after the bonus issue announcement (0 to +10) i.e. -0.0298675. Pre bonus issues the values are positive while post issue it is negative. This reflects the market sentiment specific to the IT Industry. Investors are reacting negatively to bonus issue as the bonus issue is smaller in size and fails to attract investors and hence delivers a negative impact. Bonus issue in IT industry is typically (2:1), and historical information shows a lot of delays in actual implementation of bonus issue in the IT industry thus the investors are unfavorably disposed to such corporate actions.

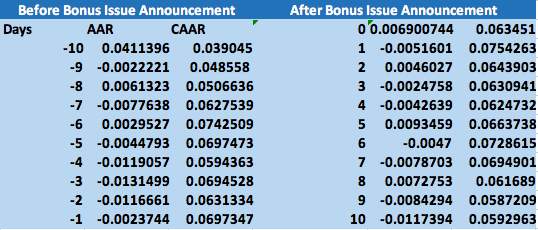

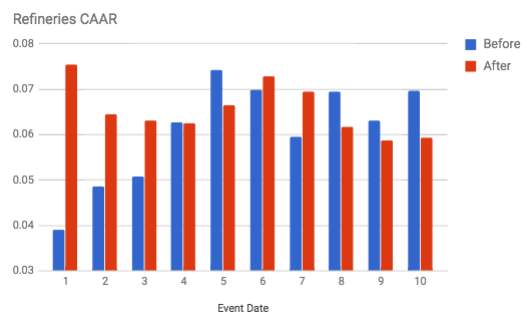

- Refineries: The table below shows the Average Abnormal Returns (AARs) and Cumulative Average Abnormal Returns (CAARs) for all 27 bonus issue announcements, before and after the event date. It can be seen that the CAARs preceding the bonus issue announcement (-10 to -1) i.e. 0.606776 are lower than the CAARs after the bonus issue announcement (0 to +10) i.e. 0.6538155. This could be due to the fact that refineries have a larger bonus issue size (1:5), which is attractive to investors and the share prices see a boom due to the increased demand as investors interpret increased profitability. Furthermore, the refineries industry in India has been doing spectacularly well in recent years as they have expanded their capacities significantly.

4. Trend of Cumulative Average Abnormal Returns

Sample:

The table depicts the cumulative average abnormal returns of the entire sample, as it can be seen from the table that the all the values for the CAAR lie between 0.03 and 0.04 except on the 10th day after the bonus issue. The CAARs are consistent throughout the 21 day period and no major trend can be seen. There is not a significant difference in the volume of shares traded.

Industry:

- IT

The IT Industry in India in past years has a subdued performance due to the depreciation of rupee compared to the US Dollar, impacting their profitability. Furthermore client issues and international policies on outsourcing have led to volatility in the industry. Bonus issue announcements are of a smaller size (2:1), and thus don’t attract investors. From the graph we can see that as we approach the event date, investors in anticipation of bonus issue are selling out rather than buying in and post bonus issue the values fall in negatives as their existing equity is being diluted. Thus, the volume of shares being traded in anticipation/before event is greater than post issue. The liquidity of shares goes down post bonus issue announcement as the market has reacted negatively.

b) Refineries

The graph above indicates the comparative difference before and after the bonus issue announcements. The CAAR is lower in the event window pre announcement as compared to post bonus issue announcement. However, this is balanced out from the -5/+5 th day which results in a 0.05 difference in sum total of CAAR before and after which is a marginal difference while comparing to the entire sample and IT Industry. The liquidity in the stock remains high post announcement as demand has increased and market reaction is positive.

3) IT vs Refineries

- Negative market reaction vs Positive market reaction

- Low Liquidity vs High Liquidity

- Greater difference in CAAR vs Marginal difference in CAAR

- Investors find bonus issue unattractive vs Investors find bonus issue attractive

- Higher beta vs Lower beta

- Significant difference vs No significant difference in share price

5. T test

Assuming that prices, indices and their respective returns in the event period were normally distributed, the t-statistic test was used to test for the significance at 95% confidence interval, with the cumulative average abnormal return and its standard deviation being used to determine the appropriate empirical t-statistic. T test was conducted for the sample as a whole as well as two industries namely – Technology and Refineries as they collectively form greater than 50% of the sample.

1.Sample CAAR T-test

The table depicts the paired sample t-test for all the 27 companies in our sample. The calculated t value comes to 4.135. The Degree of Freedom (DoF) is 9 and the p-value comes to 0.00253 which is less than 0.05. In this case we can accept the alternate hypothesis as it holds true which depicts that there is a significant difference between the bonus announcement and share price movement. The correlation is -0.1670 which states that there is a weak negative correlation coefficient between the companies

| Variable 1 | Variable 2 | |

| Mean | 0.347418432 | 0.159134336 |

| Variance | 0.015102643 | 0.003274736 |

| Observations | 10 | 10 |

| Pearson Correlation | -0.167009061 | |

| Hypothesized Mean Difference | 0 | |

| df | 9 | |

| t Stat | 4.135726637 | |

| P(T<=t) one-tail | 0.00126887 | |

| t Critical one-tail | 1.833112933 | |

| P(T<=t) two-tail | 0.002537739 | |

2. Industry Wise CAAR T-test

a)Technology: The table depicts the paired sample t-test for all the 7 companies in the IT sector of the sample.

The calculated t value comes to 6.943705277. The Degree of Freedom (DoF) is 9 and the p-value comes to 0.0000336573 which is less than 0.05. In this case we can accept the alternate hypothesis as it holds true which depicts that there is a significant difference between the bonus announcement and share price movement.

The correlation is 0.758805329 which states that there is a positive correlation coefficient between the companies in the information technology industry.

| t-Test: Paired Two Sample | ||

| Variable 1 | Variable 2 | |

| Mean | 0.02686499 | -0.00298675 |

| Variance | 0.00033367 | 5.30E-05 |

| Observations | 10 | 10 |

| Pearson Correlation | 0.758805329 | |

| Hypothesized Mean Difference | 0 | |

| df | 9 | |

| t Stat | 6.943705277 | |

| P(T<=t) one-tail | 3.37E-05 | |

| t Critical one-tail | 1.833112933 | |

| P(T<=t) two-tail | 6.73E-05 | |

| t Critical two-tail | 2.262157163 | |

b) Refineries: The table depicts the paired sample t-test for all the 4 companies in the Oil and Refinery Sector of our sample

The calculated t value comes to -1.03220. The Degree of Freedom (DoF) is 9 and the p-value comes to 0.1644 which is greater than 0.05. In this case we reject the alternate hypothesis and accept the null hypothesis as it holds true which depicts that there is no significant difference between the bonus announcement and share price movement.

The correlation is -0.03774 which states that there is a weak negative correlation coefficient between the companies.

| t-Test: Paired Two Sample for Means | ||

| Variable 1 | Variable 2 | |

| Mean | 0.060677598 | 0.065381553 |

| Variance | 0.000128061 | 3.16E-05 |

| Observations | 10 | 10 |

| Pearson Correlation | -0.377400806 | |

| Hypothesized Mean Difference | 0 | |

| df | 9 | |

| t Stat | -1.032207248 | |

| P(T<=t) one-tail | 0.164457092 | |

| t Critical one-tail | 1.833112933 | |

| P(T<=t) two-tail | 0.328914185 | |

| t Critical two-tail | 2.262157163 | |

Conclusion

1. There is a significant difference between the stock prices of the sample companies before and after the issue of bonus announcement. The paired sample t test conducted on pre and post bonus CAARs gives a p value of 0.00253 and a correlation of -0.1670. The results could be due the following reasons:

a. Information leakages in the market, i.e. parties close to the event announcement release data to unauthorized parties which cause investors to speculate and results in high cumulative abnormal returns before the bonus share announcement.

b. Bonus issue announcement leads to an increase in the freely tradable shares in the stock market which in turn causes a dilution in equity of existing shareholder. As the equity is being diluted but profits remain unchanged, the Earning Per Share(EPS) is brought down which drives down the stock price in proportion. This fundamental reflects in the market sentiment post bonus issue announcement. A negative price trend post bonus issue is not always a bad thing, it can also be a price correction and will stabilize in the further upcoming days as there is more clarity in time. The CAARs might fall for a short term but then usually improve because bonus issues are generally taken as a sign of profitability of the company. However, to make a decision regarding the long term impact is hard as stock price cannot be taken in isolation, it is affected by a number of factors like volume, liquidity, etc. If these factors fail to catch up, it might hurt the company’s share price and bears would lose out in such a scenario.

2) There is significant difference between the impact of bonus share announcement on the financial sector vs. the non-financial sector.

(a) There exists a significant difference on the CAARs of the share price before the bonus announcement in the Technology and Oil Refinery as the p value is 0.0011 which is less than 0.05.

(b) A significant difference does not exist in the CAARs of the share price after the bonus announcement in the Technology and Oil Refinery as the p value is 1.2194 which is more than 0.05.

(c) A significant difference does not exist in the CAARs for Technology and Oil Refinery sectors for the entire window for 10 days pre and post bonus issue as the p value is which is greater than 0.05.

(d) The general direction of the CAARs can be determined from the negative correlation of 3.681.

References

https://www.acmeintellects.org/images/AIIJRMSST/Oct2013/12-10-13.pdf

http://chss.uonbi.ac.ke/sites/default/files/chss/THESIS-FINAL(1).pdf

http://www.allresearchjournal.com/archives/2015/vol1issue7/PartL/1-7-172.pdf

http://chss.uonbi.ac.ke/sites/default/files/chss/BESSIE%20COMPLETE.pdf1_.pdf

http://apjor.com/downloads/0801201515.pdf

http://acrpub.com/article/publishedarticles/02102015IARJEF232.pdf

http://iiste.org/Journals/index.php/JEDS/article/viewFile/35121/36124

http://ijiet.com/wp-content/uploads/2017/01/341.pdf

http://www.ijmra.us/project%20doc/IJMT_SEPTEMBER2012/IJMRA-MT1323.pdf

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1087200

http://www.pbr.co.in/December2014/5.pdf

http://shodhganga.inflibnet.ac.in/bitstream/10603/10921/7/07_chapter3.pdf

https://in.finance.yahoo.com/quote/ONGC.NS/history/

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

Related Content

All TagsContent relating to: "Finance"

Finance is a field of study involving matters of the management, and creation, of money and investments including the dynamics of assets and liabilities, under conditions of uncertainty and risk.

Related Articles

DMCA / Removal Request

If you are the original writer of this dissertation and no longer wish to have your work published on the UKDiss.com website then please: